Research — May 15, 2026

McDonald's postQ snapshot: International strength offsets US demand softness

By Dharmang Sapariya

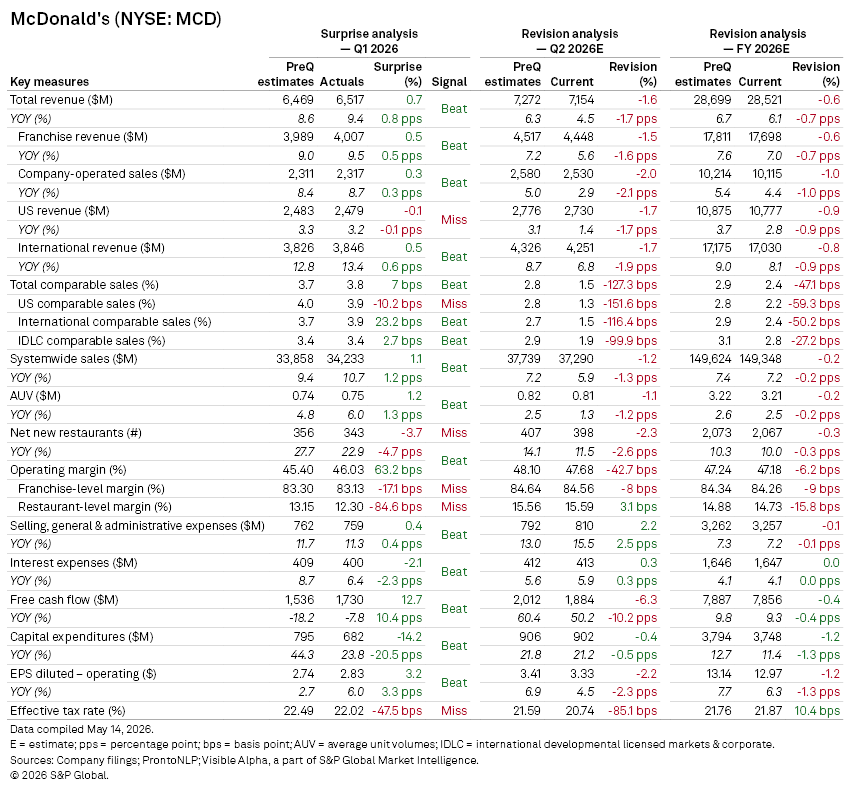

McDonald's Corp. (NYSE: MCD) reported Q1 2026 earnings on May 7 delivering a modest beat with revenue, EPS and margins coming in slightly ahead of Visible Alpha consensus expectations. This was driven by resilient international performance, even as US sales softened and management flagged a more cautious near-term demand backdrop.

Looking at earnings summaries compiled by S&P Global Pronto NLP, along with Visible Alpha pre-quarter consensus expectations and revised outlook, here are some key takeaways.

Key takeaways

- Q1 revenue of $6.52 billion came in modestly ahead of consensus expectations, while diluted EPS of $2.78 beat consensus by 1.6%. Operating margin of 46% also exceeded expectations by ~60bps, reflecting disciplined cost control and the structurally high-margin franchise model.

- System-wide sales rose 11% year-on-year to $34.2 billion, supported by pricing, unit growth and solid comparable sales performance across most international markets.

- Comparable sales trends remained positive but uneven. US comparable sales growth of 3.9% slightly missed consensus expectations, amid softer traffic and increasing value sensitivity among lower-income consumers

- International Operated Markets outperformed, led by strength in the UK, Germany and Australia

- International Developmental Licensed Markets were broadly in line, despite volatility in parts of the Middle East and Asia.

- Average unit volumes rose 6% year-on-year, coming in ahead of expectations and highlighting continued pricing power despite a more cautious consumer backdrop.

- However, profitability at the restaurant level came under pressure, with margins missing consensus due to labor and commodity inflation. Franchisee margins were comparatively more stable, supported by operating leverage and the asset-light model.

- Free cash flow reached $1.73 billion, beating expectations, aided by favorable working capital timing and capex phasing.

Guidance

- The key incremental surprise was on near-term demand. Management guided to a “meaningful deceleration” in Q2 comparable sales following softer April trends, below pre-quarter consensus expectations of ~2.8%.

- However, the broader FY26 framework was broadly reaffirmed:

- Net restaurant additions of ~2,100, implying ~4.5% unit growth

- Operating margin: mid-to-high 40% range (vs ~47% pre-quarter consensus expectations)

- Capex: $3.7 billion–$3.9 billion

- Free cash flow conversion: low-to-mid 80%

- FX tailwind: ~$0.20–$0.30 to EPS

- Management also signaled sequential improvement in comp trends through May and June, aided by easier comparisons.

Analyst Q&A highlights

- Management emphasized continued momentum in McValue, loyalty engagement and beverage innovation as key demand stabilizers.

- At the same time, executives acknowledged:

- Ongoing margin pressure for franchisees from labor, energy and input costs

- Persistent weakness in lower-income consumer cohorts across multiple markets

- Early-stage evaluation of a refreshed US restaurant experience and remodel cycle

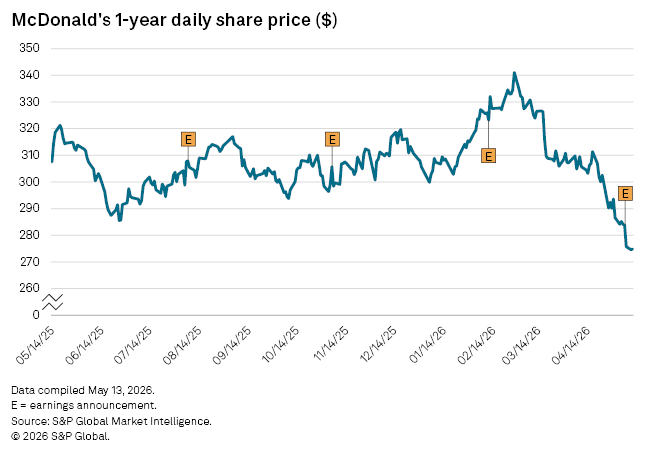

Share price reaction

- McDonald's shares dipped following the earnings reports as investors focused on cautious Q2 comparable sales commentary and ongoing concerns around franchisee economics and consumer spending softness.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings