ECONOMICS COMMENTARY — 25 Mar, 2026

G4 flash PMIs signal war stress as economies report slower growth and higher inflation

S&P Global’s flash PMI data showed output growth slowing in all four largest developed economies in March following the outbreak of war in the Middle East. Inflationary pressures meanwhile picked up across the board to signal a growing risk of the global economy moving into a period of heightened stagflation risk.

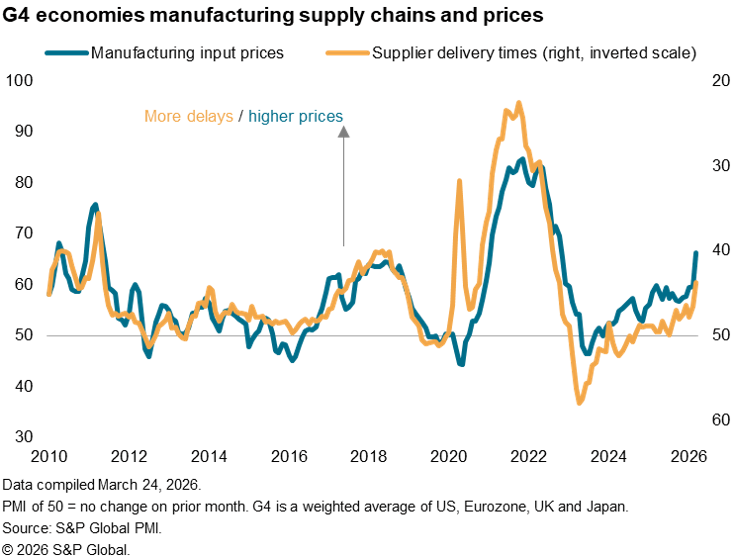

The degree to which stagflation may become a problem for policymakers will depend principally on the duration of the conflict in the MENA region, with signals tracked by the PMI’s survey gauges measuring firms’ output, input costs and supply chain delays – the latter providing a valuable insight into the degree to which scarcities are likely to drive up inflation further and constrain economic growth in various economies. March saw delivery delays become more widespread, though have so far remained modest compared to the pandemic.

Growth slows on outbreak of war

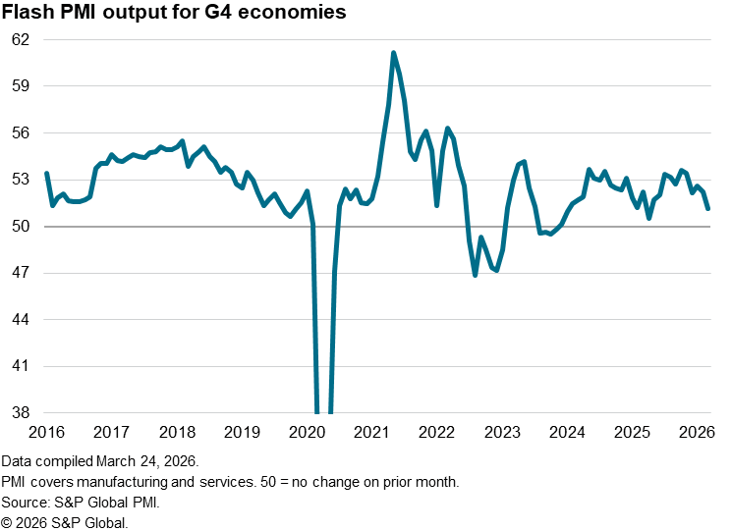

Business activity growth across the four largest developed economies – the ‘G4’ – slowed in March to its weakest since the announcement of US tariffs in April of last year, according to S&P Global’s flash PMI data. The data provide the first indication of the war in the Middle East having had an immediate and material impact on global economic growth.

At 51.2, down from 52.2 in February, the output index for the G4 economies remained in expansion territory but was the one of the lowest reading for just over two years, with only last April’s index having been lower.

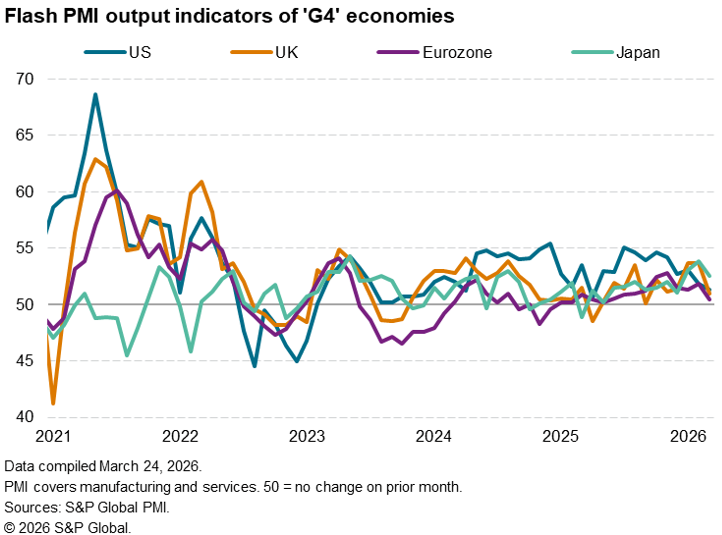

All four largest developed economies reported slower growth. Japan’s upturn proved the most resilient, with output merely rising at the slowest rate for three months. But growth sank to an 11-month low in the US, a ten-month low in the eurozone and a six-month low in the UK.

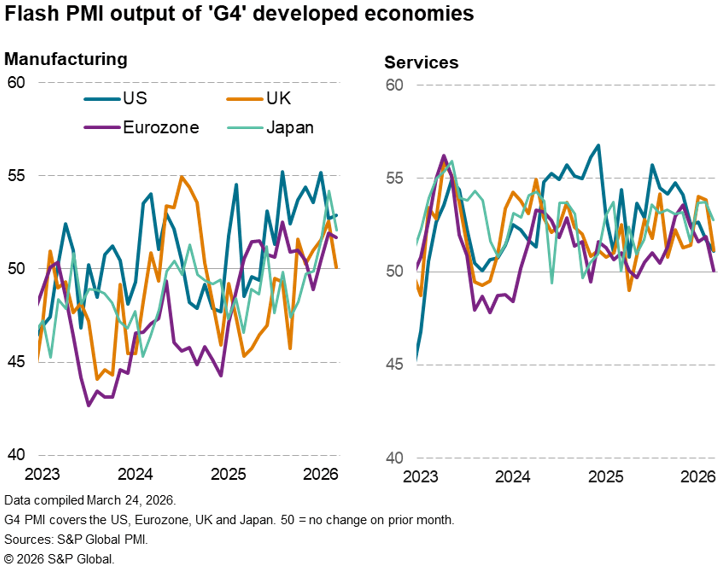

By sector, the slowdown was most evident across the G4 for services, where output rose only modestly and at the weakest rate since last April. Especially disappointing service growth was reported in the eurozone, where the expansion was only marginal, but the US, UK and – to a lesser degree – Japan all also reported slower service sector upturns.

Manufacturing proved more resilient at the G4 level, the aggregate upturn losing only a little momentum to register the third strongest monthly gain seen for almost four years. US manufacturing growth even ticked higher, contrasting with weakened upturns elsewhere, and with the UK reporting an especially marginal increase.

All four largest developed economies reported slower growth. Japan’s upturn proved the most resilient, with output merely rising at the slowest rate for three months. But growth sank to an 11-month low in the US, a ten-month low in the eurozone and a six-month low in the UK.

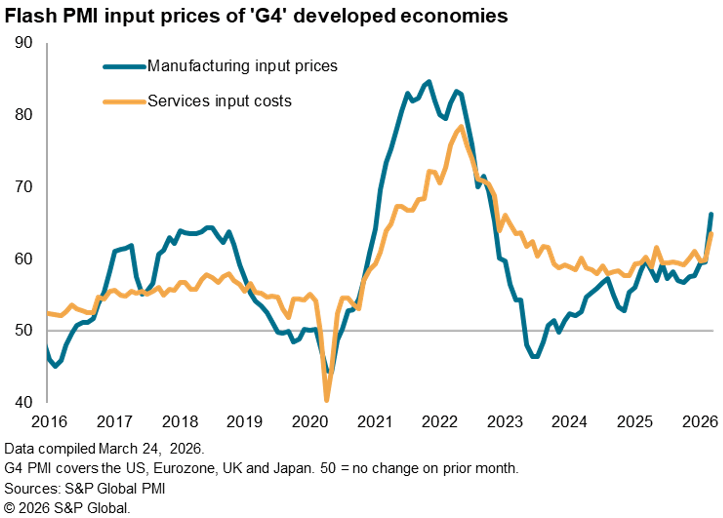

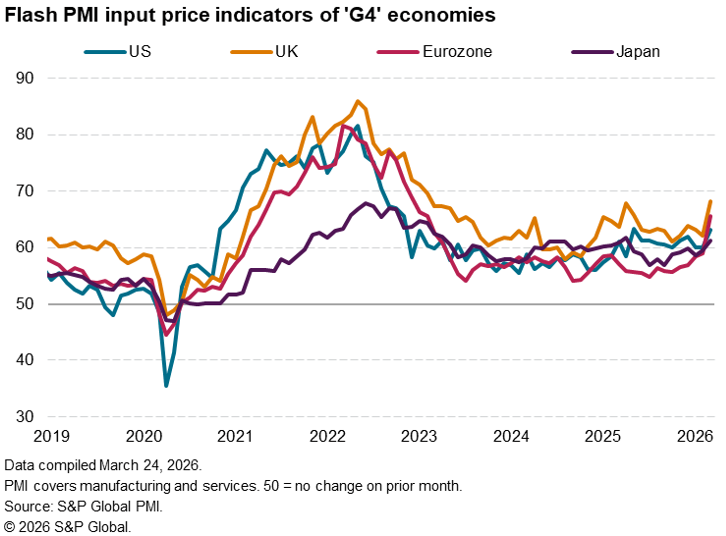

G4 manufacturing input cost inflation shows record surge

The flash PMI surveys also showed a steep increase in price pressures during March. Measured across goods and services, input costs rose among the G4 economies at the fastest rate since January 2023. Service sector costs increased at a rate not seen since April 2023 while manufacturers reported the sharpest cost increase since October 2022. The jump in manufacturing inflation was notable in being the largest monthly change recorded since comparable G4 data were first available in mid-2007.

Measured across both goods and services, input costs rose particularly steeply in the UK, where the rate of inflation hit the highest since February 2023, but also accelerated sharply in the US (to the joint highest since November 2022) and in the eurozone (to the highest since February 2023), with a more muted rate of increase in Japan (to the highest since last April).

Supply concerns

Input cost increases could be largely attributed to the spike in energy prices seen since the US-Israeli attacks commenced at the end of February, but a more lasting inflationary impact could become evident if supply conditions worsen amid the de facto closure of the Strait of Hormuz.

Longer supplier delivery times were reported on average across the G4 economies to a degree not seen since October 2022, being most prevalent in Europe. Although far less widespread than witnessed at the height of the pandemic, a concern is that any further lengthening of supply lead times will exert additional upward pressure on prices as demand exceeds supply for key commodities beyond oil and LNG, including agricultural commodities to affect food supplies.

The feed-through of higher priced, or scarcer, oil derivatives to plastics and chemicals will also be important to monitor, as well as increased prices linked to short supply situations for some metals such as aluminium and sulphur dependent metals, and building materials.

The disruption to container transport and shipping more broadly could also lead to a further worsening of the global supply situation, albeit depending to a large extent on the duration of the conflict in the MENA region. The suppliers’ delivery times index will provide perhaps the most important gauge of this supply-inflation mechanism, as well as the degree to which production capacity and growth may be constrained. Read more about the PMI Suppliers’ Delivery Times Index here

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings