Research — May 14, 2026

Meta postQ snapshot: Ad strength drives beat; AI capex clouds near-term outlook

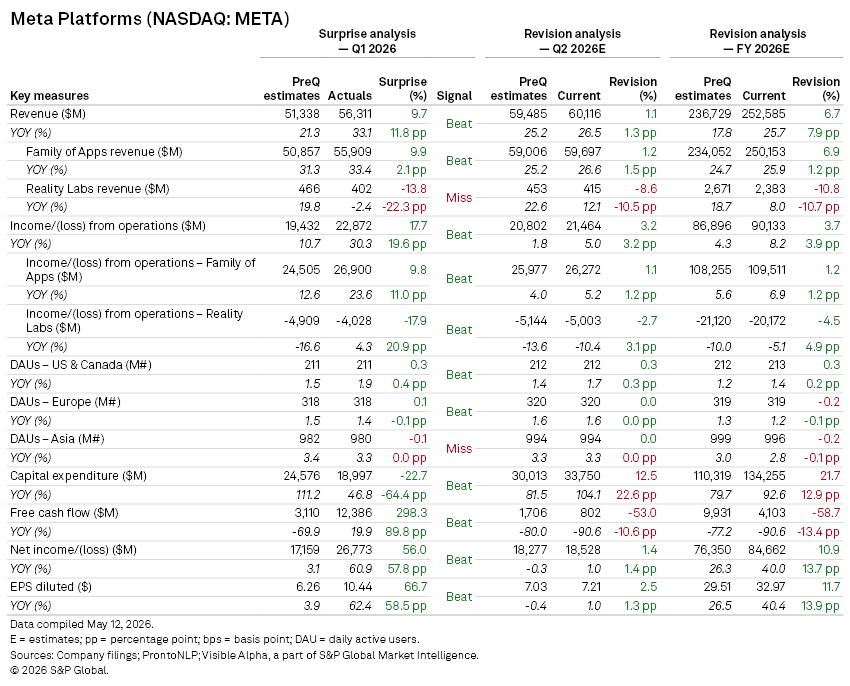

Meta Platforms Inc. (NASDAQ: META) delivered a clear earnings beat in Q1 2026, with numbers across key lines coming ahead of Visible Alpha consensus expectations, driven by robust advertising performance and margin expansion. However, a step-up in full-year AI capital expenditure guidance and mixed user trends tempered investor sentiment

Looking at earnings summaries compiled by S&P Global Pronto NLP, along with Visible Alpha pre-quarter consensus expectations and revised outlook, here are some key takeaways.

Key takeaways

- Revenue rose 33.1% year-on-year to $56.3 billion, ahead of Visible Alpha consensus expectations, while diluted EPS of $10.44 exceeded expectations by a wide margin due to a tax benefit.

- The outperformance was driven primarily by the Family of Apps segment, where revenue of $55.9 billion benefited from stronger ad pricing, improved AI-led targeting, and ongoing monetization gains. Operating profit of $22.9 billion also came in well above expectations, reflecting meaningful operating leverage across the core advertising business.

- Despite this strength, user trends were more mixed. Daily active users in the US & Canada modestly beat expectations, Europe was broadly in line, and Asia slightly underperformed, pointing to increasing maturity in key regions and a shift in focus toward engagement and monetization rather than pure user growth.

- Capital expenditure of $19 billion came in below expectations, largely due to the timing of AI infrastructure investments rather than a strategic pullback. This drove a sharp beat in free cash flow, which reached $12.4 billion versus expectations of $3.1 billion, highlighting strong near-term cash generation.

- Reality Labs remained a drag, with revenue of $402 million missing expectations and declining year-on-year. However, the operating loss of $4 billion was narrower than analysts anticipated.

Guidance

- Management guided Q2 revenue of $58–61 billion, ahead of Visible Alpha pre-quarter expectations, driven by continued strength in advertising demand.

- The key shift came in capital allocation. Full-year 2026 capex guidance was raised to $125–145 billion, above prior guidance and consensus expectations, reflecting an acceleration in AI infrastructure investment and higher component costs.

Analyst Q&A highlights

- Management emphasized that AI-driven improvements in targeting, measurement, and content recommendations are already supporting engagement and advertiser ROI. However, monetization of these investments is expected to scale gradually over a multi-year horizon.

Share price reaction

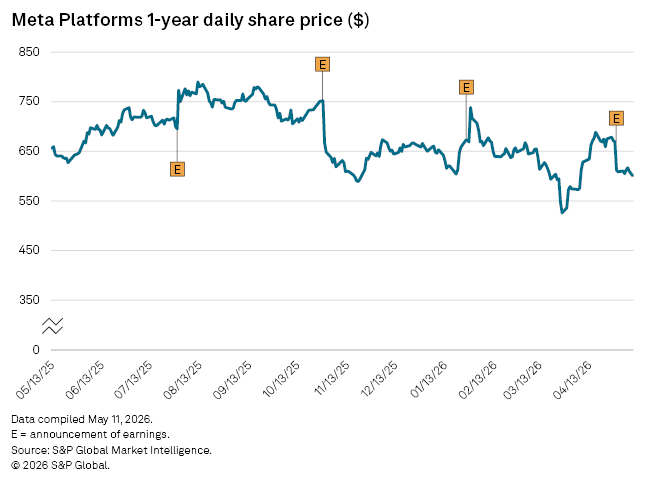

- Shares of Meta declined following the release, as investors focused on the magnitude of the capex increase rather than the earnings beat. The raised AI spending outlook reinforced concerns around the scale, duration, and return profile of incremental investment, with expectations of near-term free cash flow pressure outweighing confidence in current operating momentum.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment