ECONOMICS COMMENTARY — 22 May, 2026

Week Ahead Economic Preview: Week of 25 May 2026

The following is an extract from S&P Global Market Intelligence's latest Week Ahead Economic Preview. For the full report, please click on the 'Download Full Report' link.

Inflation data to guide central bank policy decisions

Inflation updates for many of the world’s largest economies will be in the spotlight in the coming week as policymakers and markets assess the likely next moves in interest rates.

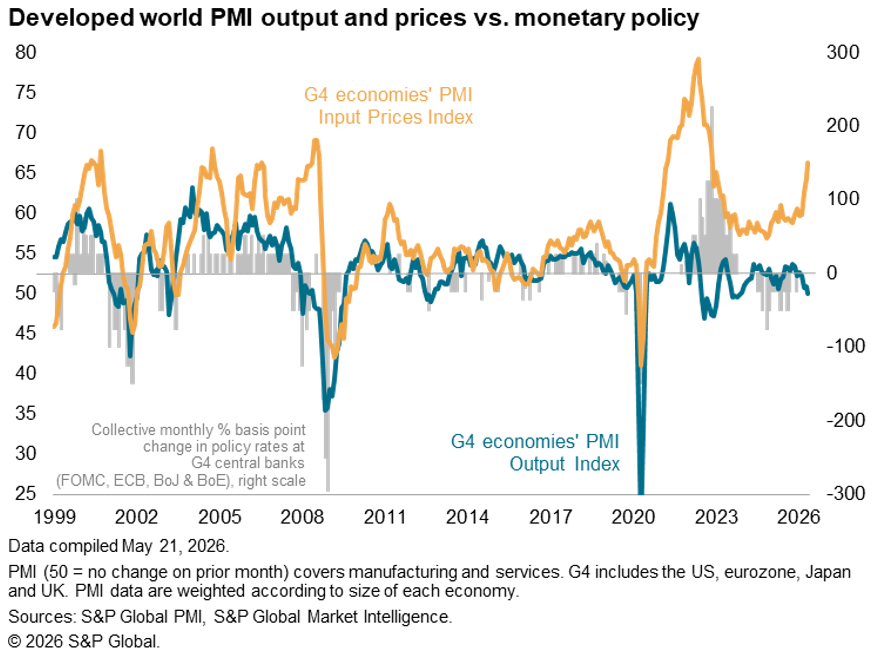

Kevin Warsh has taken over as Chair of the US Fed’s rate setting committee as inflation indicators are flashing red. After the US consumer price index showed the annual rate of inflation rising to 3.8% in April, its highest since May 2023, the coming week’s updated core PCE inflation measure – widely touted as the Fed’s preferred gauge – will be eagerly awaited. Core PCE prices rose at a 3.2% annual rate in March, up 0.3% on a month ago. Any large uplift will add to market speculation that rates are on hold for the rest of the year, and that the next move could even be a hike. Note that S&P Global’s flash US PMI survey hinted at yet another rise in price pressure in May as the war triggered more cost growth among businesses.

However, with the flash US PMI signalling only modest output growth in May, the Fed will be eager to see how well the economy is holding amid the ongoing war in the Middle East. Hence US trade data and durable goods orders, plus further survey activity measures from the Chicago, Richmond and Dallas Feds, will all be closely eyed in the coming week.

The European Central Bank will also be assessing inflation trends via consumer price indices for Germany, France and Italy, as well as producer price data for Italy, France and Spain. The flash eurozone PMI survey data showed price growth accelerating due to a growing supply shock to the region, but also indicated that the economy has now fallen into a deepening downturn, complicating the policy stance.

Inflation data are likewise updated for April in Australia, where the reserve bank has already hiked its policy rate at its last three consecutive meetings in response to rising prices. The RBA’s May meeting concluded with warnings that more rate hikes were likely needed. However, with PMI data hinting at growing downturn risks for the economy, it will be interesting to see if policymakers move more cautiously.

Other notable releases during the week include first quarter GDP for the US (its second estimate), Canada, Brazil, Italy and Singapore. However, in all cases these data are capturing conditions prior to the impact of the war in the Middle East, so hold few signals for the economic outlook. Nonetheless, strong first quarters will be important in helping position economies to weather the conflict.

Chart of the week: Flash PMIs signal stagflation

S&P Global’s flash PMI surveys showed business growth grinding to a halt in May as the war in the Middle East exerts a growing toll. Europe is hardest hit, with the UK and eurozone economies now both in decline, but the US and Japanese expansions have also shifted down gears since the onset of the conflict.

Services have generally reported the worst deterioration in demand, whereas manufacturers have continued to benefit in May from stockpiling. This precautionary stock build will only be temporary, however, and reflects growing concerns over supply conditions (with supply availability having deteriorated markedly again in May) as well as worries over price hikes. Manufacturing input price inflation accelerated sharply among the major economies to reach a four-year high, with energy prices also pushing up service inflation.

These indications that the major economies are already facing stagflationary conditions poses a major challenge to central bank policymakers.

Read more about recent worldwide PMI trends here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings