Research — June 30, 2026

Accenture postQ: Weaker bookings and cautious outlook remain in focus

By Bhavik Jain and Soumya Khandelwal

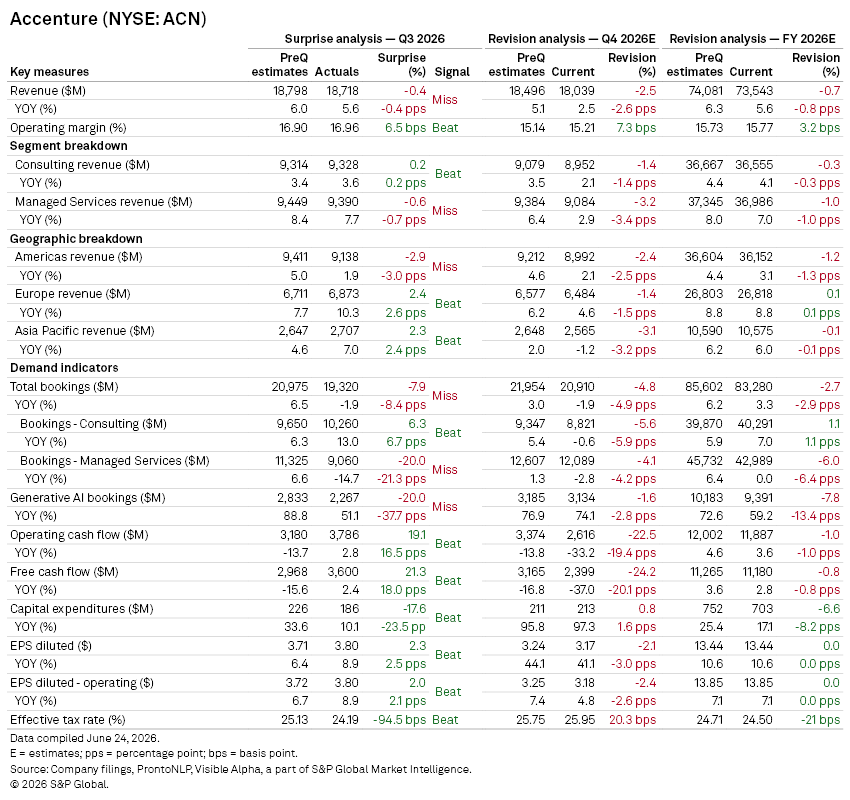

Accenture (NYSE: ACN) delivered fiscal third-quarter 2026 results on Thursday, June 18, that were broadly in line with consensus expectations, with profitability and cash generation offsetting a modest revenue miss. However, attention quickly shifted to weaker-than-expected bookings, particularly within Managed Services, and management's decision to narrow its fiscal 2026 revenue growth outlook.

Looking at earnings summaries compiled by S&P Global Pronto NLP, along with Visible Alpha pre-quarter consensus expectations and revised outlook, here are some key takeaways.

Key takeaways

Q3 revenue rose 5.6% year-on-year to $18.7 billion, slightly below Visible Alpha consensus expectations. GAAP diluted EPS of $3.80 exceeded expectations by 2%, while operating margin of 17% came in modestly ahead of forecasts, reflecting continued operational discipline despite an uneven demand backdrop.

The quarter highlighted a growing divergence between Accenture's two core businesses. Consulting revenue increased 4% year-on-year to $9.3 billion and modestly exceeded consensus expectations, supported by ongoing enterprise transformation programs and AI-related investments. Managed Services revenue, on the other hand, grew a faster 7.7% to $9.4 billion, driven by demand for cloud, data and AI-enabled outsourcing solutions, but came in slightly below consensus forecasts.

Regional performance was mixed. Europe and Asia-Pacific both delivered stronger-than-expected growth. The Americas, however, fell short of consensus expectations.

The most closely watched metric was bookings, where results disappointed. Total bookings declined 1.9% year-on-year to $19.3 billion, missing consensus expectations by 7.9%. While Consulting bookings rose 13% to $10.3 billion on strong demand for AI-led transformation projects and digital reinvention initiatives, Managed Services bookings fell 15% to $9.1 billion following the postponement of several large contracts and regional deal slippage. Management emphasized that the weakness reflected timing rather than a deterioration in underlying demand.

AI-related bookings reached $2.3 billion, up 53% year-on-year, but fell significantly short of elevated analyst expectations.

Cash generation remained a notable strength. Operating cash flow increased 2.8% year-on-year to $3.79 billion, while free cash flow rose 2.4% to $3.60 billion, exceeding consensus by 19.1% and 21.3%, respectively. Lower-than-expected capital expenditures of $186 million contributed to stronger cash conversion despite softer bookings.

Guidance

Looking ahead, management struck a more cautious tone.

For Q4 FY2026:

- Revenue guided at $17.75 billion-$18.40 billion, implying growth of roughly 1%-5% . The guidance came in below preQ consensus expectations.

For the full year:

- Accenture narrowed its revenue growth outlook to 3%-4%, reducing the upper end of the previous range amid continued weakness in federal services and an uncertain spending environment.

- Despite the softer revenue outlook, management raised adjusted EPS guidance and reiterated its commitment to margin expansion.

- Accenture also reiterated plans to return at least $9.5 billion to shareholders through dividends and share repurchases while deploying approximately $9 billion toward acquisitions during FY2026.

Analyst Q&A highlights

Management acknowledged that client spending remains cautious heading into Q4, with geopolitical uncertainty, particularly disruptions related to the Middle East, continuing to weigh on discretionary consulting demand.

Looking ahead to FY2027, management outlined several potential growth drivers, including roughly 2% inorganic revenue contribution from recent acquisitions, an expected recovery in federal services, continued expansion in enterprise AI spending and increased penetration of the mid-market through Accenture Edge.

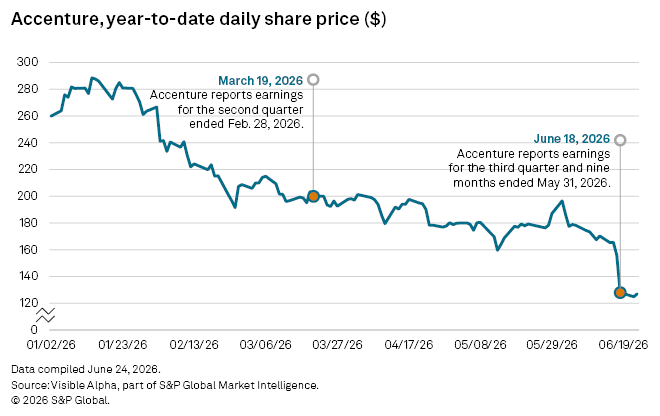

Share price reaction

Accenture shares declined following the results as investors focused less on stronger earnings and cash flow and more on the weaker bookings performance, particularly in Managed Services, the reduction in the upper end of FY2026 revenue growth guidance and management's cautious commentary on enterprise spending.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment