Research — May 7, 2026

AI infrastructure results in 2025 top expectations, forecast upgraded

By Greg Macatee

The AI infrastructure market continues to outpace expectations, finishing 2025 with $337 billion in aggregate revenue, according to 451 Research's AI Infrastructure Market Monitor & Forecast. By the end of this decade, we expect the annual market opportunity to exceed the $1 trillion mark for the first time, underscoring the massive potential of AI technologies.

The AI infrastructure race continues as participants across the technology spectrum snap up accelerators, storage, networking, and security tools to support model training, fine-tuning, deployment and operationalization. While this dynamic has helped grow the market over the last few years, inferencing should sustain it; however, capitalizing on this shift will be no easy feat. While enterprise adoption and technical skillsets continue to expand, organizations still face steep operational and technical roadblocks in realizing the full potential of these technologies.

Enterprise and AI technology vendors will likely face immense pressure to deliver tangible return on investment to justify prolonged investment. Winning in this environment will require constantly driving down token costs — a key dynamic defining the current AI infrastructure landscape. We have already witnessed strategic shifts to capitalize on this, evidenced by increased dealmaking with inferencing trailblazers like Cerebras Systems Inc. and custom silicon rollouts like AWS' Trainium and Microsoft Corp.'s Maia. Still, memory and flash storage shortages, as well as data center power and cooling constraints, remain bottlenecks to large-scale AI infrastructure rollouts.

Context

We define AI infrastructure as the hardware, software and services-based technical foundation supporting AI and machine learning life cycles. It enables organizations to collect, manage and process their data in order to build, train and refine models; leverage data sources; and perform inference. AI infrastructure may be internally or externally facing, powering products and services across consumer and business-to-business markets. It also underpins other core markets that we track, such as generative AI and accelerated computing-as-a-service (ACaaS).

Our AI Infrastructure Market Monitor & Forecast (MMF) sizes the AI infrastructure market from 2025 to 2030. Results are based on a bottom-up, supply-side analysis and interviews of 163 participating vendors, combined with proprietary company modeling and Visible Alpha estimates. We verify these results with demand-side inputs from our knowledge base and user insight from our Voice of the Enterprise surveys.

The AI infrastructure market represents a massive opportunity, totaling $4.8 trillion over the forecast period. Annual revenue is projected to grow rapidly, scaling from $337 billion in 2025 to $1.2 trillion by 2030 (a compound annual growth rate of 28%). While these figures reflect substantial ongoing AI infrastructure investments by model builders, hyperscalers and neoclouds, we anticipate enterprise buyers will contribute an increasingly larger share of revenue over time as they build and scale their AI capabilities.

Workload categories

Demand for inferencing — using trained and fine-tuned models to generate new predictions, insights and content based on previously unseen prompts — continues to surge. Inferencing also underpins advanced technologies such as agentic AI, which allows software to act semi- or fully autonomously on behalf of users. As organizations increasingly shift from early generative AI pilots to enterprise-wide deployments of autonomous agents, we expect the resulting spike in continuous model execution will amplify AI infrastructure demand throughout the forecast.

Driven by this shift, inferencing will likely act as the market's primary growth driver over the next several years, with associated revenue projected to climb from $101 billion in 2025 to $532 billion in 2030 (39% CAGR). By comparison, model training and fine-tuning workloads are expected to boost AI infrastructure revenue from $127 billion to $336 billion over the same period (21% CAGR). We project that the inferencing opportunity will overtake training and fine-tuning in 2027. Additionally, AI infrastructure spending to support data ingestion, integration and preparation is forecast to expand from $109 billion in 2025 to $295 billion in 2030 (22% CAGR).

Infrastructure components

Hardware, software and ACaaS components form the foundation of an AI infrastructure stack. AI infrastructure hardware primarily consists of accelerators like GPUs, application-specific integrated circuits and other custom silicon, but it also extends to foundational system components such as CPUs, memory, storage drives and arrays, and networking equipment. As the market evolves, AI infrastructure software is increasingly co-engineered and deployed alongside inference servers and runtime environments. While software makes up a relatively small portion of total market revenue, its qualifying revenue includes stand-alone products (as opposed to those bundled with system purchases) sold via commercial subscriptions, licenses and maintenance agreements.

ACaaS primarily consists of GPU-as-a-service offerings, as well as other immediate and necessary storage and networking services. We have expanded our market definition to account for other types of cloud-based accelerated instances (e.g., those powered by Trainium, Maia and Google Cloud's Ironwood). Because these customized chips are engineered to support the ultra-bandwidth and low-latency requirements of real-time inference workloads, they should serve as a major driver for ACaaS as user adoption and demand for real-time inferencing grow.

Hardware is expected to continue contributing the most AI infrastructure revenue over the next several years, growing from $298 billion in 2025 to $946 billion in 2030 (26% CAGR). While software should expand more rapidly — increasing from $19 billion to $72 billion over the same period (31% CAGR) — it starts from a smaller numerical base. ACaaS should emerge as the market's fastest-growing segment, expanding from $20 billion in 2025 to $145 billion in 2030 (48% CAGR).

Regions

Our AI infrastructure regional revenue forecast maps to where infrastructure deployments are physically located or where ACaaS is consumed. We expect strong performance globally as users continue to adopt AI technologies and deploy agents and other inferencing workloads. North America should remain the largest market, increasing from $201 billion in 2025 to $632 billion in 2030 (26% CAGR). Over the same period, Latin America is projected to be the fastest-growing market, expanding from $2 billion to $14 billion (43% CAGR). Europe, the Middle East and Africa should be the second-fastest-growing region, climbing to $157 billion from $36 billion (34% CAGR). Asia-Pacific revenue should increase from $97 billion to $360 billion (30% CAGR).

We expect that growth outside of North America will be bolstered by a wave of new AI data center announcements and infrastructure projects. For example, in late March 2026, France-based Mistral AI SAS raised $830 million in debt financing to purchase 13,800 NVIDIA GB300s and secure up to 44 megawatts of capacity in a data center in Bruyères-le-Châtel, near Paris. Similarly, Nebius Group NV, a Dutch neocloud, announced the construction of a new AI factory in Lappeenranta, Finland, with up to 310 MW of capacity. In Asia-Pacific, initiatives such as the Japanese government's planned ¥10 trillion ($63 billion) investment in the semiconductor and AI industries should drive sustained growth through the end of the decade.

As user adoption and technical proficiency grow, these investments will support the market's enormous inferencing opportunity while closely aligning with global digital sovereignty efforts. By increasing visibility and control over hardware and software stacks, digital sovereignty allows organizations to de-risk against technical and supply chain uncertainties. It also drives improved privacy, compliance and governance — a trend especially pronounced in EMEA following legislation like the US CLOUD Act. In response, hyperscalers and neoclouds are actively expanding their sovereignty portfolios and local data center presences. Crucially, this localized control over data exposure benefits non-English AI initiatives — because leading foundation models are predominantly trained in English, localizing model training and fine-tuning is essential for ensuring both linguistic accuracy and cultural relevance.

Forecast changes

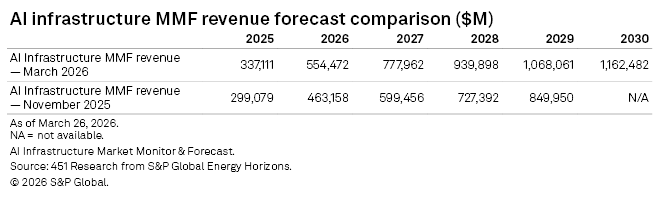

For context, discussion of our previous market results can be found here. We have upgraded our forecast based on several key market developments. Since our last publication, leading vendors have consistently outperformed their financial guidance, which informed our prior forecast. The size and velocity of funding rounds and M&A activity have also exceeded expectations, particularly among cloud service providers and GenAI model builders that are heavy consumers of AI infrastructure. We are also tracking a global wave of new AI infrastructure projects characterized by massive power commitments, often ranging from hundreds of megawatts to over a gigawatt per deployment.

Driven by these factors, we have upgraded our AI Infrastructure MMF five-year forecast, increasing the collective AI infrastructure market opportunity through the end of the decade by 25% compared with our previous estimates. Notably, forecast revenue in both 2029 and 2030 now exceeds $1 trillion.

451 Research from S&P Global Energy Horizons provides technology industry research, data, and advisory solutions. For more information or to contact us, please visit 451 Research.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Language