Research — February 6, 2026

Microsoft vs. Micron: A look at the rotation into memory

By Melissa Otto, CFA

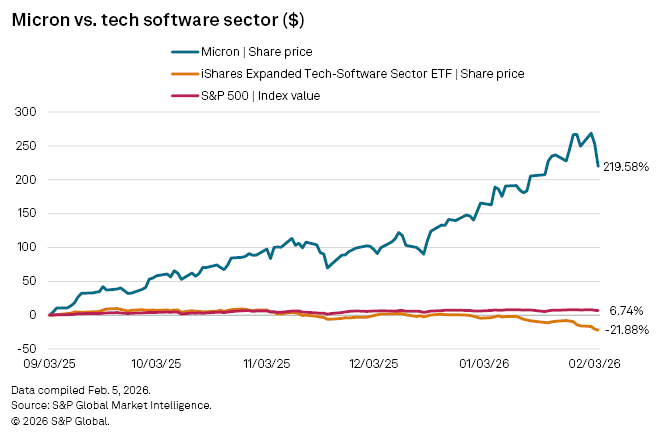

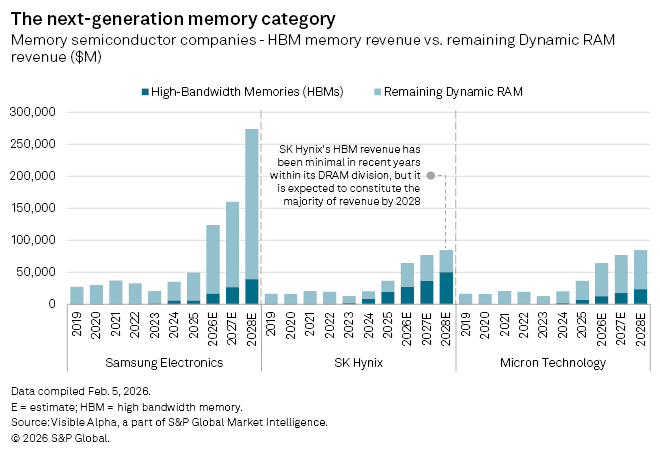

One of the most dramatic market moves around the AI story has been the recent move out of software and into memory stocks. Memory, especially High Bandwidth Memory (HBM), plays an important role in ensuring AI workloads run efficiently and fast, reducing latency. The strength of HBM is that it increases performance by stacking traditional Dynamic Random Access Memory (DRAM) layers vertically, while decreasing the amount of power consumed. As investment in data centers for AI has exploded, demand for memory has become a critical component of AI accelerators, like NVIDIA's Blackwell GB200/B200.

With the surge in demand, memory prices have skyrocketed, causing many investors to question the potential earnings growth of chipmakers and, ultimately, software companies operating in this AI ecosystem. The IGV Technology Software ETF, which includes Microsoft, Palantir, Oracle, Salesforce and ServiceNow, has significantly underperformed the S&P 500 in the past few months, making this an interesting time to revisit the trajectory of consensus for the key drivers. While memory stocks continue to see estimates increase, there are questions about the bottom for software stocks.

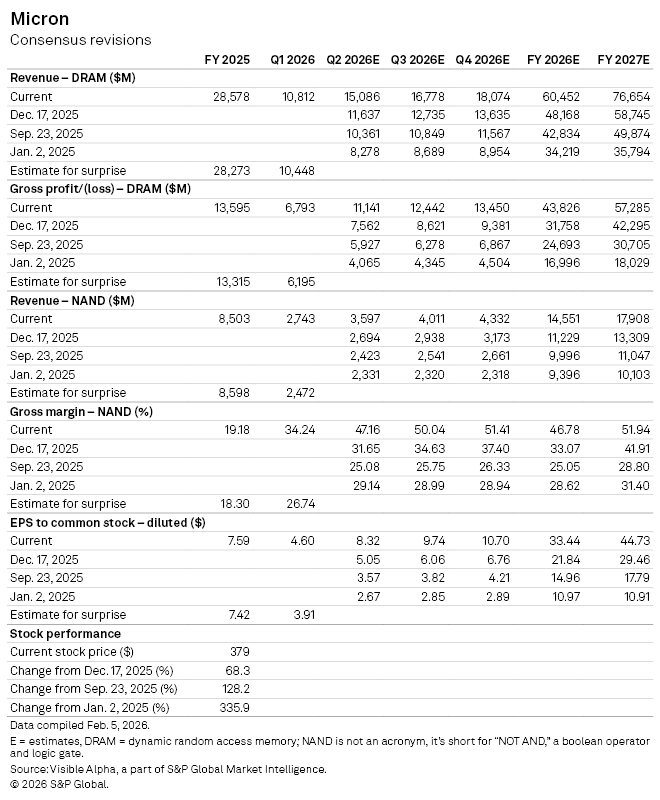

Micron Technology's quarterly estimates for both DRAM and NAND memory sales and gross profit have increased substantially since last quarter. DRAM revenues are now 25% higher for FY 2026 and 30% higher for FY 2027. Gross profit consensus for DRAM has increased more, capturing higher prices and driving full-year 2027 EPS to $45/share or a P/E of 9.3x.

The pace of these upward revisions feels reminiscent of the massive upward revisions we observed in 2023 for Nvidia's data center revenue forecasts for 2024 and 2025. These estimates kept rising due to extraordinary demand from hyperscalers. With Alphabet just announcing its full-year 2026 capex guidance of $175 billion to $185 billion, significantly above the consensus of $120 billion, will this continue to fuel demand and prices for memory?

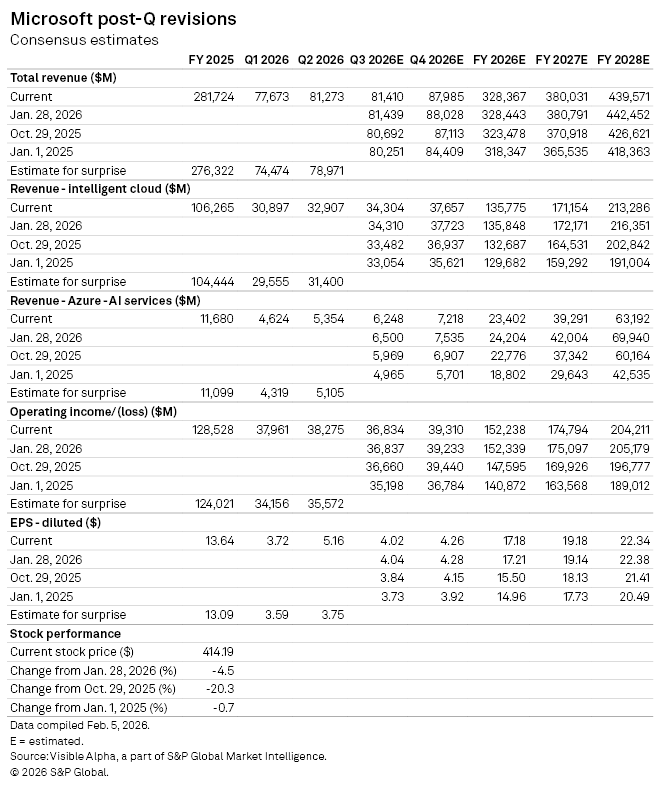

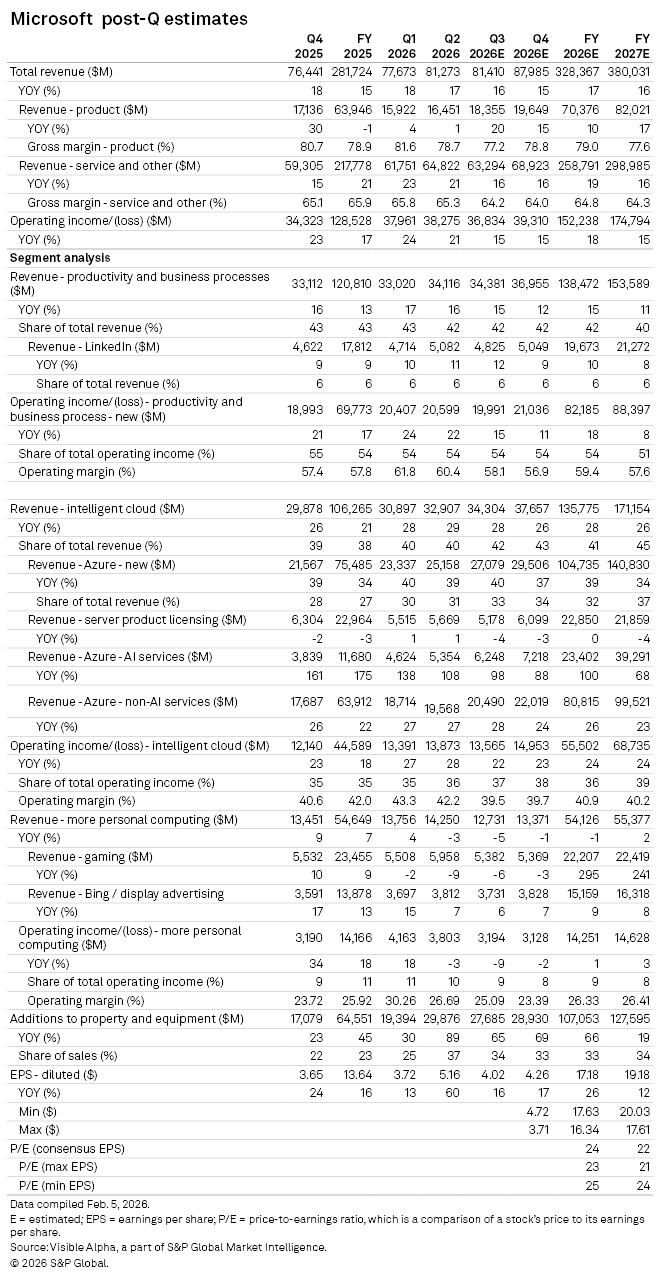

Microsoft's Azure business delivered an in-line quarter and outlook, causing a sell-off in the stock in the past week that has spilled into other related software companies. The reaction seemed surprising since Microsoft delivered 39% revenue growth in the quarter, with 40% expected for the third quarter in Azure. The disappointment came from the lack of upside surprise.

Post second quarter, the Intelligent Cloud revenue remained approximately $34 billion for the next quarter and $135 billion for full year 2026, due to the sentiment around Azure's outlook. More concerning is that the Azure AI segment revenue estimates also have declined since last quarter, suggesting estimates were too high. This lack of a strong growth outlook for its new AI business line is likely to be a disappointment to investors. However, with the stock down nearly 25% since the fall, there are questions about valuation and fundamentals.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment