ECONOMICS COMMENTARY — 30 Mar, 2026

Week Ahead Economic Preview: Week of 30 March 2026

The following is an extract from S&P Global Market Intelligence's latest Week Ahead Economic Preview. For the full report, please click on the 'Download Full Report' link.

PMI surveys to track war impact, US payrolls for added policy guidance

The week ahead features worldwide manufacturing PMI data, providing insights into the impact of the war in the Middle East on factory business conditions. US nonfarm payrolls and eurozone inflation data will also provide key inputs into policy decision making.

The release of worldwide PMI surveys will provide the first global overview of the economic impact of the war in the Middle East on the manufacturing sector. Flash PMI data, released 24 March, have provided early insights, revealing an unwelcome combination of slower economic growth and rising inflation, thereby hinting at stagflation risks. The jump in manufacturing input cost inflation among the largest developed economies was the sharpest on record, linked to the energy price spike but also reflecting the increasingly concerning supply chain delays (see box on right).

The coming week will add PMI data for a host of other economies beyond those tracked by the flash surveys, notably in the Middle East and Asia Pacific, the former being more directly involved in the conflict via Iran’s retaliatory strikes while the latter will be important to watch given their dependence on trade through the Strait of Hormuz.

While Easter holidays push many service sector PMI releases into the following week, updates to service sector conditions in mainland China, Japan and Russia are also scheduled for Friday, with eyes on how rising energy prices in particular have affected demand.

The war comes at a time of existing signs of economic weakness in the United States, notably a softer than anticipated GDP reading for the fourth quarter and disappointing employment growth. Hence the updated nonfarm payroll report for March will be eagerly assessed to gauge whether the US job market might be deteriorating further to help keep alive any hopes of Fed rate cuts amid the worsening inflation outlook. Payrolls fell by 92,000 in February, while the unemployment rate rose to 4.4%.

The two Fed speeches will also help judge how the Fed is balancing upside inflation risks against the soft job market.

The European Central Bank has meanwhile adopted a hawkish tilt, with President Christine Lagarde stating that rate hikes could be considered as early as April due to the rise in price pressures seen since the outbreak of war. Provisional eurozone inflation numbers for March, due Tuesday, could be crucial in steering any such decision.

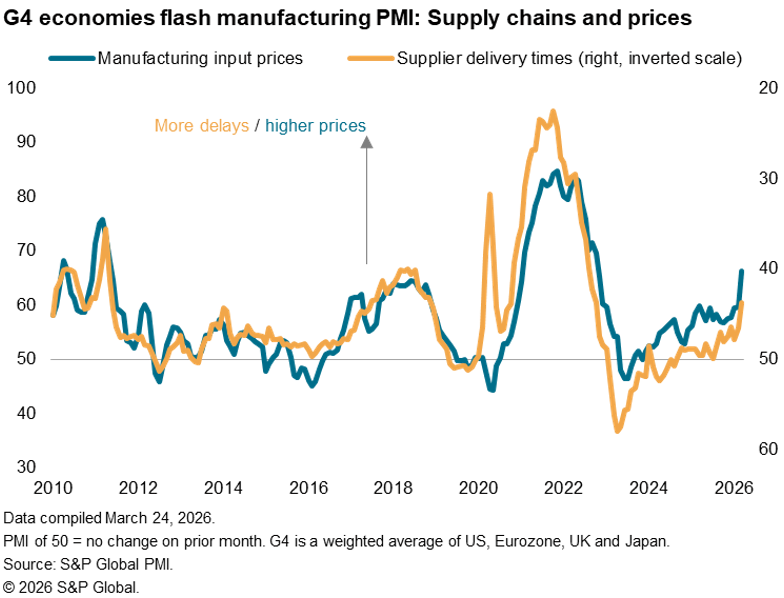

Chart of the week: Business costs surge higher on outbreak of war

The S&P Global flash PMI surveys showed a steep increase in price pressures during March. Manufacturers across the G4 developed economies (the US, Eurozone, UK and Japan) collectively reported the sharpest rise in input costs since October 2022. The jump in costs in the manufacturing sector was notable in being the largest recorded since comparable G4 data were first available in mid-2007.

Input cost increases could be largely attributed to the spike in energy prices seen since the US-Israeli attacks commenced at the end of February, but a more lasting inflationary impact could become evident if supply conditions worsen. Longer supplier delivery times were already reported on average across the G4 economies to a degree not seen since October 2022, being most prevalent in Europe.

Although far less widespread than witnessed at the height of the pandemic, a concern is that any further lengthening of supply lead times will exert additional upward pressure on prices as demand exceeds supply. Supply constraints, especially for energy, will also limit economic growth.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings