Research — April 20, 2026

Tesla faces challenging Q1 as deliveries miss estimates

By Nitin Mirajkar

Tesla Inc. (NASDAQ: TSLA) is due to report first-quarter 2026 earnings on Wednesday, April 22, facing a testing backdrop after two consecutive years of declining deliveries and intensifying competition from Chinese rivals such as BYD Company Ltd. and Xiaomi Corp.

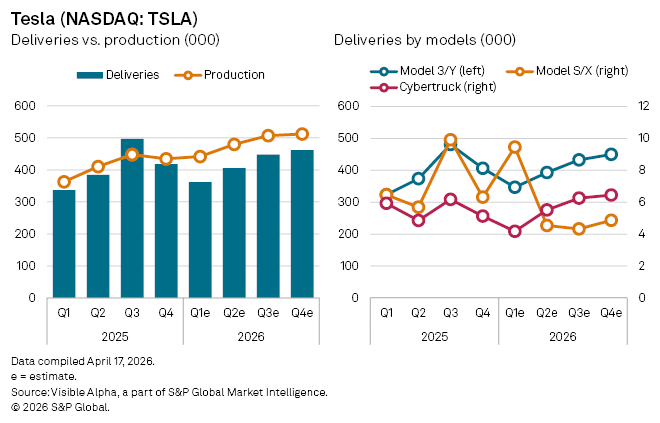

Tesla has already flagged a soft start to the year. The company reported Q1 deliveries of 358,023 vehicles, missing Visible Alpha consensus estimates of 362,000. Deliveries of its core Model 3 and Model Y vehicles, which account for the bulk of volumes, totaled 341,893, also below expectations of roughly 347,000, as the company faces continued pressure in the mass-market segment.

The weakness comes amid a shifting policy landscape in the US, including the rollback of federal tax incentives for EVs, as well as mounting pricing pressure globally. Tesla has also been contending with slowing demand growth and rising competition in key markets, particularly China.

There are, however, pockets of resilience. Consensus estimates point to a 46% year-on-year increase in deliveries of higher-end Model S and Model X vehicles to 9,464 units, partially offsetting declines elsewhere, including softer Cybertruck volumes.

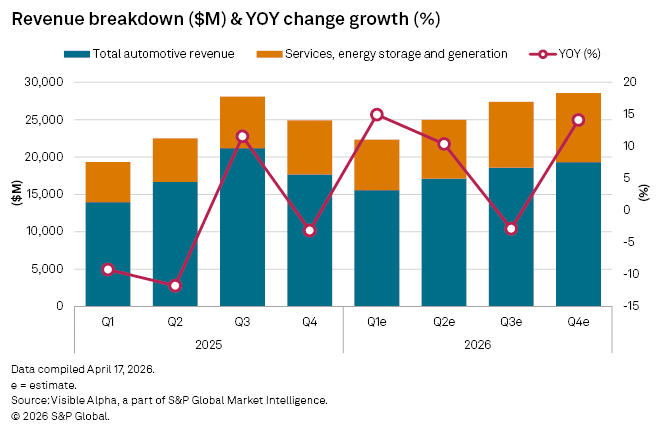

Financially, automotive revenue is expected to rise 11% year-on-year to $15.6 billion, though this marks a 12% decline from the previous quarter, reflecting both lower volumes and pricing headwinds. By contrast, Tesla’s energy, storage and other businesses continue to gather momentum, with revenue forecast to grow 27% year-on-year to $6.8 billion, an increasingly important offset as the core automotive division loses traction.

Overall, group revenue is projected at $22.2 billion for the quarter, up 15% from a year earlier, yet down 11% sequentially. While near-term prospects for vehicle sales remain subdued, Tesla’s energy segment is projected to see growing momentum and provide a more durable growth engine.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment