Research — May 29, 2026

Optical and IP momentum to push Nokia network revenues up 14% in 2026

By Anas Kapadia

Nokia Oyj (HEL: NOKIA) has emerged as one of the standout performers in European telecoms this year, with its shares rising more than 140% year-to-date to about $16 as of May 26, as sentiment pivots towards the group’s growing role in AI-driven network infrastructure.

The inflection point came in October 2025, when Nvidia invested $1 billion in Nokia at $6.01 per share, taking roughly a 3% stake. The partnership centers on AI-RAN, which integrates AI workloads directly into radio access networks, positioning Nokia at the intersection of telecoms and accelerated computing. T-Mobile US Inc. has already signed on as the first deployment partner, lending early commercial credibility to the initiative.

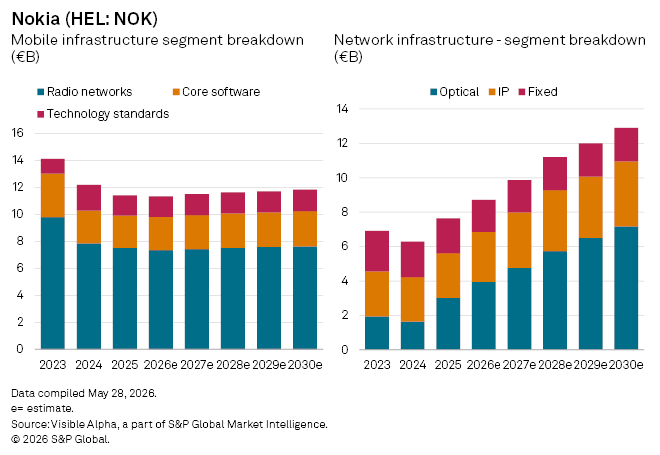

Momentum has since been reinforced by Nokia’s first-quarter results, which highlighted a sharp divergence within its business mix. Optical network infrastructure revenues rose 56.4% year-on-year to €821 million, driven by hyperscaler demand for data center connectivity as companies scale AI capacity. This strength offset broader weakness elsewhere, lifting total network infrastructure revenues 12% to €1.8 billion despite declines across more traditional segments.

According to Visible Alpha estimates, Nokia’s optical networking revenues are expected to increase 31% year-on-year to €4 billion in 2026, while IP networking is projected to grow 12% to €2.9 billion. Together, these gains are set to push total network infrastructure revenues up 14% to €8.7 billion. By contrast, the group’s core mobile networks division is expected to remain under pressure, with revenues seen edging down 1% to €11.3 billion.

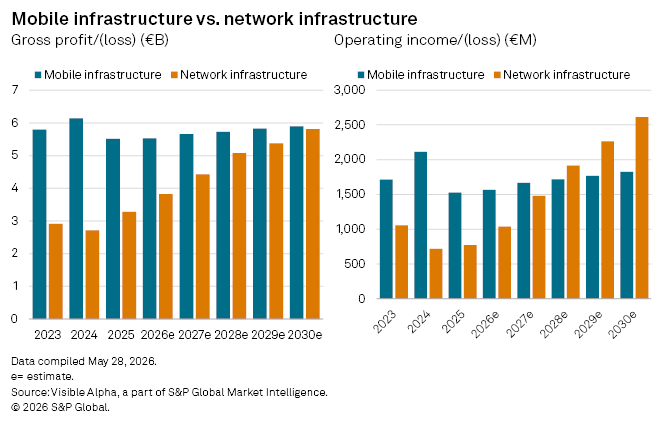

Profitability is also expected to follow the mix shift. Analysts forecast network infrastructure gross profit to rise 16% to €3.8 billion in 2026, with operating income climbing 35% to €1 billion, reflecting both higher-margin optical products and operating leverage from scale.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment