ECONOMICS COMMENTARY — 10 Jun, 2026

Global economy stuck in slow lane as advanced economies see falling demand for services

May’s PMI surveys produced by S&P Global indicated that the pace of worldwide economic growth held steady in May, but at a reduced rate compared to prior to the outbreak of war in the Middle East. A divergence has opened up, however, with economic weakness spreading to more advanced economies, linked in part to rising prices, notably for services. In contrast, emerging markets have reported fewer price pressures and stronger growth.

Global PMI rises in April

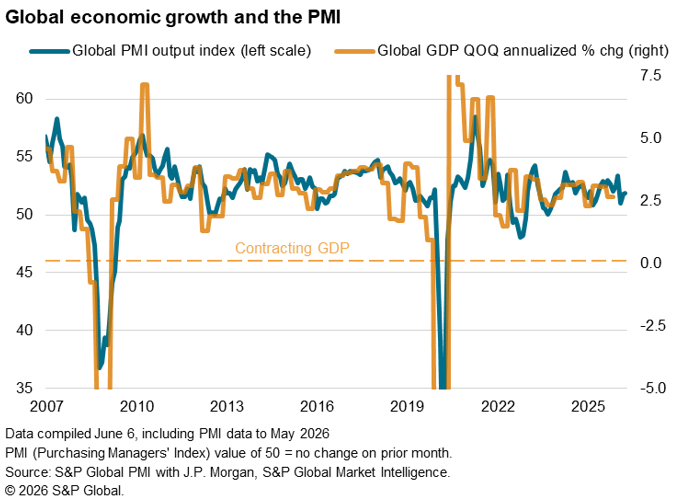

Survey data indicate that the war in the Middle East continued to subdue global economic growth in May. The J.P.Morgan Global Composite PMI Output Index held steady at 51.8 in May indicating an expansion of business activity for a fortieth successive month.

While the past two months have seen stronger growth than the recent low seen in March, the average expansion over the past three months – since the outbreak of the war in the Middle East – has nevertheless been the weakest since the second quarter of last year (when growth slowed largely in response to the announcement of broad-based US tariffs).

The PMI readings are broadly indicative of global GDP growth running at an annualized 2.5% rate over the past two months, down from around 3% at the start of the year.

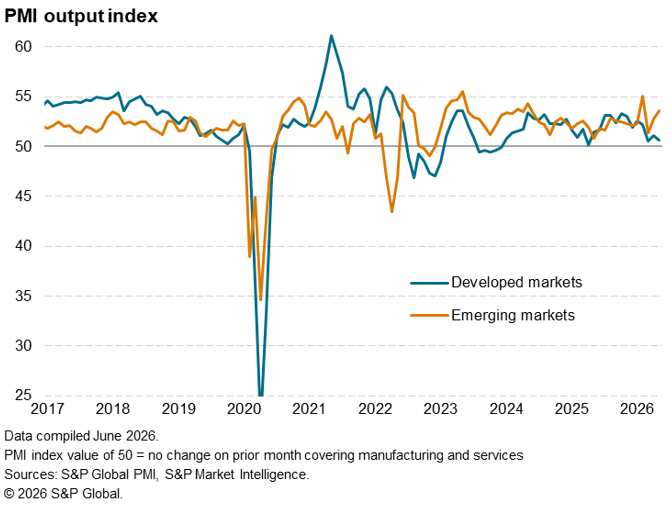

Advanced economies lag emerging markets

A notable divergence has developed in May, with emerging market growth accelerating to the second-fastest for two years, while growth in the advanced economies has slowed to one of the weakest recorded over the past two years.

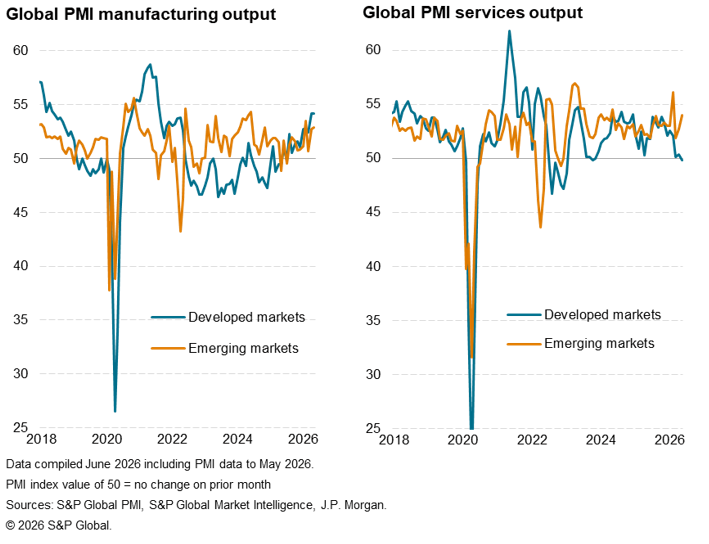

Both markets saw rising manufacturing output, but a key differential is the performance of the service sector. Emerging markets reported the second-strongest rise in factory output for one and a half years, while advanced economies reported the joint-steepest rise since mid-2021, the rate of expansion matching the recent high seen in April. In both advanced and emerging markets, gains were characterised by companies building precautionary inventories amid war-related price and supply concerns, However, although the emerging markets collectively saw service sector business activity rise at the sharpest rate since June 2024, services activity in the advanced economies contracted for the first time since October 2023, reflecting a second-successive monthly dip in new order inflows.

War-related stress spreads to more advanced economies

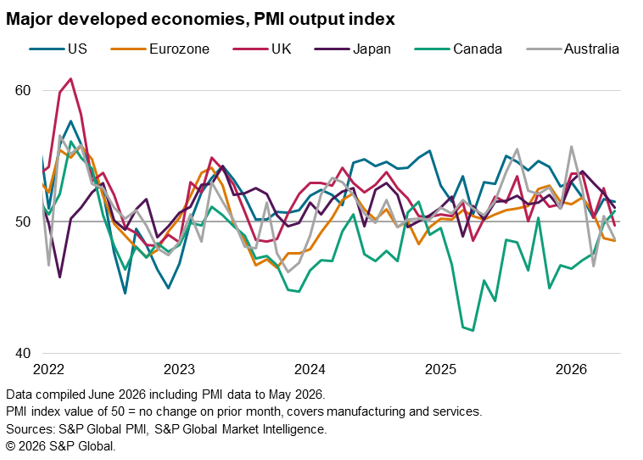

Looking further at the advanced economies, hardest hit by the war in the Middle East so far has been Europe. The eurozone saw output fall for a second month running in May, with the rate of decline accelerating slightly to the fastest for one-and-a-half years. The further weakness of the eurozone PMI hints at a contraction of GDP of around 0.2% in the second quarter. The UK PMI also fell into contraction territory, for the first time in just over a year, likewise hinting at a potential small contraction of GDP in the second quarter if weakness persists into June.

However, the advanced APAC economies are now likewise showing more signs of stress. Australia saw a fall in output for the second time in the past three months, pointing to its worst growth patch since late 2023, and output growth hit joint-lowest for a year in Japan to register only a modest expansion.

While the US was the strongest performer of the big advanced economies, its expansion was among the weakest seen over the past two-and-a-half years to point to just 1% annualized growth. Canada meanwhile managed only modest growth, albeit reviving from a six-month downturn to register its largest improvement for one-and-a-half years.

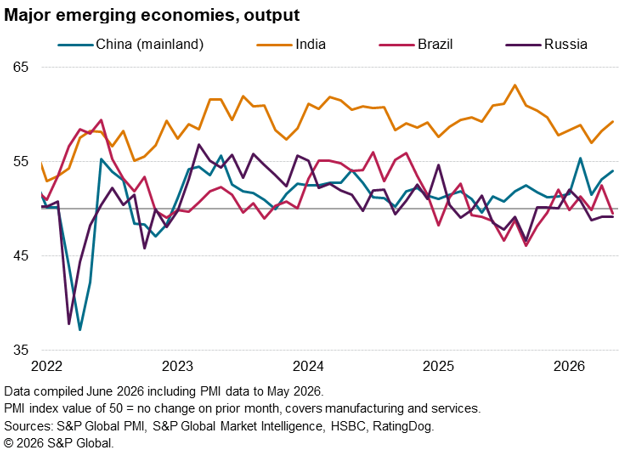

Emerging market growth accelerates

Among the emerging markets, the improvement in performance was fueled by mainland China and India, in turn reflecting better service sector trends alongside manufacturing expansions, but downturns were seen in both Russia and Brazil.

India remained the strongest performer, with output growth lifting further from March’s 40-month low to reach a six-month high thanks to improved gains across both goods and services.

A further upturn in growth was also recorded in mainland China. Having slowed sharply in March, the expansion gained further traction to register the second-strongest growth for two years amid a broad-based upturn.

In contrast, Brazil reported a slip back into contraction territory after a solid uptick in April, with a near-stalled service sector accompanied by a sharp decline in manufacturing output.

Output in Russia contracted for a third successive month, led by a weakened services economy.

Higher prices killing demand

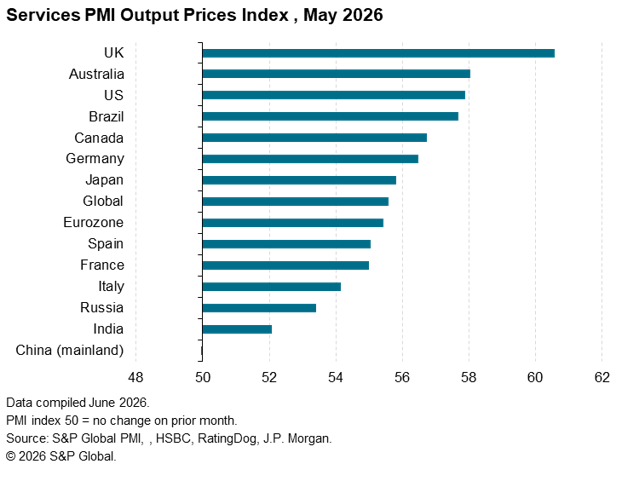

A key determinant in the divergence of performance in the services sectors appears to be prices. While manufacturing has also seen high prices, demand for goods has been relatively inelastic compared to services reflecting the buying of inventory ahead of further price rises or supply shortages. In contrast, no such inventory build is relevant to many services, and instead demand here is being impacted by high prices in many economies, especially those seeing the steepest rates of inflation, notably the UK, Australia and the US but also the eurozone economies and Japan. In economies where services inflation remains muted or is falling, namely India and mainland China respectively, demand for services has been holding up much better.

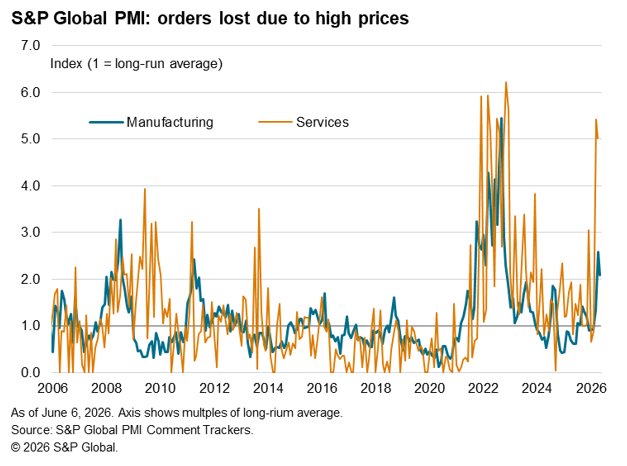

PMI comment trackers monitoring price impact

The impact of high prices on demand is reflected in the global PMI Comment Trackers, which tracks anecdotal evidence provided by surveyed companies to determine the extent to which new orders have been affected by prices. In the services sector, only the pandemic saw demand being hit more by high prices than was reported in April and May of 2026, with recent levels almost matching pandemic highs. In manufacturing, cases of price-related demand losses have also spiked, but to a much lesser degree than in the pandemic.

Monitoring this impact of ‘demand destruction’ will be important in assessing economic outlooks in the coming months.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings