Research — May 20, 2026

Visible Alpha breakdown of Canadian big banks’ Q2 2026 earnings expectations

Canada’s largest banks head into fiscal Q2 2026 earnings facing a more complex macro backdrop than they did just three months ago. The domestic economy is being pulled in opposing directions. Renewed US tariff pressures and slowing labor markets are weighing on growth, while higher oil prices linked to conflict in the Middle East are providing a partial offset for an energy-exporting economy already grappling with sticky inflation and weaker household spending.

Bank of Canada has kept its benchmark rate at 2.25% as policymakers weigh the inflationary impact of higher energy prices against softer economic momentum and rising unemployment. Recent central bank commentary has highlighted how tariffs and trade uncertainty are putting Canada’s economy “on a lower path”, even as oil prices offer some support to exports and national income.

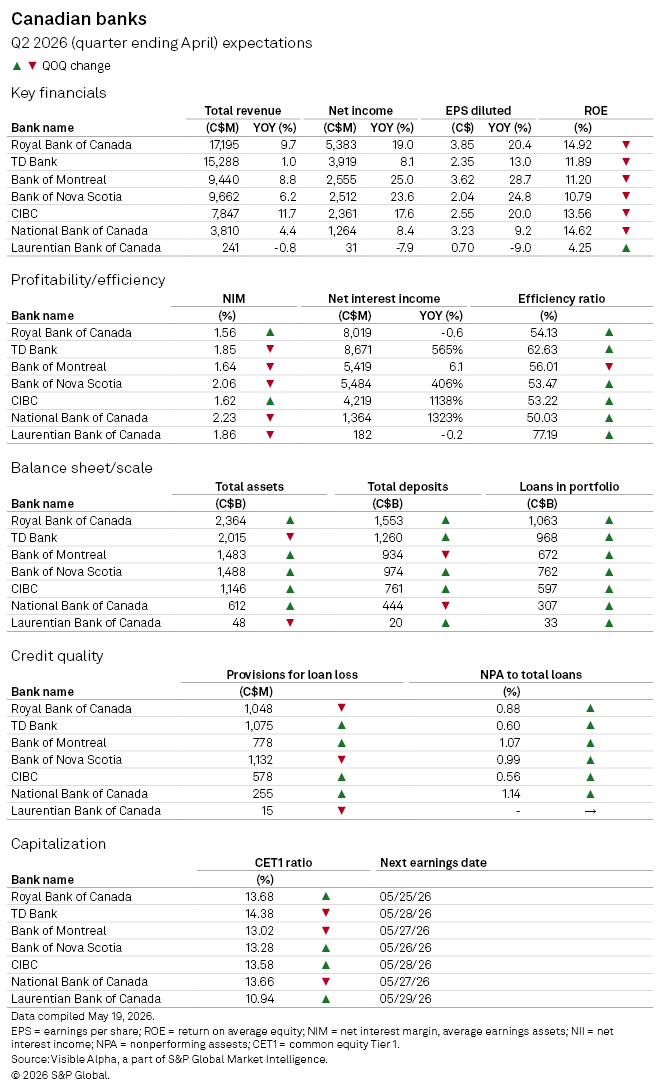

Against this backdrop, Visible Alpha consensus expectations show Canada’s major banks are still poised to deliver resilient fiscal Q2 2026 results for the April quarter. Strong capital markets activity, steady loan growth and largely stable credit quality are expected to support earnings, even as lower interest rates continue to pressure margins across the sector. Consensus expectations point to healthy year-over-year growth in revenue and earnings across most banks, although profitability metrics such as ROE and NIM are expected to soften sequentially.

Among the Big Six, Royal Bank of Canada/ RBC (TSE: RY) is expected to see net income growth of 19% year-on-year to C$5.4 billion, on revenue growth of nearly 10%. ROE, however, is expected to edge lower sequentially to 14.9%. Net interest margin (NIM) is projected to improve modestly quarter-on-quarter to 1.56%, while provisions for credit losses are expected to decline sequentially, signaling stable credit performance.

The Toronto-Dominion Bank (TSE: TD) is expected to report comparatively muted revenue growth of less than 1%, though net income is still forecast to rise 8% year-on-year. TD concluded its major restructuring following significant anti-money laundering (AML) failings, involving US regulatory settlements, a 3% workforce reduction, and an C$886 million total pre-tax charge in early 2026. Analysts are now focused on margin pressure and capital deployment following the restructuring efforts and regulatory scrutiny in the US. TD’s NIM is expected to decline sequentially to 1.85%, while its CET1 ratio is projected to remain among the strongest in the peer group at 14.4%, despite a modest sequential decline.

Bank of Montreal (TSE: BMO) and The Bank of Nova Scotia (TSE: BNS) are both expected to deliver strong bottom-line growth, with net income projected to rise roughly 25% and 24%, respectively. BMO’s earnings outlook is expected to continue benefiting from cost synergies, scale efficiencies and improved operating leverage tied to its 2023 acquisition of Bank of the West, as the bank moves further beyond the heavier integration phase and focuses more on extracting profitability from its expanded US franchise. Scotiabank is expected to benefit from improving international banking trends and expense discipline. However, both banks are also expected to see sequential compression in ROE and NIM, due to the industry-wide challenge from a declining rate environment.

Canadian Imperial Bank of Commerce (TSE: CM) is expected to remain a solid retail banking performer this quarter, with revenue projected to increase 11.6% and earnings up 17.6% year-on-year. CIBC’s net interest income is expected to grow 11.5%. However, the bank’s efficiency ratio is expected to rise sequentially to 53.2% from 51.4% in Q1, though the metric remains broadly improved relative to 54.2% in the year-ago quarter.

National Bank of Canada (TSE: NA) is expected to continue benefiting from resilient retail and commercial banking activity in Quebec, where the bank maintains a stronger market presence than most peers, alongside continued strength in capital markets activity. Revenue and earnings are forecast to rise 3.9% and 7.9%, respectively. The bank is also expected to maintain one of the highest NIMs in the peer group at 2.23%, though sequential compression remains evident.

Meanwhile, Laurentian Bank of Canada (TSE: LB) is expected to remain an outlier, with revenue, earnings, and EPS all forecast to decline year-on-year. While ROE is expected to improve sequentially, efficiency metrics remain significantly weaker than peers, reflecting ongoing restructuring and scale challenges.

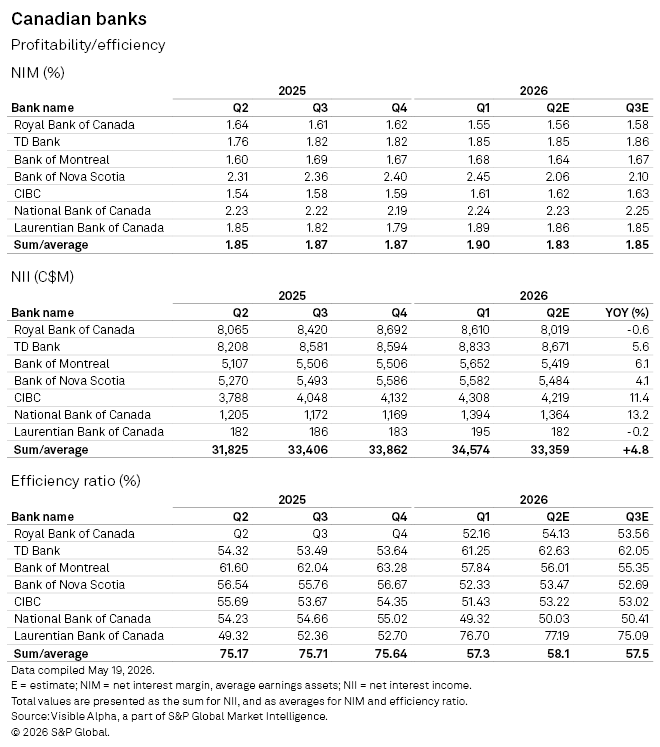

Profitability and efficiency: Margin compression to persist despite resilient NII growth

Diving deeper into profitability metrics, consensus expectations for Q2 2026 suggest Canadian banks will continue to face pressure as lower interest rates weigh on NIM, although net interest income (NII) growth remains broadly resilient due to balance sheet expansion and loan growth.

Most banks are expected to report either stable or lower margins sequentially, with the sharpest projected decline at Scotiabank, where NIM is forecast to fall to 2.06% from 2.45% in Q1. Meanwhile, CIBC and RBC are among the few banks expected to post modest sequential stabilization in margins.

Despite softer margins, aggregate NII for the group is still expected to rise 4.8% year-on-year, benefiting from loan growth and larger earning asset bases.

Efficiency trends remain mixed across the sector. National Bank of Canada continues to stand out as the most efficient large Canadian bank, with an efficiency ratio near 50%, while Laurentian Bank of Canada remains a laggard at over 77%. Among the Big Six, TD Bank is expected to maintain the weakest efficiency profile, with its ratio projected above 62%, as expenses continue to weigh on operating leverage.

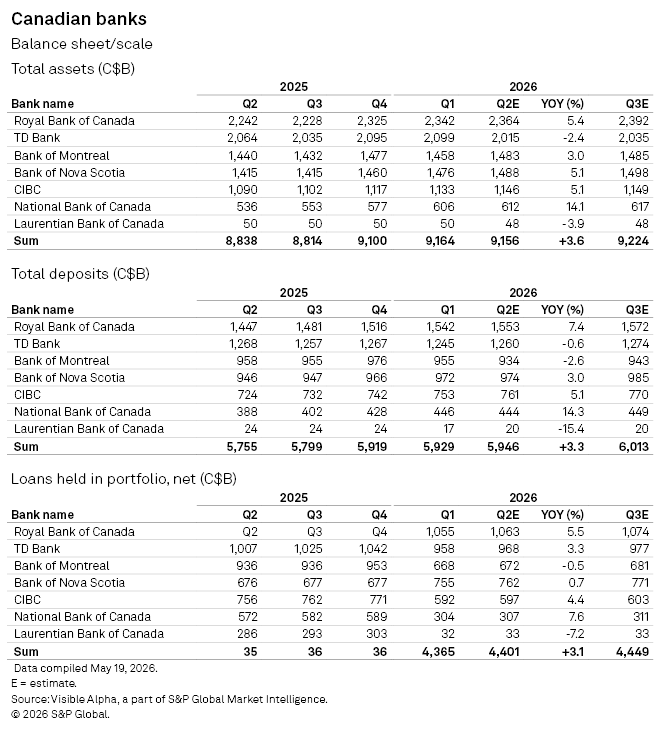

Balance sheet and scale: Broad-based growth to support earnings, led by National Bank expansion

Analysts expect steady growth in assets, deposits, and loans across the group continuing to support NII resilience despite moderating margins. Across the group, total assets are expected to grow 3.6% year-on-year, with deposits up 3.3% and loans in portfolio rising 3.1%. Consensus expectations suggest a broadly supportive volume backdrop, even as pricing power normalizes in a lower-rate environment. However, growth is increasingly uneven across institutions, with clear leaders and laggards emerging.

National Bank of Canada stands out as the strongest growth franchise in the sector, with total assets expected to rise 14.1% year-on-year, deposits up 14.3%, and loans up 7.6%. This outsized expansion continues to reflect both strong organic momentum in its core Quebec and commercial banking businesses and the ongoing integration of Canadian Western Bank, which is materially boosting scale and deposit depth. While the initial acquisition-driven step-change occurred in 2025, Q2 2026 reflects a full-quarter contribution and continued balance sheet build-out.

RBC is also expected to deliver solid expansion, with assets, deposits, and loans growing mid-single digits year-on-year. In contrast, TD Bank is expected to see modest contraction in total assets (-2.4%) and flat deposit growth, even as loan growth remains positive at 3.3%.

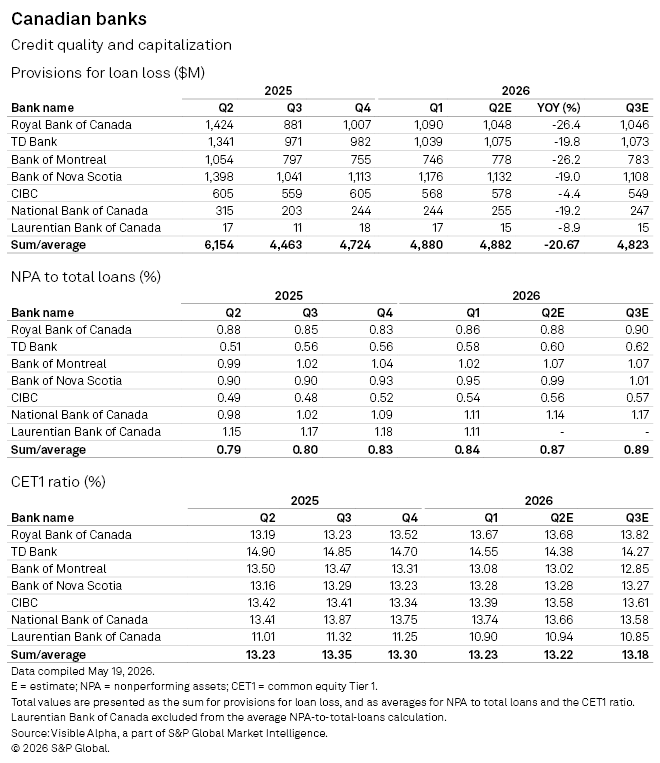

Credit quality: Stable credit trends and strong capital buffers to support sector resilience

Credit quality across Canadian banks is expected to remain broadly stable in Q2 2026. Sector-wide provisions for loan losses are expected to decline by ~21% year-on-year. At the same time, average NPA ratios are expected to gradually drift higher, suggesting a mild deterioration in asset quality but no signs of systemic stress. Importantly, CET1 ratios remain strong across the group, providing ample capital flexibility for dividends, buybacks, and balance sheet growth.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Theme

Products & Offerings