Research — March 19, 2026

Xiaomi’s Q4 growth to cool as core devices falter; EV momentum to accelerate

By Kanika Garg

Xiaomi Corp. (SEHK: 1810) is set to report its fourth-quarter 2025 results on Tuesday, March 24, with growth expected to moderate as weakness in its core hardware divisions offsets a surge in EVs.

Visible Alpha consensus estimates point to revenue of CN¥118.5 billion for the quarter, up 9% year-on-year, a marked deceleration from the 22% rise recorded in the previous quarter.

The drag is expected to come primarily from Xiaomi’s smartphone and IoT and lifestyle segments, with revenues forecast to decline 11% and 13% respectively. In smartphones, a combination of waning consumer demand, aggressive promotional activity, heightened competition from domestic peers and rising memory costs are all weighing on performance.

Smartphone shipments are projected at around 40 million units in Q4, down from 43 million in the prior quarter and 7% lower year-on-year, while year-on-year average selling prices are expected to fall 4% to CN¥1,156.

Within IoT, the weakness appears particularly acute in personal computing, where laptop shipments are expected to plunge as much as 49% year-on-year to roughly 214,000 units.

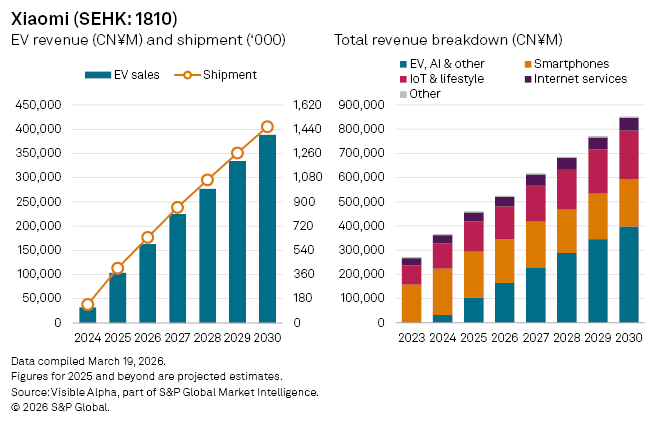

Set against this softness is the company’s rapidly scaling EV business, which continues to emerge as a key growth engine. Smart EV, AI and other new initiatives revenues are forecast to surge 119% year-on-year to CN¥36.5 billion in the quarter, driven by EV shipments growth of 102% and average selling price growth of 8%.

For the full year, revenues are expected to rise 26% to CN¥459.5 billion. Much of this growth is being driven by the smart EV, AI and other new initiatives segment, which is projected to contribute CN¥105.4 billion to group revenue. By contrast, the smartphone division, still Xiaomi’s largest business, is expected to post a modest 2% decline to CN¥188.4 billion, while the IoT and lifestyle segment is forecast to grow 20% to CN¥125.4 billion.

The rapid expansion of Xiaomi’s newer businesses is reshaping its revenue mix. The smart EV, AI and other new initiatives segment is expected to overtake the IoT division in 2026 and become the company’s largest revenue contributor by 2027, accounting for 37% of group revenue, up from just 9% in 2024. The performance reflects Xiaomi’s aggressive push into China’s crowded but fast-growing EV market, where it is seeking to leverage its brand and ecosystem advantages.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings