Research — April 24, 2026

Microsoft and Meta earnings previews

By Melissa Otto, CFA

The strong investment growth in technology infrastructure to support generative AI (GAI) has been a focus over the past year and is projected to expand this year. The expectations for CapEx spending by the hyperscalers continues to move higher. For 2026, consensus year-over-year CapEx is expected to increase by almost $250 billion from $379 billion to $622 billion. The much stronger pace of the expected CapEx to support the technology infrastructure for AI has caused some concern as the significant ramp in spending is projected to grow faster than revenues. Will Meta Platforms Inc. (NASDAQ: META) and Microsoft Corp. (NASDAQ: MSFT) maintain their capex guidance this year?

Microsoft

According to Visible Alpha consensus, total revenues expected for Q3 have remained stable since late October 2025, driven by a resilient view of its core business segments. However, the new Azure AI Services segment is projected to increase for FY 2026, with consensus estimates now expecting $23.4 billion, up from $18.8 billion last January. Expectations for this segment in Q3 2025 have edged up since October and nearly 25% since early 2025. Profitability is also expected to remain resilient for the Company, driving EPS expectations for the quarter and full year up.

We are closely watching what the company will say about the outlook for Azure and OpenAI, as Microsoft’s FY 2026 CapEx numbers have continued to increase steadily. According to consensus projections, CapEx estimates are expected to double from $65 billion in FY 2025 to currently $130 billion in FY 2027.

Microsoft stock has traded down 21% since the last earnings release. The consensus P/E for 2027 has come down from 31x in July and is now 22x. Could the Q3 release and outlook begin to drive outperformance in the stock?

Meta Platforms

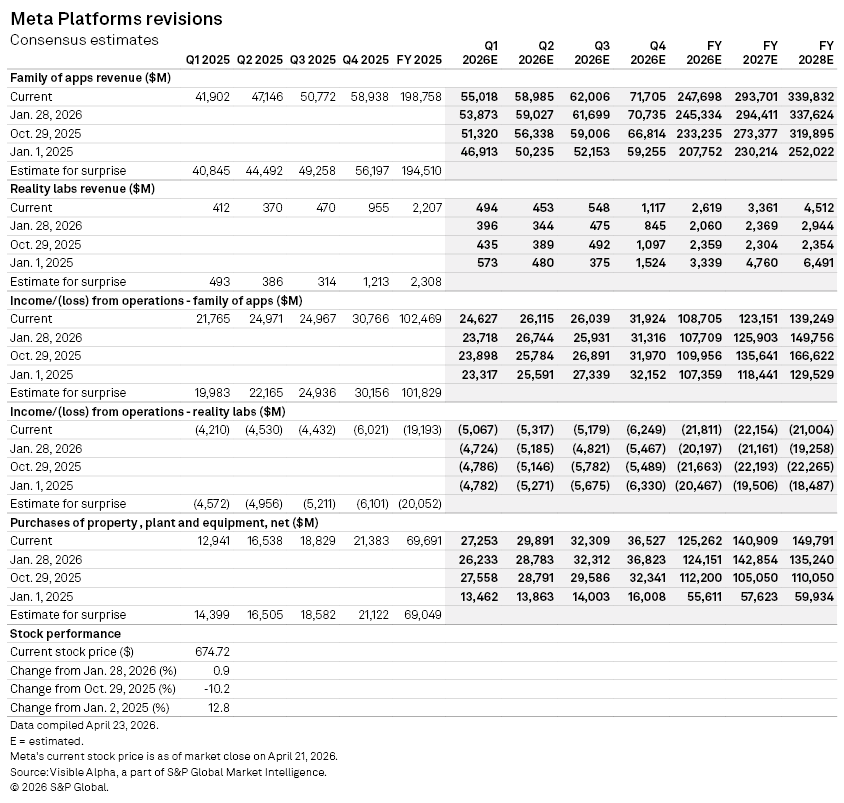

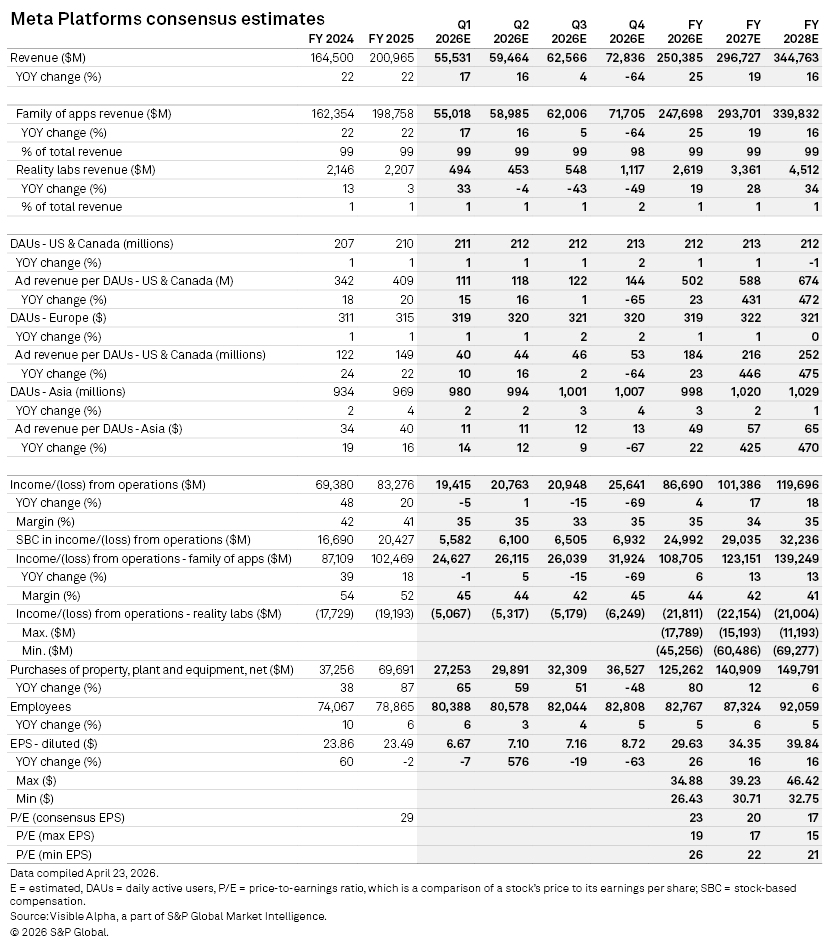

According to Visible Alpha consensus, total revenues for Q1 are expected to be $55.5 billion, driven by solid performance in the Family of Apps segment, especially in the US and Europe. Operating profit is expected to be $19.4 billion, driven by steady profitability in the Family of Apps and consensus losses remaining around -$5.0 billion for Reality Labs.

For 2026, earnings expectations for operating income from the Family of Apps have increased $1.0 billion to $108.7 billion, but down from $110.1 billion in the fall, driven by slightly shifting views about ad revenue per DAU in the US and internationally. The management commentary on the outlook in the earnings call will be key to assessing the potential direction of revisions for 2026. In addition, the projected losses from Reality Labs for 2025 have remained and recently ticked back up for 2026 to -$21.8 billion, driven by continued anticipated losses in the division.

In Q1 2025, CEO Mark Zuckerberg highlighted that the company planned to invest in servers and data centers to support AI. CapEx consensus of nearly $125 billion for FY 2026 is a year over year increase of $55 billion from FY 2025. There are questions about whether Meta will maintain their CapEx this year.

META stock has been underperforming since last October and is down 10.9%. The consensus P/E for FY 2027 dropped to 19x from 21x last year. Will Meta be able to deliver a profit surprise in Q1 2026 and begin to outperform?

Content Type

Products & Offerings