Research — May 14, 2026

Airbnb postQ snapshot: International expansion, ADR drive upside; guidance rises

By Dharmang Sapariya

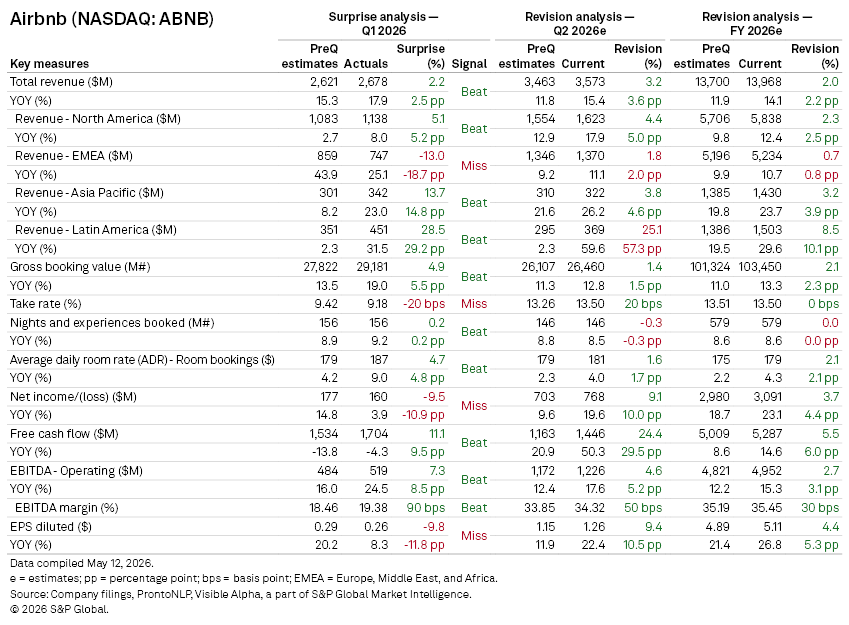

Airbnb Inc. (NASDAQ: ABNB) reported earnings on May 7, with revenue, gross booking value (GBV), and adjusted EBITDA coming in modestly ahead of Visible Alpha consensus expectations, driven by strong average daily room rate (ADR) growth and international expansion. EPS, however, missed analyst expectations.

Looking at earnings summaries compiled by S&P Global Pronto NLP, along with Visible Alpha pre-quarter consensus expectations and revised outlook, here are some key takeaways.

Key takeaways

- Q1 revenue increased 18% year-on-year to $2.7 billion, slightly ahead of $2.6 billion consensus expectations. GBV rose 19% to $29.2 billion, ahead consensus. Adjusted EBITDA of $519 million also exceeded expectations, with EBITDA margin expanding to 19.4%.

- Booking trends remained healthy, with nights and experiences booked rising 9.2% year-on-year to 156 million, broadly in line with expectations. ADR increased by 9% to $187, benefiting from FX tailwinds and growing adoption of the company’s “Reserve Now, Pay Later” offering. Strong ADR performance was a key driver of both revenue and GBV upside.

- Take rate, however, was below expectations at 9.18%, reflecting faster growth in lower-take-rate international markets as well as deferred revenue recognition tied to installment payment products.

- Regional performance highlighted continued momentum outside North America. APAC revenue rose 23% year-on-year to $342 million, significantly ahead of expectations, driven by strong demand across Japan, Korea, and Southeast Asia. Latin America revenue of $451 million also materially exceeded expectations, supported by strength in Brazil and Mexico.

- North America revenue grew 8% year-on-year to $1.14 billion and modestly beat consensus, while EMEA revenue of $747 million missed expectations. Management attributed the softer EMEA result primarily to FX impacts and geographic classification changes rather than underlying demand weakness.

- Net income of $160 million and diluted EPS of $0.26 came in below expectations due to higher interest expense and tax costs, even as underlying operating performance remained strong. Free cash flow generation remained robust, supporting ongoing share repurchases alongside continued investment in AI-driven personalization, search enhancements, and international infrastructure.

Guidance

- Q2 revenue guidance of $3.54–$3.60 billion came in ahead of consensus expectations, implying year-on-year growth of 14–16%. Management expects low double-digit GBV growth, supported by continued nights booked growth and moderate ADR increases.

- The company noted that nights and experiences booked growth is expected to slow modestly in Q2 from Q1 levels, reflecting an estimated 100 basis point headwind from the Middle East conflict. Even so, both adjusted EBITDA and EBITDA margin are expected to increase year-on-year in Q2.

- For full-year 2026, management raised revenue growth guidance to the low-to-mid teens, ahead of consensus expectations.

Analyst Q&A highlights

- Management highlighted strong engagement trends across the platform, driven by improved mobile web-to-app conversion, higher notification opt-ins, and stronger App Store positioning.

- The company also pointed to growing momentum around major global events, with the upcoming World Cup expected to become Airbnb’s largest event to date, while many new hosts acquired during the event are expected to remain active afterward.

- Meanwhile, hotel expansion efforts continue to progress, with management focused on improving merchandising and matching the right inventory to the right users ahead of a broader rollout.

- Reserve Now, Pay Later continues to support booking conversion and gross bookings, with management expecting related take-rate pressure to reverse in the second half of 2026.

Share price reaction

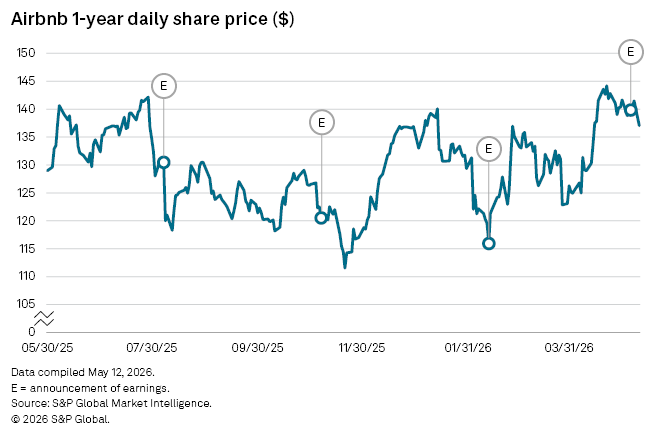

- Shares of Airbnb moved modestly higher following the earnings release, as investors looked past the EPS miss and focused instead on strong revenue growth, improving margins, and raised full-year guidance.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment