Research — April 20, 2026

UnitedHealth faces muted Q1 growth as regulatory pressures cloud outlook

By Mohd Naim

UnitedHealth Group Inc. (NYSE: UNH) is set to report first-quarter 2026 earnings on April 21 against a subdued backdrop, with consensus forecasts pointing to a near-stagnant top line and mounting policy headwinds.

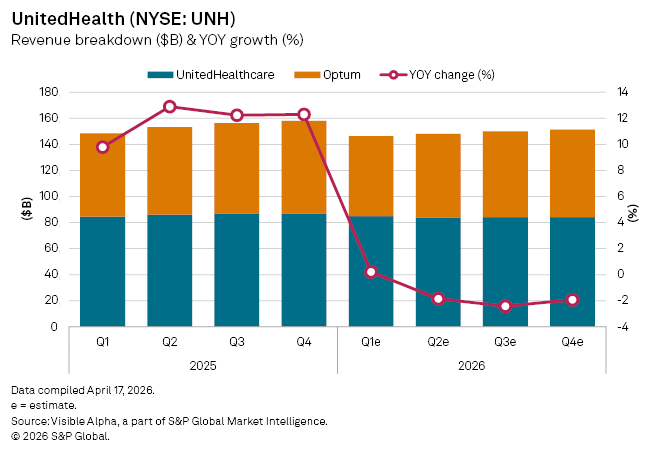

According to Visible Alpha estimates, revenues are expected to edge up just 0.2% year-on-year to $109.8 billion, while declining 3% sequentially, an unusually soft trajectory for a company that has historically delivered consistent high-single-to-double-digit growth. The performance reflects slower momentum across both its core insurance and services businesses.

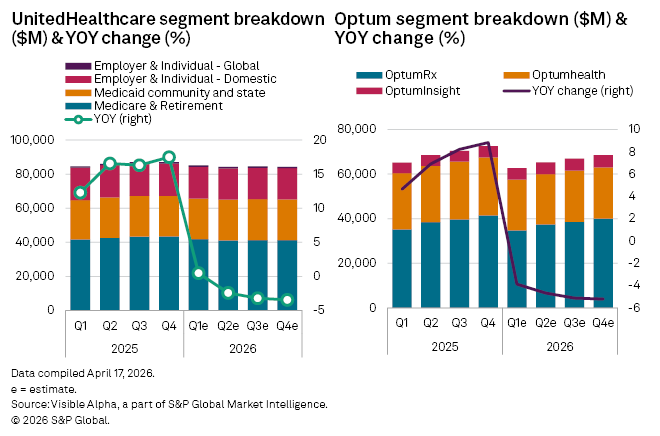

Within its main division, UnitedHealthcare, revenues are projected to rise a modest 0.5% to $85 billion, with total membership falling to an estimated 51 million (from 54 million last year). Meanwhile, Optum revenue is expected to see a decline of 4% to $61.4 billion.

The muted operating outlook comes amid a broader deterioration in market sentiment. Shares in UnitedHealth are currently down 24% over the past year, reflecting concerns over slowing enrolment in Medicare Advantage and Medicaid plans, which are key drivers of volume growth. At the same time, the group faces intensifying regulatory scrutiny of its Optum unit and its pharmacy benefit manager operations, areas increasingly targeted by policymakers seeking to curb healthcare costs.

There are, however, tentative signs of relief. A proposed 2.48% increase in Medicare Advantage reimbursement rates for 2027, above earlier expectations, has offered some support to the sector, hinting at a more favorable policy environment ahead. Even so, for 2026, UnitedHealth appears to be navigating a more constrained growth landscape.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment