22 Dec, 2025

Data center demand, rising investor interest fuel US nuclear growth, restarts

| A mockup of a GE Vernova Hitachi Nuclear Energy BWRX-300 small modular nuclear reactor facility. |

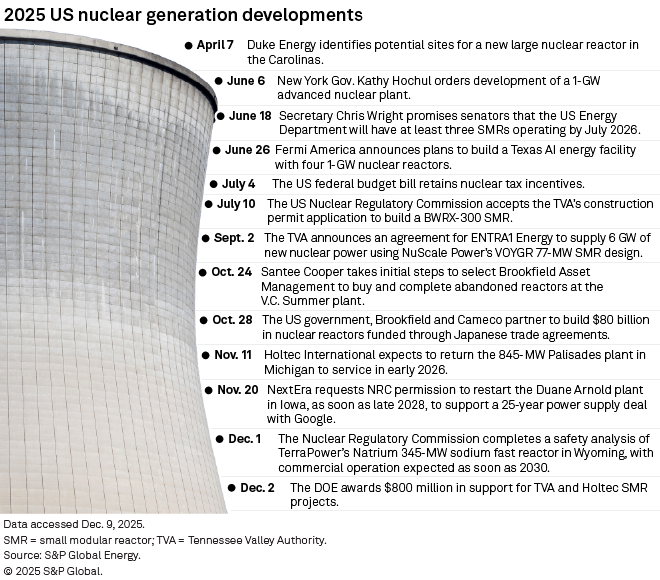

Licensing milestones and construction of advanced reactor projects will be key signs of the nuclear sector's progress in 2026, according to experts, following a year in which plans to restart shuttered plants drove most deal activity.

"That term, 'nuclear renaissance,' has been batted around a few other times before. But this time, I think it's fundamentally different in that it's demand driven," Drew Marsh, CEO and chairman of Entergy Corp., who is also chair of the industry advocacy group the Nuclear Energy Institute, said in an interview with Platts, part of S&P Global Energy.

Demand from large-load customers such as data centers has pushed nuclear into the "energy expansion" narrative, said Marlina Omar, an analyst at S&P Global Energy Horizons. Major tech companies including Microsoft Corp., Amazon.com Inc. and Google LLC announced power purchase agreements with nuclear power providers, the US government signaled clear support of the industry, and advanced technologies are progressing.

"I don't expect that to slow down anytime soon," Marsh said.

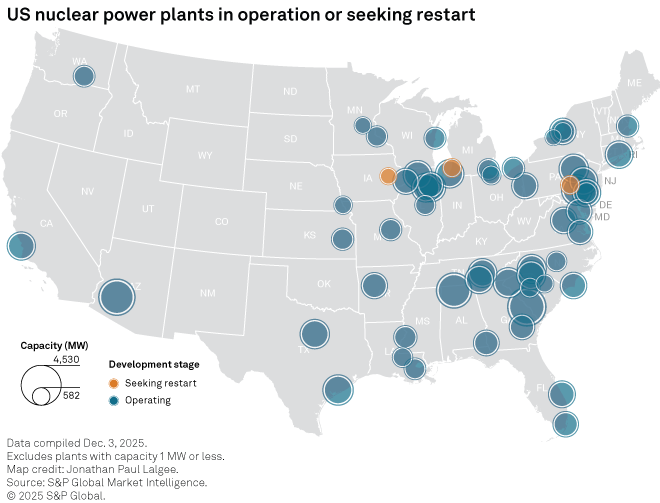

The Trump administration set a goal in 2025 of increasing US nuclear capacity to 400 GW by 2050. Existing US nuclear capacity totals about 97 GW.

A US nuclear resurgence is "not assured," said Adam Stein, director of the Nuclear Energy Innovation program at the Breakthrough Institute. "What we're missing from this equation is firm orders … and buyers cannot all be hyperscalers and tech companies, or even industrial companies. They have to be utilities."

Utilities may need to consider forming consortia to share costs, risks and output in order to build up reactor orders, experts said.

Fleet revival

Increased demand has reversed the fate of shuttered US nuclear plants such as Three Mile Island unit 1, Palisades and the Duane Arnold Energy Center. South Carolina's unfinished V.C. Summer reactors are also back in play after the project was abandoned in 2017.

Additionally, owners are seeking uprates of existing plants that could increase US nuclear capacity by 1 GW to 2 GW by the end of the decade.

This activity follows a decade in which US nuclear generation declined and operators worked to preserve existing capacity.

"Today, there's clearly a 'floor' on US nuclear capacity, with uprates, restarts and revivals," said Alan Ahn, deputy director for nuclear at think tank Third Way. "These near-term activities, combined with growing prospects of new builds … have created a positive longer-term outlook for the US fleet."

Investment

The nuclear power sector recorded its highest annual venture funding to date in 2025, signaling renewed investor confidence.

Nearly 40% of all equity investments in nuclear fission since 2020 took place in 2025 alone, according to Net Zero Insights research. In that time, the US raised more than 50% of global venture funding for nuclear power companies. At the beginning of the third quarter of 2025, nuclear fission companies had raised $1.3 billion in equity funding.

Investors gravitated toward projects and technologies with clearer timelines in 2025, a shift from early-stage ventures toward bankability and more selective, near-term commercial designs.

Rounds of investment grew larger, with more strategic investors and participation from utilities, such as the Tennessee Valley Authority and Duke Energy Corp. exploring advanced reactors and associated funding.

"We may see some more traditional utilities take a step forward," such as by selecting a reactor technology in 2026, Stein said.

The World Bank changed policy on financing nuclear projects, which could open the door for other finance institutions to change their policies, said Matt Bowen, a senior research scholar focused on nuclear at the Center on Global Energy Policy at Columbia University.

Nuclear power is expected to receive the bulk of funding from the US Energy Department's Office of Energy Dominance Financing, formerly the Loan Programs Office, Secretary Chris Wright said at the American Nuclear Society conference on Nov. 10.

"We have significant lending authority," Wright said. "By far the biggest use of those dollars will be for nuclear power plants — to get those first plants built."

New reactors

New nuclear technologies saw commercial momentum, proof-of-concept validation and regulatory acceleration in 2025. The demand forecasts prompting the revival of shuttered reactors also increased interest in advanced technologies.

"For better and for worse, SMR developers have tied their fortunes to the AI growth/energy dominance agenda," said Francesco d'Avack, associate director at S&P Global Energy Horizons.

The US has a handful of new commercial nuclear projects under construction, such as Kairos Power LLC's Hermes 2 project. Construction permit applications are under Nuclear Regulatory Commission review for GE-Hitachi Vernova Nuclear Energy Inc.'s BWRX-300 reactor in Tennessee, TerraPower LLC's Natrium reactor in Wyoming and X-energy LLC's Xe-100 reactor in Texas.

Key designs moved through major licensing steps in 2025, showing that advanced reactors are shifting from research and development toward market readiness, according to analysts.

Progress on construction and licensing milestones for those projects will be among the "most significant developments over the next year," Ahn said.

Looking forward

Capital continues to flow for advanced nuclear, d'Avack said, but the "real signpost is going to be when one of the hyperscalers actually puts down the money and cost-overrun guarantee to back a [first-of-its-kind technology]. We have seen money for tech and project development, but nothing on the scale needed to build an actual power plant."

Investment will likely continue in 2026, contingent on visible project delivery. "Investors will demand demonstrated schedule and cost discipline," Omar said.

Gen III+ reactors could see final investment decisions and early construction starts in 2026. Early European contenders also may hit major licensing or financial milestones that could shape investor confidence, Omar said, adding that US repowerings and site reuse are also likely to gain momentum in 2026, with efforts to convert sites of retiring coal plants and aging nuclear facilities into small modular reactor locations.

"I expect some very large deals in 2026," Stein said.

New large-scale nuclear, such as AP1000s, also remain an option for utilities. Duke is exploring the potential to add a large-scale reactor, and others have not ruled it out.

"Some of these utilities … made climate commitments," Bowen said. "In the back of their minds, that's still something that, long term, they're aiming for."

Uneven regulatory pathways

The federal commitment to nuclear in 2025 included maintaining tax credits in federal budget legislation and executive orders to boost the industry. But that may not be enough.

More government intervention to de-risk new nuclear projects could also be on the table in 2026, analysts said, including further DOE support and US-UK regulatory cooperation to help developers reduce uncertainty and streamline the regulatory process.

But the Nuclear Regulatory Commission's reduced capacity may affect application reviews, especially for reactor projects seeking decisions in 2026 and 2027.

"The administration and the Republican-led Congress has … significantly reduced funding for financing tools and tax incentives that would have helped accelerate new nuclear … at a critical inflection point for the sector," Ahn said. "The Trump administration's actions — in the name of regulatory reform and efficiency — threaten to undermine progress for the US nuclear sector."

'If things go south'

A history of cost and schedule overruns still haunts the industry.

"No service commission has stepped forward … to say, 'Well, we are going to put our ratepayers at risk,' because it's still a question for any of these AP1000 builds in the United States, who's going to be holding the bag if things go south. I don't think it's going to be Westinghouse," Bowen said, referring to the AP1000 reactor designer.

Those risks remain one of the industry's primary hurdles.

"If we could figure out a way to really narrow down the uncertainty associated with construction, then … utilities would significantly invest in nuclear reactors versus other potential technologies," Marsh said.

If the industry can deliver a nuclear project using first-of-a-kind technology at cost and on schedule, Bowen said that "could pave the way for a bunch more orders in the 2030s and 2040s."

"We're still years away from knowing whether or not any of these first-of-a-kind projects were landed reasonably close to on time and on budget," Bowen said. "Who is willing to accept the risk … and how does its cost compare to alternatives?"