Research — May 14, 2026

Apple postQ snapshot: iPhone 17 demand, Services strength, and margin expansion drive earnings beat

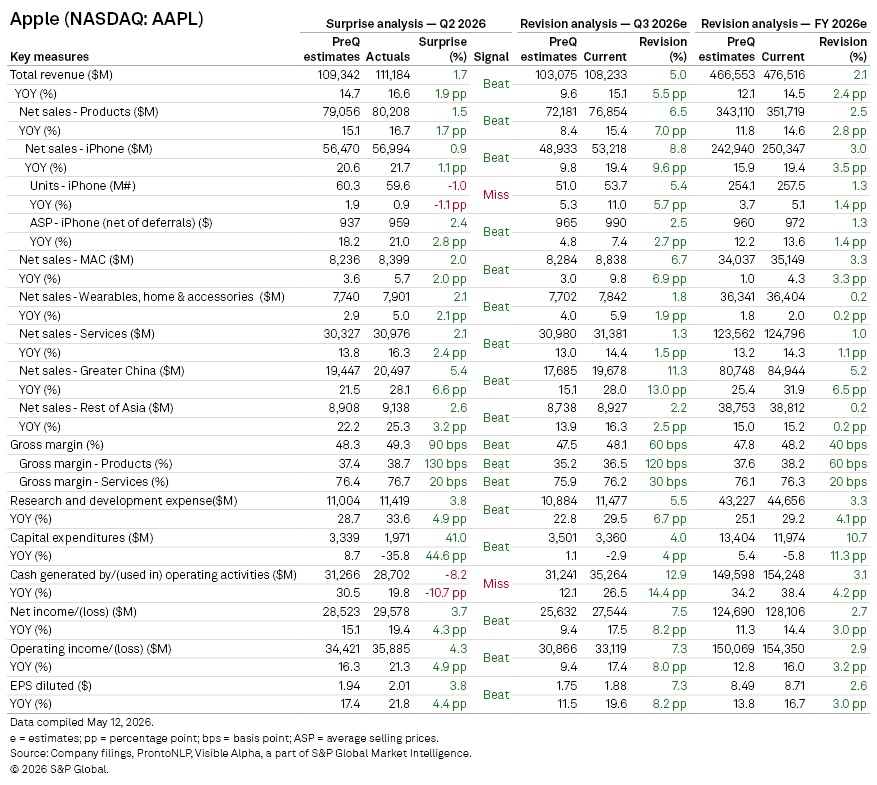

Apple Inc. (NASDAQ: AAPL) delivered a strong Q2 2026 performance, with revenue, earnings, and operating income coming in ahead of Visible Alpha consensus expectations, driven by strong Services revenue, favorable product mix and pricing, expanding gross margins, and continued resilience across the product portfolio despite softer iPhone unit growth and ongoing supply constraints.

Looking at earnings summaries compiled by S&P Global Pronto NLP, along with Visible Alpha pre-quarter consensus expectations and revised outlook, here are some key takeaways.

Key takeaways

- Apple reported revenue of $111.2 billion, increasing 17% year-on-year and coming in ahead of Visible Alpha consensus expectations of $109. 3 billion. Diluted EPS of $2.01 also exceeded expectations, supported by operating leverage, margin expansion, and continued share repurchases.

- iPhone net sales of $57 billion modestly exceeded expectations and increased 22% year-on-year despite supply constraints. Revenue growth continued to benefit from a richer product mix and higher average selling prices, even as unit shipments came in below consensus expectations. Mac and Wearables, Home & Accessories also delivered upside versus expectations, reinforcing broad-based product strength.

- Services revenue reached a record $31 billion in revenue, rising 16% year-on-year and beating consensus expectations by of $30.3 billion.

- Gross margin expanded to 49.3% in Q2, exceeding consensus expectations by 90 basis points.

- Geographically, Greater China was a key standout, with revenue of $20.5 billion beating expectations by 5.4% and growing 28% from last year, driven by robust demand for the iPhone 17 family. The rest of Asia also remained strong, growing by 25% in Q2, pointing to continued momentum across international markets.

- Operating cash flow of $28.7 billion increased 20% year-on-year but came in below consensus expectations, primarily due to working capital timing effects. Capital expenditure declined 36% to $2 billion and was below the $3.3 billion expectations.

- Meanwhile, research and development expenses increased to $11.4 billion, up 34% year-on-year, indicating Apple’s continued investment in AI capabilities and its broader product innovation roadmap.

Guidance

- Management guided to Q3 2026 revenue growth of 14–17% year-on-year, ahead of pre-quarter Visible Alpha consensus expectations of a 10% growth.

- Services revenue growth is expected to remain in line with Q2 levels at roughly 16% after adjusting for FX tailwinds, ahead of pre-quarter consensus expectations of 13%.

- Gross margin guidance of 47.5–48.5% is broadly in line with pre-quarter consensus expectations of 47.8%.

- Management guided operating expenses to $18.8–19.1 billion, above pre-quarter consensus expectations of $18.1 billion, reflecting continued elevated investment in AI initiatives and broader product development efforts.

Analyst Q&A highlights

- Management noted that Q3 guidance already incorporates expected supply constraints across products, alongside significantly higher memory costs, while iPad faces a difficult year-on-year comparison.

- The company attributed iPhone revenue strength despite softer unit growth to a favorable mix shift toward the higher-end iPhone 17 family, with management highlighting “extraordinary” customer demand, though supply constraints limited additional upside.

- Management also highlighted continued year-on-year growth in the advertising business and disclosed that Apple’s installed base expanded to 2.5 billion active devices, reinforcing confidence in the long-term durability of Services growth.

- On margins, management stated that Q2 tariff impacts improved sequentially due to reduced product volumes and the benefit of lower IIFA and Section 122 tariff rates throughout the

Share price reaction

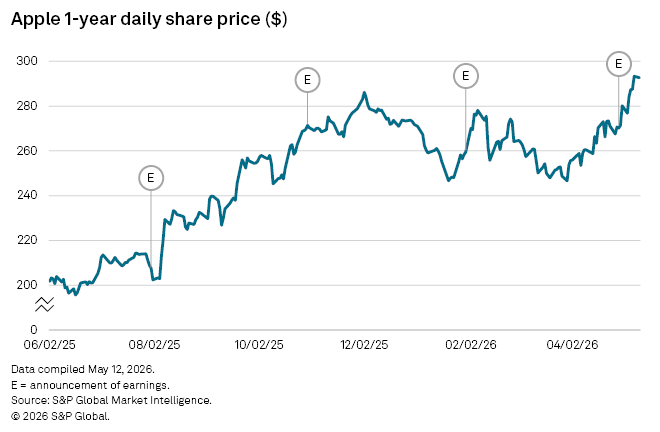

- Investor reaction to the quarter was positive, with shares moving higher following the earnings release as the market responded favorably to record revenue, continued Services momentum, margin expansion, and Apple’s announcement of a new $100 billion share repurchase authorization alongside a dividend increase.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment