Research — January 28, 2026

AI memory boom squeezes legacy DRAM supply, pushing prices higher

By Akash Jishnu and Ehteesham Ansari

As leading memory semiconductor manufacturers; Samsung Electronics Co. Ltd. (KRX: 005930), SK hynix Inc. (KRX: 000660), and Micron Technology Inc. (NASDAQ: MU), divert production capacity toward high-bandwidth memory, a premium form of DRAM used in AI data centers, supplies of conventional DRAM are tightening, driving prices higher.

High-bandwidth memory, or HBM, has become one of the most lucrative niches in semiconductors, benefiting from explosive demand linked to AI model training and inference. The problem for enterprise IT buyers is that the same production lines also make standard DRAM, which supports servers, PCs, and a wide range of consumer electronics. As capacity tilts toward HBM, traditional DRAM is experiencing a supply shortage, driving up prices.

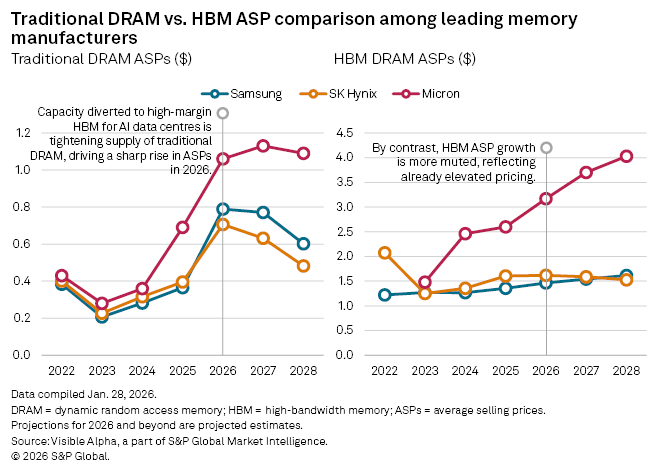

Visible Alpha consensus estimates point to a steep acceleration in average selling prices for conventional DRAM in 2026. Samsung’s revenue per bit from traditional DRAM is forecast to rise 116% year-on-year to $0.79 in 2026, up from $0.36 last year. SK Hynix is expected to see a 78% increase to $0.70 from $0.40, while Micron’s traditional DRAM ASP is projected to climb 54% to $1.06.

By contrast, pricing gains in HBM look far more restrained, reflecting both rapid capacity expansion and the already elevated starting point. Analysts expect HBM ASPs to rise by about 8% at Samsung, 1% at SK Hynix, and 22% at Micron in 2026.

The imbalance reflects clear economic incentives. HBM carries meaningfully higher margins than conventional DRAM, encouraging all manufacturers to prioritize AI-linked products over legacy enterprise and consumer memory. That strategy supports profitability, but risks pushing up costs for corporate IT budgets at a time when data center investment is already under pressure.

Micron has moved to ease near-term constraints. The US chipmaker recently struck a strategic partnership with Taiwan’s Powerchip Semiconductor Manufacturing to access additional DRAM capacity, while also stepping up investment in new fabrication plants in the US. Those facilities, however, will not come on stream for several years. In the meantime, Micron is relying on existing clean-room infrastructure in Taiwan to lift output.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment