ECONOMICS COMMENTARY — 08 May, 2026

Global PMI: Europe hit hardest by war impact in April

S&P Global’s PMI surveys for the world’s largest economies reveal the differing impact of the war in the Middle East on economic growth and inflation.

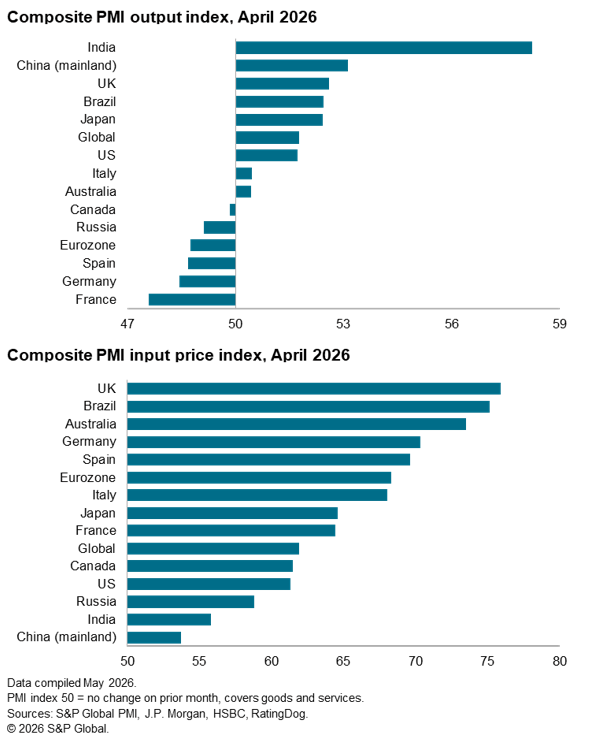

The eurozone nations of France, Germany and Spain have been hardest hit by the war in terms of economic growth, each reporting lower output in April. The UK meanwhile suffered the steepest rise in input costs, widely linked to the war’s impact on energy and shipping prices.

Eurozone hit hardest by war

Mixed trends were seen in the advanced economies during April as economies struggled amid the uncertainty, shortages and price inflation generated by the ongoing war in the Middle East.

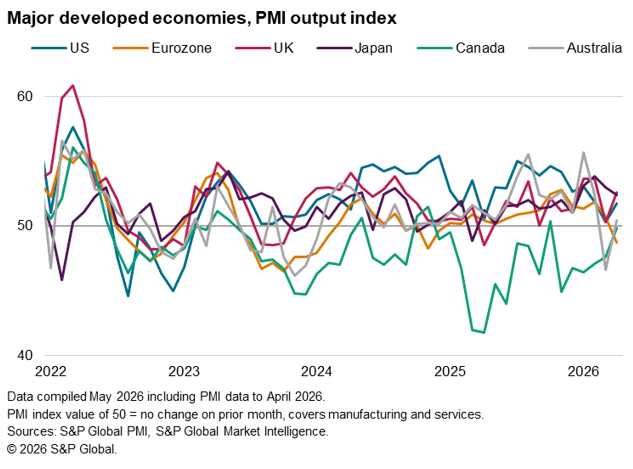

Hardest hit by the war in April was the eurozone, where output fell for the first time in 16 months. A drop in services activity outweighed an improved manufacturing performance. Declines in Germany, France and Spain were joined by only a marginal increase in business activity in Italy.

In contrast, growth rebounded in the US and UK, the latter enjoying the strongest upturn of the major developed economies thanks to improved performances across goods and services. The US expansion was the second-weakest in 14 months, however, as sluggish services growth dragged on manufacturing’s best performance for four years.

While Japan lagged the UK, it outperformed the US despite growth dipping to a four-month low. Although factory output grew at the fastest rate for over 12 years, Japan also saw the smallest rise in services output for nearly a year.

Canada meanwhile remained in a downturn, despite the rate of decline easing to only a marginal rate amid the largest rise in factory output for nearly four years.

Only a marginal gain was seen in Australia which, while a marked improvement on March’s steep decline, was among the slowest recorded over the past year-and-a-half.

Broad-based emerging market improvements

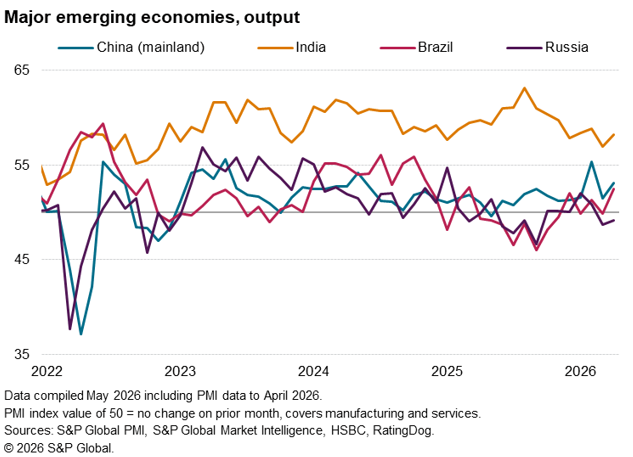

Improved performances were seen across all four ‘BRIC’ emerging economies in April, albeit with Russia merely reporting a reduced rate of contraction.

India remained the strongest performer, with output growth lifting from March’s 40-month low thanks to improved gains across both goods and services.

A notable upturn in growth was also seen in mainland China. Having slowed sharply in March, the expansion hit the second-highest in nearly two years. Faster services growth was accompanied by the quickest rise in goods production since June 2024.

Brazil likewise reported an upturn whereby output rebounded from a slight fall in March to register the steepest increase for just over a year. Both manufacturing and services reported stronger performances.

Output in Russia contracted for a second successive month amid downturns across both manufacturing and services, though at a reduced rate.

Stockbuilding

One caveat to any improved performance in April was the fact that many companies reported improved demand or activity in response to concerns over supply availability or price hikes linked to the war. This precautionary spending therefore represents only a temporary lift to growth which will likely dissipate in the coming months. Clearly, however, much will depend on the duration of the conflict and the associated energy and supply impact.

See our recent manufacturing-focused note to find out more about the impact of this stock building.

UK and Brazil suffer steepest price hikes

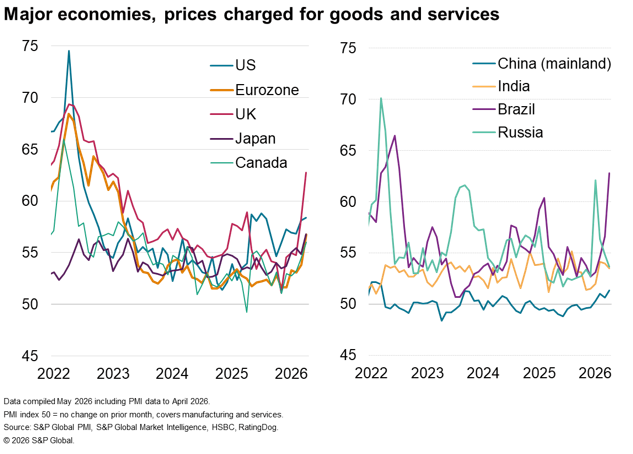

Price hikes linked to the war are already broad-based globally, albeit with varying degrees of impact.

Especially steep rates of charge inflation were recorded in the UK and Brazil, which have both seen unprecedented increases in their PMI selling price indices over the past two months. Rates of inflation hit the highest since January 2023 and July 2022 respectively, in both cases linked to higher rates of both goods and services inflation.

US price growth also remained steep, accelerating to a nine-month high amid stronger goods price inflation and sticky service inflation.

Similar strong rates of increase were meanwhile seen in the eurozone and Japan, with inflation hitting a three-year high in the former while a fresh survey-record was seen in Japan.

Prices also rose sharply in Australia, the rate of increase the highest since August 2022, while in Canada the rate hit its highest since July 2023.

Selling prices rose more modestly by comparison across mainland China, though the rate of inflation was nevertheless the joint-steepest since March 2022 due to higher goods prices.

Inflation rates cooled in both Russia and India due to weaker service inflation.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings