Research — February 25, 2026

Alphabet and Amazon earnings review and outlook

By Melissa Otto, CFA

Alphabet Q4 2025 earnings and outlook

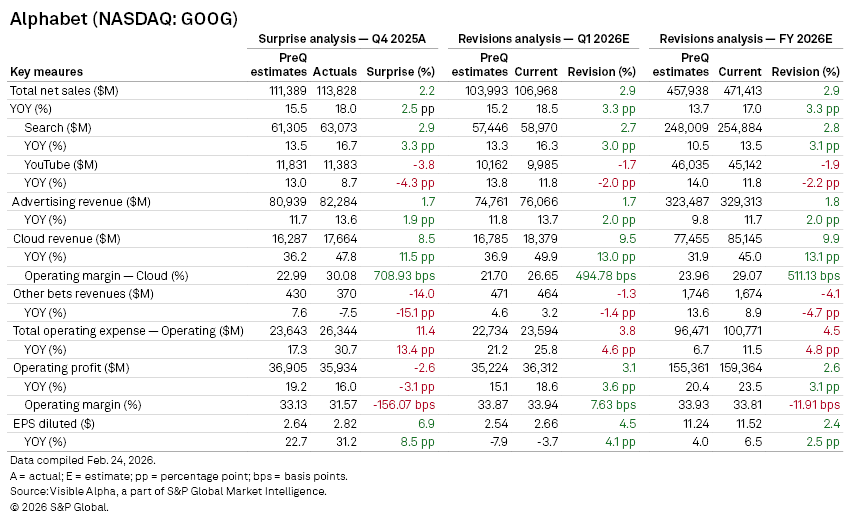

Alphabet Inc. (NASDAQ: GOOG) closed 2025 with a broadly solid fourth quarter, beating Visible Alpha consensus expectations on revenue and earnings as Google Cloud continued to outpace margin expectations. YouTube and the Other Bets segments underwhelmed, and operating expenses rose in Q4 and are expected to continue to move higher in FY 2026.

Big surprise in the Cloud margin

Q4 net sales came in at $113.8 billion, ahead of pre-quarter consensus estimates of $111.4 billion (+2.2% surprise), with year-on-year growth accelerating to 18% vs. an expected 15.5%.

- Search revenue rose 16.7% year-on-year to $63.1 billion, beating consensus estimates by 2.9%.

- Advertising overall grew 13.6%, beating Visible Alpha consensus expectations by 1.7%.

- Google Cloud stood out, surging 47.8% year-on-year to $17.7 billion, an 8.5% revenue beat. In addition, the Cloud margin beat consensus by 708bps in Q4 2025, driven by strong demand for enterprise AI products.

By contrast:

- YouTube revenue missed consensus expectations by 3.8%, with growth slowing to 8.7% year-on-year (vs. 13% expected).

- Other Bets revenue declined 7.5% year-on-year and came in 14% below expectations.

Waymo charge pressures consolidated margins

Total operating expenses rose 30.7% year-on-year in Q4, well above the 17.3% increase that analysts expected. As a result, operating profit of $35.9 billion fell 2.6% short of analyst estimates, and operating margin growth lagged top-line expansion. The company reported a $2.1 billion stock-based compensation charge due to an increase in Waymo's valuation related to its recent investment round. According to Management, most of the charge was reflected in R&D expenses.

Outlook: Higher AI investment, stronger Cloud expectations

Looking forward, Capex guidance came in significantly ahead of expectations and is projected to be $179 billion, up from $120 billion for FY 2026.

Total revenues also are getting revised up, driven by continued solid performance of the Search and Cloud segments.

Cloud expectations have increased materially:

- Q1 2026 Cloud revenue forecasts have been raised by roughly 9.5% and the Cloud margin is now expected to be 26.8%.

- FY 2026 Cloud revenue is now projected to grow 45% year-on-year, well above prior estimates, with margins also revised up more than 500bps to 29.3%, driven by strong demand for Cloud services and products.

More broadly, consensus continued to move higher post-Q4 2025:

- Q1 2026 revenue estimates by 2.9% to $107 billion.

- Q1 2026 EPS estimates by 4.5%.

- FY 2026 revenue forecasts by 2.9% to $471.4 billion.

- FY 2026 EPS estimates by 2.4%.

Amazon Q4 2025 earnings and outlook

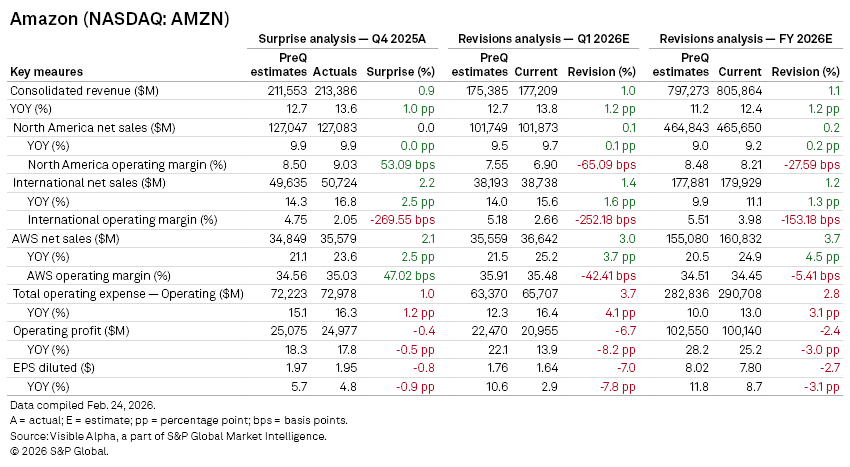

Amazon.com (NASDAQ: AMZN) delivered a modest top-line beat in Q4 2025, driven by continued strength in AWS and international growth.

However, softer profitability trends and downward revisions to 2026 operating income and EPS suggest analysts are recalibrating expectations amid rising costs and margin compression outside of cloud.

Revenue: Slight beat, mixed segment trends

Q4 consolidated revenue rose to $213.4 billion, a 0.9% beat versus Visible Alpha consensus expectations.

Segment performance was mixed:

- North America net sales totaled $127.1 billion in Q4, broadly in line with consensus expectations. Operating margin expanded to 9.03%, 53 basis points above consensus.

- International net sales beat consensus expectations by 2.2%, rising 16.8% year-on-year. However, operating margin missed estimates by nearly 270 basis points.

- AWS revenue reached $35.6 billion, up 23.6% year-on-year, and 2.1% ahead of consensus expectations. AWS operating margin came in at 35.03%, slightly above expectations.

Profitability: Costs outpaced revenue growth

Total operating expenses rose 16.3% year-on-year in Q4, outpacing revenue growth. As a result:

- Operating profit of $25 billion slightly missed consensus expectations (-0.4%).

- Diluted EPS of $1.95 came in 0.8% below pre-quarter estimates.

2026 outlook: Revenue up, earnings down

Looking ahead, analysts have raised revenue forecasts but lowered earnings expectations.

Q1 2026:

- Revenue is projected at $177.2 billion, 1% above prior estimates.

- Operating profit estimates have been cut by 6.7%.

- EPS estimates have been lowered by 7%.

FY 2026:

Revenue is now expected to reach $805.9 billion, 1.1% above prior projections.

- Operating profit forecasts are down 2.4%.

- EPS expectations have been lowered by 2.7%.

Analysts have also trimmed margin forecasts across key segments:

Q1 2026:

- AWS margin is now forecast at 35.48%, slightly below prior estimates.

- North America operating margin is now expected at 6.90%, down from prior expectations of 7.55%.

- International operating margin is currently projected at 2.66%, sharply below the prior 5.18%.

FY 2026:

- AWS margin expectations have edged down to 34.45%, from 34.51%.

- North America operating margin is now estimated at 8.21%, below the previous 8.48%.

- International operating margin is forecast at 3.98%, down from 5.51%.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment