Research — May 6, 2026

Cytokinetics rallies on late-stage Myqorzo data, strengthening sales outlook

By Mehak Sharma

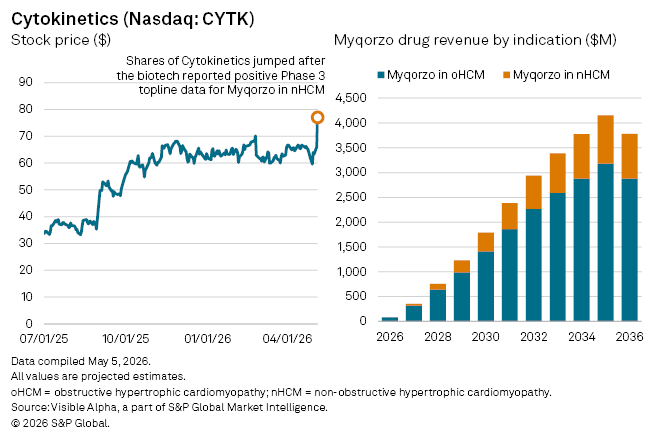

US biotech Cytokinetics Inc. (NASDAQ: CYTK) saw its shares surge on Tuesday, May 5 after reporting positive Phase 3 results for its cardiac therapy Myqorzo (aficamten) in patients with symptomatic non-obstructive hypertrophic cardiomyopathy (nHCM), broadening the drug’s potential beyond its initial niche.

The treatment is already approved across the US, EU and China for the obstructive form of the disease (oHCM), marking the company’s first commercial product following a December approval. Management said it plans to present detailed trial data at an upcoming medical meeting and engage with the US FDA and other regulators on a potential label expansion.

Visible Alpha consensus estimates show analysts expect Myqorzo to generate $83 million in sales in 2026 from oHCM alone, its first year on the market. Sales are expected to rise to $318 million by 2028 and reach blockbuster sales of $1.4 billion by 2030. Peak sales in the oHCM indication are projected at $3.3 billion by 2038.

In nHCM, where approval is anticipated in 2027, risk-adjusted sales are currently projected at $37 million for 2027, climbing to $115 million by 2028. Analysts currently assign a 70% probability of success for Myqorzo in nHCM.

Longer term, analysts see Myqorzo’s combined peak global sales at roughly $4.5 billion by 2039, positioning the drug as the dominant driver of Cytokinetics’ revenue base.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment