13 Aug, 2021

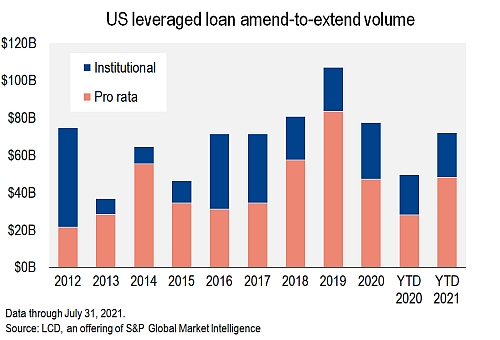

Leveraged loan extension activity remains hot, with YTD volume topping $72B

Amend-and-extend activity in the U.S. leveraged loan market rolled on in July, with the volume of loan extensions coming in at $11.2 billion during the month, just $300 million shy of the $11.5 billion in June, according to LCD.

Amend-and-extend activity reached $72.06 billion in 2021 through July 31, topping the volume recorded during the first seven months of 2020 by $22.55 billion, and already closing in on the $77.34 billion during all of last year.

Amend-and-extend activity last month was courtesy of 13 borrowers, including three borrowers with institutional debt — an extension and repricing of Alterra Mountain Co.'s $1.388 billion term loan B and $643 million TLB-2 that was extended out by seven years, Curia Inc.'s $1.19 billion first-lien term loan that was extended to August 2026, and Switch Inc.'s $400 million TLB that was extended to 2028.

Some of the larger pro rata extensions, meanwhile, included Alliance Data Systems Corp.'s extension of most of its term loan A and revolver to July 2024, SBA Communications Corp.'s extension of its $1.5 billion revolver to July 2026, Avis Budget Car Rental LLC's extension of its $1.95 billion revolver to 2026, EnerSys's extension of its pro rata facility to 2026 and Netflix Inc.'s extension of its $1 billion revolver to June 2026. Overall, pro rata deals continue to represent the lion's share of extension activity, accounting for about $48 billion of the $72 billion of extension volume year-to-date. Pro rata debt typically entails amortizing term loans or revolving credit facilities.

Stepping back and looking at extensions overall, borrowers this year with pro rata loans have been looking mostly down the road, focusing on maturities coming due in 2023 and 2024, extending $21.3 billion and $12.8 billion of debt, respectively. In 2020, borrowers with pro rata loans focused more on upcoming maturities, extending $14.2 billion due in 2021, $15.8 billion due in 2022 and $9.4 billion due in 2023. On the institutional side, borrowers have been focusing on loans coming due in 2024 or later, extending $19.2 billion of that debt. Last year, borrowers with institutional debt also primarily focused on 2024 and beyond, extending $16.8 billion of debt.

Turning to upcoming maturities, the volume of loans coming due in 2021-2023 fell by about $7 billion between June and July, to about $59 billion, against the backdrop of about $1.26 trillion in outstanding loan paper. The volume of loans coming due in 2021-2023 was about $216.2 billion less at the end of July than it was at the end of 2019. Meanwhile, the volume of loans coming due in 2024 and 2025 shrank by about $176.2 billion between the end of 2019 and July 2021, while the par amount outstanding due 2026 or later grew by about $453 billion.

Covenant-relief activity, meanwhile, remains dormant, with just a pair of these transactions being recorded in the month. Sabre GLBL Inc. amended a financial performance covenant to remove the minimum liquidity requirement and the total net leverage ratio maintenance requirement, while VSE Corp. modified the maximum total funded leverage covenant alongside an extension of its pro rata facility.

Overall, year-to-date covenant-relief activity has been down significantly compared to last year. In the first seven months of 2021, there were 21 covenant-relief transactions, versus 149 during the same period in 2020, as companies scrambled for flexibility at the onset of the coronavirus pandemic. In terms of volume, covenant-relief activity through July is the lowest it has been in more than a decade.

Looking at specific sectors, borrowers in Services & Leasing were the most active, with four covenant-relief transactions, while Real Estate, Computers & Electronics, and Manufacturing & Machinery have each seen three transactions so far this year.

Of course, one of the fundamental differences in the covenant-relief landscape today is that most current deals are pro rata, comprising revolving credits and amortizing term debt taken on by banks and financial institutions. A decade ago, covenant-relief activity tilted toward institutional issuers, whose debt is primarily bought by CLOs and retail/mutual funds and exchange-traded funds.

In 2009, the volume of institutional and pro rata covenant-relief activity was about $140 billion and $97 billion, respectively. Fast forward to 2020, and institutional deals accounted for just $20 billion of the $161 billion in covenant-relief volume, according to LCD.

As usual, we will note that because more than three-quarters of the approximately $1.26 trillion in outstanding U.S. leveraged loans are covenant-lite (and pro rata deals are required to have covenants), it stands to reason that most of today's covenant-relief activity is for pro rata deals. For the record, in July, the covenant-lite share of the S&P/LSTA Leveraged Loan Index was at 86%, up from 83% in July 2020. For reference, at the end of 2008, before the peak of covenant amendment activity during the last financial crisis, the covenant-lite share was just 15%.