ECONOMICS COMMENTARY — 15 May, 2026

Week Ahead Economic Preview: Week of 18 May 2026

The following is an extract from S&P Global Market Intelligence's latest Week Ahead Economic Preview. For the full report, please click on the 'Download Full Report' link.

Flash PMI insights into growth, supply and price trends amid Middle East conflict

Flash PMI surveys for the US, Eurozone, Japan, UK, India and Australia come under the spotlight for growth and inflation trends, with official industrial production data also released for a number of key economies.

The flash PMI surveys for May will provide an important update on how economies are faring in the third month of conflict in the Middle East.

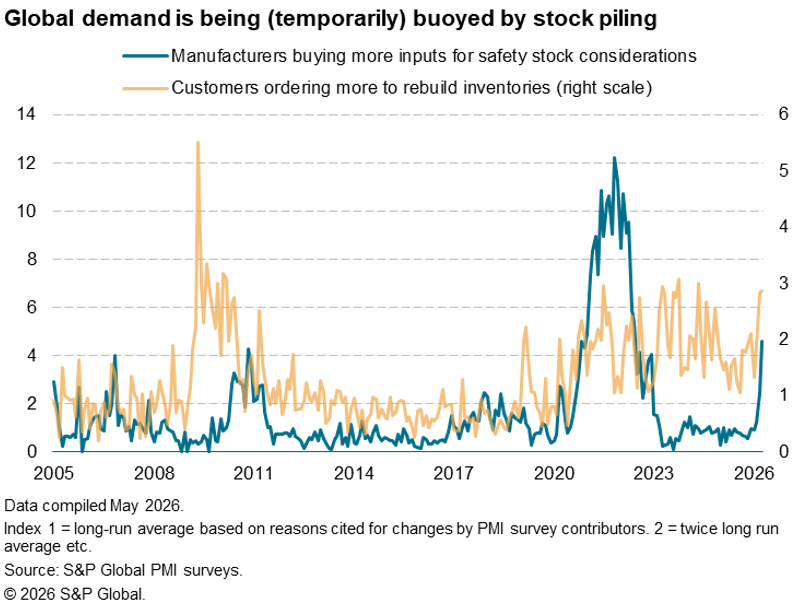

It’s clear that global growth kicked down a gear in March and remained subdued in April. However, even these weakened numbers likely overstate the underlying health of many economies, as expansions were often flattered by precautionary stockpiling. This stock build drove a large jump in factory production and shipments (factory production growth in Japan hit a 12-year high in April, a four-year high in the US, and just over a four-year peak in the eurozone). The stocking cycle may have longer to run but will eventually dampen growth rates when sufficient inventories have been accumulated, as will the reasons for why companies are stockpiling: supply chain delays are at their highest since the pandemic supply crunch in 2022, with prices rising accordingly. Supply problems will constrain growth just as high prices will ‘destroy’ demand, notably for consumer-oriented services such as travel and tourism, which is already the hardest hit sector globally, according to April’s detailed sector PMI numbers.

The message from the PMIs has therefore been one of heightened stagflation risks, with rising prices accompanied by stalling growth. Central banks have thus far been holding rates steady, unsure of which way to tread, but the markets are increasingly pricing in more hawkish stances as the inflation numbers pick up, as anticipated by the PMIs.

Further insights into the Bank of England’s next potential will be provided by official labour market, retail sales and inflation data, the latter also updated in the eurozone to assist the ECB’s estimation of price trends.

In the US, besides the flash PMIs, the coming week sees official industrial production and University of Michigan consumer confidence survey data.

In Asia, we will be watching out for industrial production data for Japan and mainland China, the latter also releasing retail sales and investment data.

However, for all these production releases, we encourage some caution as stock piling will be flattering growth rates.

Chart of the week: Supply chains hold key to growth and inflation trends

One of Alan Greenspan’s favourite leading indicators of inflation when at the helm of the US Fed, the PMI survey’s gauge of supplier delivery times is back in focus. Longer deliveries mean problems getting timely supplies into factories, handing pricing power to the seller. This commonly generates upward pressure on inflation which materialises in higher household prices with a delay of three to six months.

Supply delays naturally constrain output growth, but have also encouraged safety stock building – something that will inevitably fade to provide an additional drag on growth.

Amid ongoing war in the Middle East, April saw the longest lengthening of delivery times worldwide since the pandemic supply squeeze in 2022. With the flash PMI surveys out next week, we’ll be looking to see how supply chains in major economies have fared in May, and how inventory management is impacting growth rates.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings