Research — May 5, 2026

Tesla postQ snapshot: Margin strength offset by demand softness and heavy capex

By Nitin Mirajkar

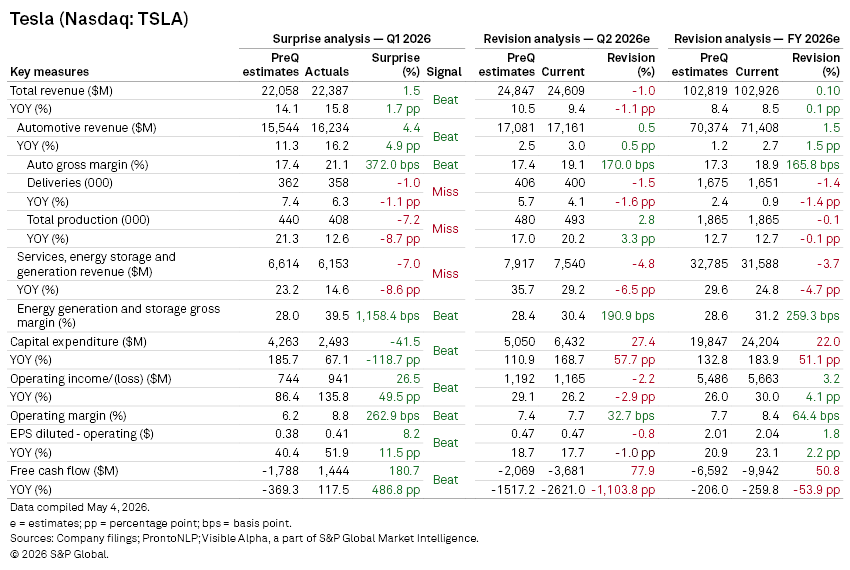

Tesla Inc. (NASDAQ: TSLA) delivered a headline beat in Q1 2026, with profitability exceeding expectations even as volumes disappointed and forward guidance signaled a sharp step-up in investment intensity.

Looking at earnings summaries compiled by S&P Global Pronto NLP, along with Visible Alpha consensus pre-quarter expectations and revised outlook, here are some key takeaways.

Key takeaways

- Revenue of $22.4 billion came in modestly ahead of Visible Alpha consensus expectations, supported by stronger-than-expected automotive sales, while diluted EPS (operating) of $0.41 also beat expectations. The quality of the beat, however, leaned heavily on margins rather than underlying demand.

- Automotive gross margin (including credits) reached 21.1%, 372 bps ahead of consensus expectations, driven by lower manufacturing costs and one-off tailwinds from warranty and tariff adjustments. Energy margins were even stronger, though boosted by a ~$250 million one-time benefit. Operating margin of 8.8% similarly exceeded expectations by 262.5 bps.

- By contrast, volumes were softer. Deliveries of 358K units missed consensus slightly, while production undershot more meaningfully, reflecting continued demand weakness in China. This was partially offset by a rebound in Europe, with France and Germany showing sharp sequential growth, suggesting a geographically uneven demand environment.

Guidance

- The key shift in the quarter came from guidance. Management raised 2026 capex expectations to over $25 billion, well above prior consensus and roughly triple 2025 levels, marking an aggressive investment phase for the company. The spending will be directed toward AI infrastructure, autonomy, robotics (Optimus), dedicated robotaxi platforms, and battery capacity. As a result, the company flagged likely negative free cash flow for the remainder of the year.

Analyst Q&A highlights

- Optimus 3 production is set to begin late July, August with a gradual ramp.

- Full self-driving is targeted for late 2026, contingent on safety validation.

- Robotaxi monetization in 2026 is expected to be limited, with more meaningful revenue impact likely from 2027 as scaling and regulatory approvals progress.

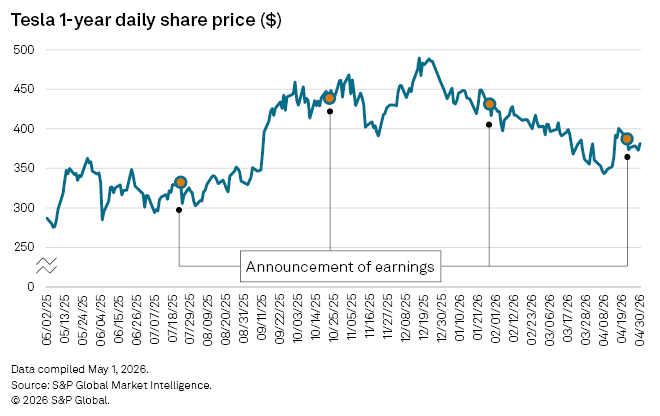

Share price reaction

- Investor reaction reflected this mix. Shares initially rose on the earnings beat but reversed during the call, with the market increasingly focused on the magnitude of capex and execution risk around AI and autonomy investments.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment