Research — February 23, 2026

Nvidia earnings preview: Q4 2026

By Melissa Otto, CFA

Nvidia’s Q4 2026 earnings preview

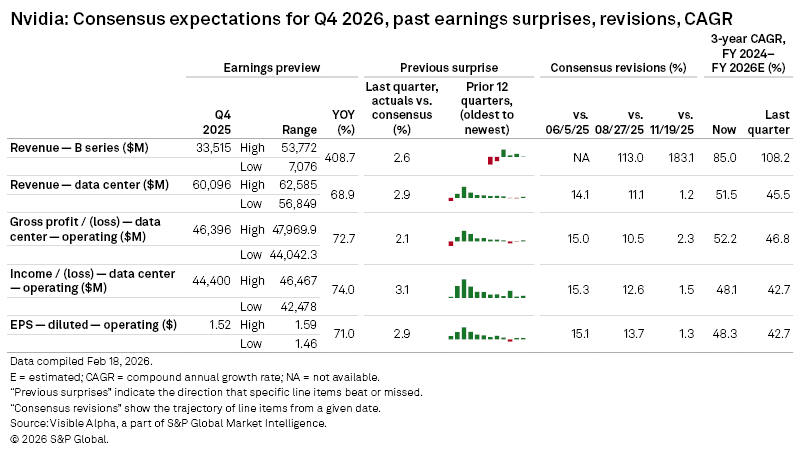

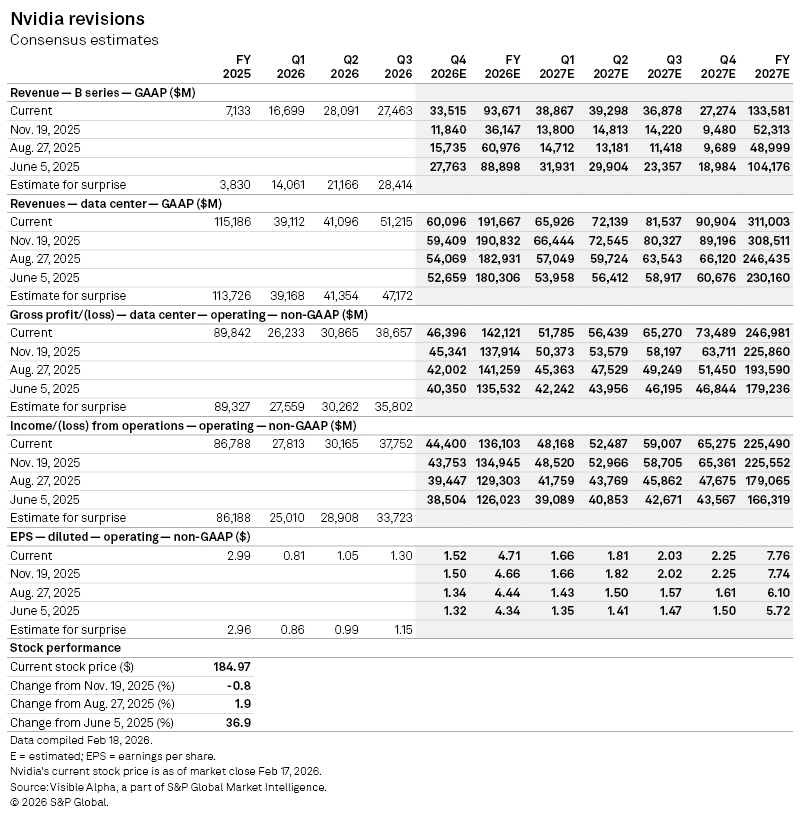

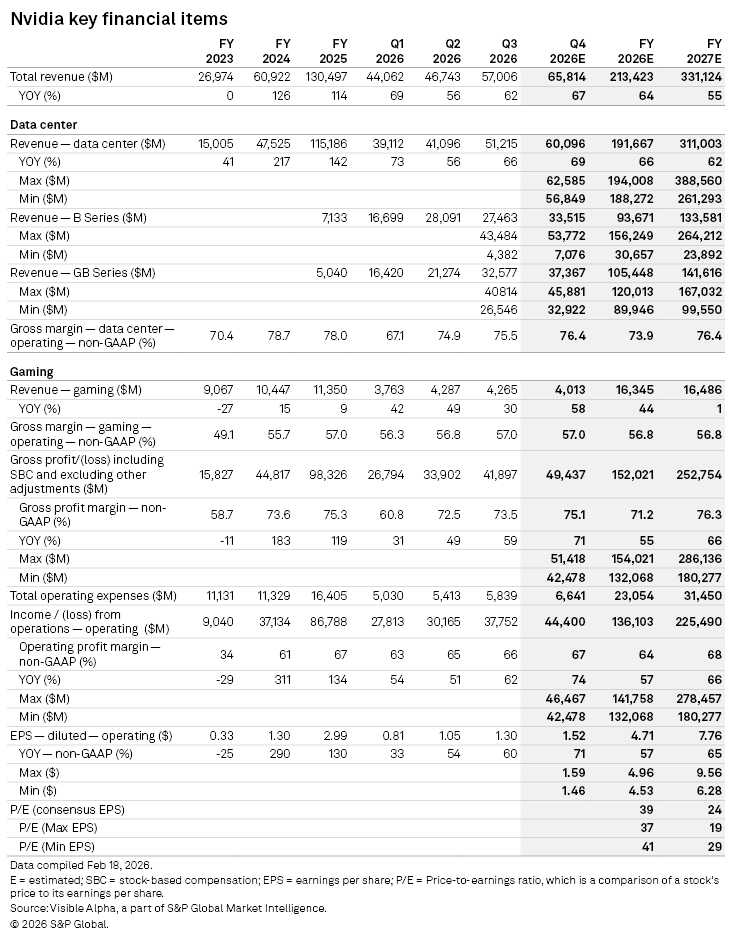

According to Visible Alpha consensus, NVIDIA Corp.'s (NASDAQ: NVDA) total revenues for fiscal Q4 2026 is expected at $57.0 billion. Overall revenue growth continues to be driven by optimism about the strength of Nvidia’s Data Center segment. This segment has seen its expected top-line performance for Q4 increase from $52.7 billion in June 2025 to its current projection of $60.1 billion, up almost 15%. However, recently, the Data Center segment’s expected revenues for Q4 moderated since the November quarter. Based on Visible Alpha consensus, Data Center revenue estimates in Q4 2026 range from $56.9 billion to $62.6 billion.

The expected revenue growth continues to be driven by strong demand for its GPUs from cloud service providers, and the move to accelerated computing in the data centers for AI. However, there are questions around the outlook for Nvidia’s new solution, Blackwell, that claims to significantly reduce energy consumption and cost for customers. There have been concerns about the timing of Blackwell’s growth and the total addressable market (TAM) for this solution. The debate is captured in the range of revenue estimates for the B-series. From 15 sources, these forecasts range from $7.1 billion to $53.8 billion in Q4 with consensus at $33.5 billion.

Due to differing views about the potential and ramp for Blackwell, there is debate about the performance of the Data Center segment going forward. Blackwell revenue is expected to jump from around $7.1 billion last year to $93.7 billion this year. It will be important to see Q4’s Blackwell performance and outlook for Q1 and the rest of FY 2027. The total Data Center revenues for FY 2027 of $311.0 billion have moved higher due to the increase in FY 2027 B-series expectations. The Data Center revenue consensus may be impacted by the higher 31 source count for the Data Center revenues, compared to the 13 sources that provide estimates for the B-series, suggesting some analysts may simply reflect Blackwell in their Data Center estimate instead of breaking it out separately.

For Q4 2026, Visible Alpha consensus for the gross profit of this segment has moved 15% higher from $40.4 billion last June to now $46.4, due to strong demand. It is worth noting that the consensus gross profit margin for the Data Center segment for FY 2027 is projected at 76.4%, reflecting a decline from the 78% levels of FY 2024 and FY 2025. However, the operating profit margin for FY 2027 is projected to move higher from this year’s 63.8% to 68.1%, due to the flat gross margin and lower expenses on significantly higher revenues. These dynamics in consensus margins are causing the expected FY 2027 consensus P/E to be 24x and to range from 19x to 29x.

The stock has traded up 36.9% since the June release but has been down slighly since November, due to concerns about overbuilding for AI. Could the Q4 release and guidance provide the next positive catalyst for the stock or are expectations largely priced in for now?

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment