ECONOMICS COMMENTARY — 02 Jun, 2026

Global PMI shows factory growth spurt amid boost from price and supply worries

PMI survey data indicate that global factory production growth accelerated to a near five-year high in May, with the war in the Middle East having induced a surge in demand for manufactured goods and inputs. However, this growth spurt is being fuelled by precautionary stock building, as companies seek to safeguard against supply shortages and prices hikes linked to the conflict.

The forward purchasing by definition points to weaker growth of purchasing and production in the coming months.

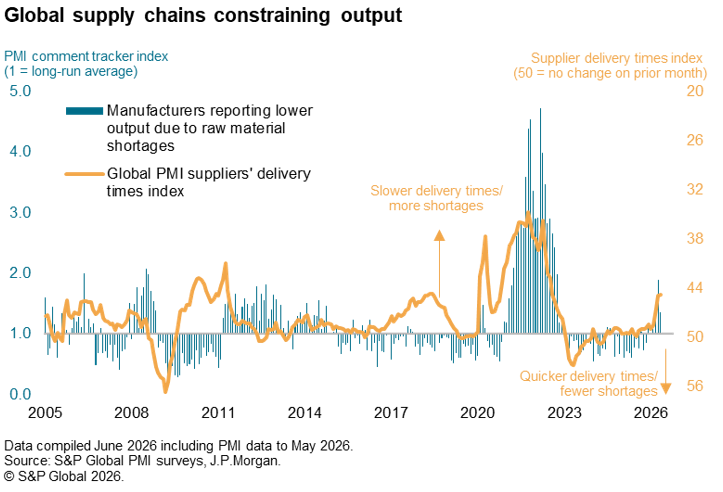

Supply shortages, which have been more widely reported than at any time since 2022 in recent months, have already been reported as constraining output to a degree not witnessed since 2022. These constraints threaten to not only subdue growth but could also sustain further price pressures.

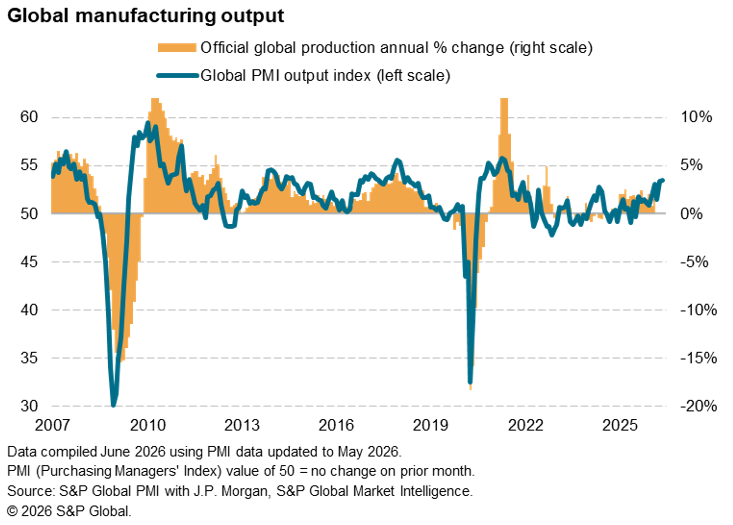

Factory production growth at fastest for nearly five years

The Global Manufacturing Purchasing Managers’ Index (PMI) survey, sponsored by J.P. Morgan and compiled by S&P Global Market Intelligence, recorded the sharpest rise in worldwide factory production since July 2021 in May. The latest rise built on a similarly strong increase in April.

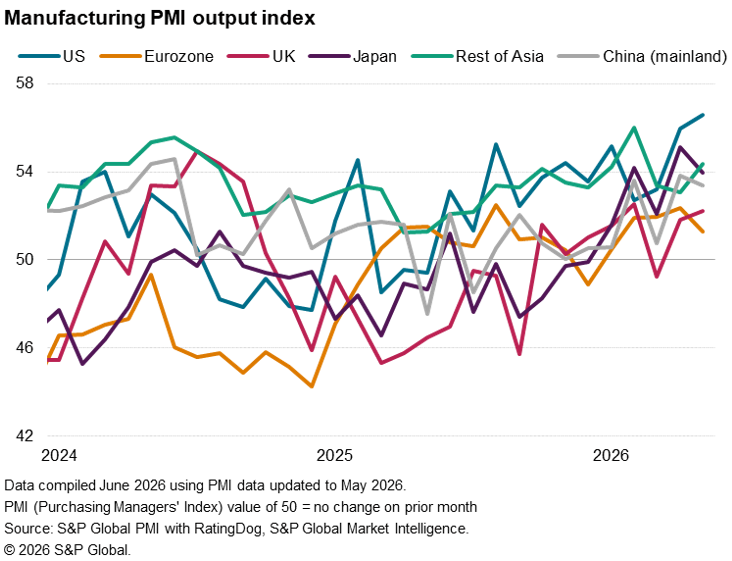

US output growth hit the highest for just over four years in May, and the past two months have seen among the largest gain in production in Japan since the start of 2018. The solid expansion in mainland China was among the strongest for two years. The upturn in eurozone was meanwhile modest. Albeit in both cases, rates of growth lost a little momentum in May. The rest of Asia saw sustained strong output growth in May.

Stock building boosts growth

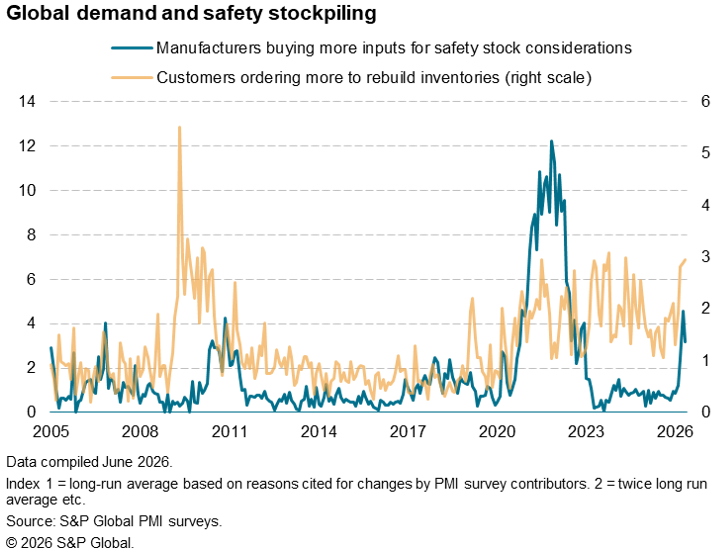

While the data point to encouraging resilience of the manufacturing economy as the war in the Middle East extended into its third month in May, growth in many cases has been buoyed by precautionary stock building as companies seek to buy good ahead of supply shortages or price rises linked to the war.

Analysis of comments provided by surveyed companies, explaining changes in order books and purchasing behaviour, reveal that the three months since the outbreak of war have seen the highest number of orders received due to customers building inventory since the global financial crisis. The number of manufacturers building safety stocks has meanwhile risen over the past two months to the greatest extent since the pandemic and Ukraine war stock build seen 2022.

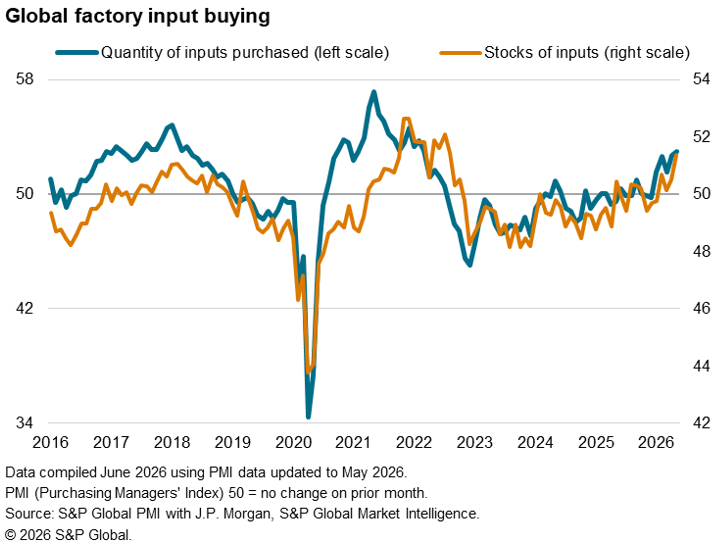

Input buying and inventories of inputs have likewise both risen in recent months at the steepest rates since 2022, in both cases the rate of increase gaining momentum in May.

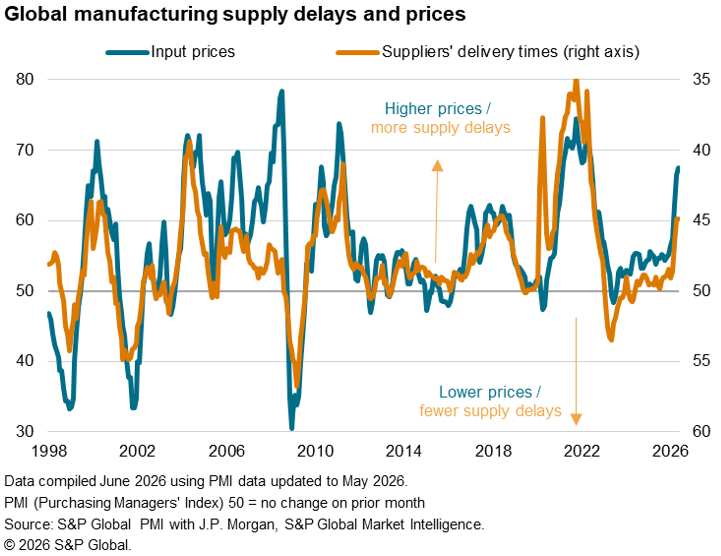

Supply delays and price pressures intensify

The surge in demand for inventory has exacerbated supply and shipping delays caused by the closure of the Strait of Hormuz. As a result, average supplier delivery delays have lengthened in April and May to the greatest extents since mid-2022.

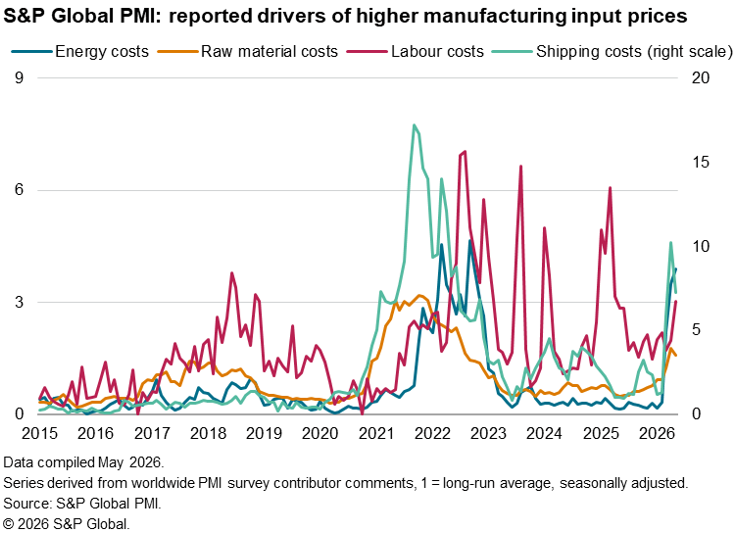

With demand exceeding supply for many products, prices have risen sharply again in May. Higher energy and shipping prices have also fed through to increased costs. Factory input costs consequently rose globally at the steepest rate since June 2022 during May, the rate of inflation having accelerated now for fourth successive months.

Inventories hold key to outlook

Looking ahead, the precautionary stock building is providing only a temporary boost to manufacturing output, and the bringing-forward of purchases – both by manufacturers and their customers – will inevitably result in weaker input buying, production and sales when the inventory cycle turns.

One upside of this inventory shift is the cooling of price pressures it could bring, as demand softens. However, it will also be important to assess how much supply shortages lead to production constraints, which could trigger further price rises by sustaining the supply shock. PMI contributors already report that war-related supply shortages have constrained output to a degree not seen since 2022.

Much will of course depend on the duration of the conflict and its associated energy and supply chain disruptions. However, it is widely anticipated that it could take months for energy and shipping markets to return to normal even in the event of a swift resolution to the closure of the Strait of Hormuz, hinting at persistent high prices and rising production constraints as we head through the summer.

Access the latest global PMI press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings