Research — March 3, 2026

Broadcom Q1 seen up 29% YOY as AI revenue nears $8 billion, margins set to ease

By Ashish Negi

US chipmaker Broadcom (NASDAQ: AVGO) is set to report first quarter fiscal 2026 earnings on Wednesday, March 4, with analysts looking at another strong top-line beat driven by surging demand for AI infrastructure.

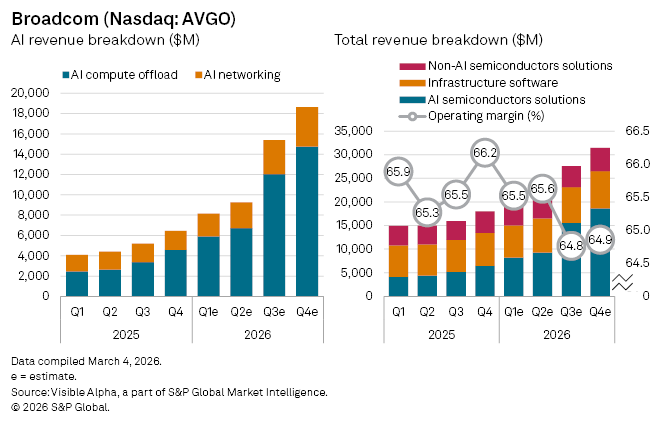

Visible Alpha consensus estimates point to quarterly revenue of $19.2 billion, a 28.7% increase year-on-year, continuing a trajectory that saw the company book a record $64 billion in full-year fiscal 2025 revenue. The AI semiconductor division is the engine of that growth. Revenues from the segment are projected to nearly double to $8.2 billion, with AI compute offload, Broadcom's custom accelerator chips, or XPUs, deployed by hyperscalers including Google, Meta and Anthropic, expected to surge 140% to $5.9 billion. AI networking, which includes the company's high-speed Ethernet switching products, is forecast to grow 37% to $2.3 billion.

Beyond AI, the legacy semiconductor business, covering enterprise networking, server storage and broadband, is showing tentative signs of recovery. Revenues from the segment are projected to grow 1.6% to $4.2 billion in the quarter, a modest but meaningful acceleration from 0.6% growth in the prior period, and a marked improvement on the revenue declines that preceded it.

Broadcom’s infrastructure solutions business is expected to post more subdued growth of 2.5% year-on-year to $6.9 billion.

Profitability is expected to fall short of the pace of top-line momentum. Analysts expect margins to soften as AI silicon and networking outpace high-margin software growth. This dynamic has already influenced trading as Broadcom’s shares slid alongside peers after Nvidia’s recent earnings.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.