BLOG — Jun 28, 2023

Right place, right time: Supply chain outlook for third quarter 2023

By Chris Rogers

Supply chains are almost back to normal in terms of activity, inventories and seasonality. Yet, there are plenty of uncertainties in both the government policy and physical risk heading into the second half of 2023 as firms start to implement long-term supply chain restructuring plans.

Time for a break: Supply chains continue to settle

Evidence of a return to normal supply chain activity is now well established, and largely due to a decline in activity. The S&P Global manufacturing PMI shows supplier delivery times have reached their fastest since April 2009 as of May.

From an inventory perspective, manufacturers' stocks of purchases in May were a touch above the first-quarter 2023 average, while stocks of finished goods are close to balance.

Retailers' inventories are more of a mixed bag based on corporate financial data, with fast-fashion firms' inventory-to-sales ratios in line with pre-pandemic levels. Inventories remain elevated for home appliances, building suppliers and electronics, though that reflects depressed demand rather than a new "just in case" management model.

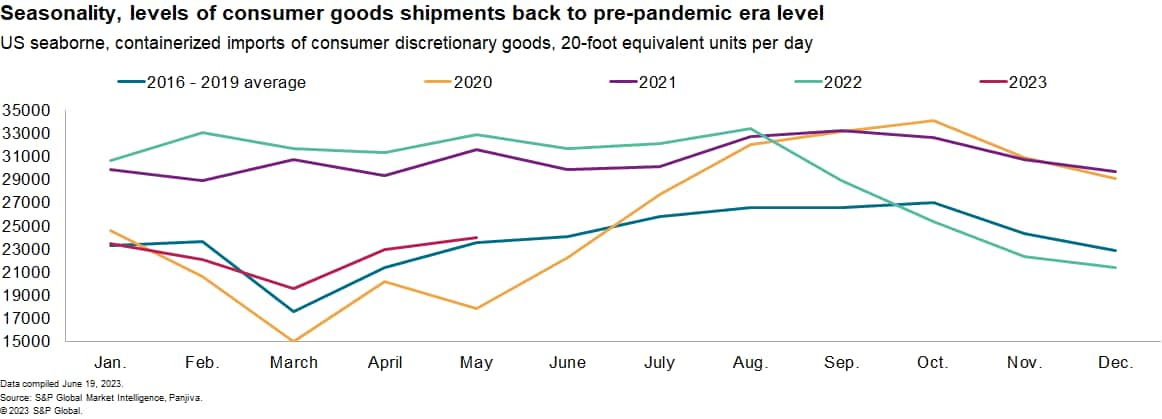

One of the most visible signs of disruptions during the pandemic were shortages and delayed deliveries of consumer discretionary goods, ranging from home appliances and televisions to furniture and apparel. That led to disrupted shipping patterns, which now appear well on the way to being corrected.

In 2023, there appears to have been a return to historic levels in both the level and pattern of shipments during in the first part of the year. In May 2023, US seaborne imports of containerized freight fell by 27% year over year and were 2% above the 2016 to 2019 average for the month.

Places matter: Policy and physical risks to watch

The ongoing conflict in Ukraine is expected to continue through at least the end of 2023. Market Intelligence's Country Risk team expects that the conflict will likely continue for the foreseeable future under the current Russian administration.

Food supply chains are particularly exposed to the "Black Sea grain initiative," which may only continue from the latter half of July 2023 without Russian participation.

Continued conflict will likely mean that supply chains will have little respite from the additional complications brought by sanctions, with new EU regulations covering exports of goods from third-party countries now in-force.

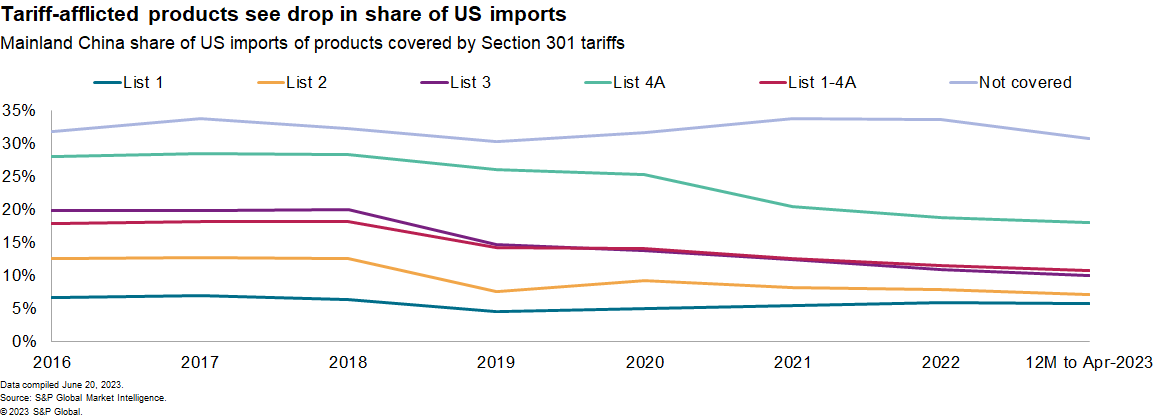

A review of US Section 301 duties on imports from mainland China, imposed initially by the Trump administration, could be completed by the end of 2023. That introduces uncertainty — both positive and negative — for supply chains utilizing the afflicted products. Reshoring decisions may be slowed until the uncertainty is resolved.

The Section 301 tariffs were instituted in four phases from July 2018 to September 2019 at rates of 25% (Lists 1, 2 and 3) and 7.5% (List 4A, down from 15% initially). A wave of COVID-19 and other exclusions have also been applied.

Market Intelligence analysis shows mainland China's share of US imports of products covered by Section 301 duties fell to 11% in the 12 months to April 30, 2023, from 18% in 2016. The share of imports of products not covered by tariffs only fell to 31% from 32% over the same period.

It's unlikely that the Section 301 tariffs will be reviewed or updated in isolation from wider US-China geopolitical tensions. Those are likely to remain focused on the technology sector.

There have already been signs of bifurcation in technology supply chains, particularly in the supply of semiconductor manufacturing equipment in early 2023. Confirmation of the rules for exports from the Netherlands to mainland China should become clearer.

A series of EU-focused environment-linked regulations are being negotiated or come into force during the second half of 2023. These could prove particularly consequential for the steel and aluminum sectors and their downstream supply chains.

- The EU and US are in the process of negotiating an agreement on tariffs to be applied on steel and aluminum based on the greenhouse gas emissions of production. The European Commission has indicated a deal could be completed by October.

- The implementation of the EU's Carbon Border Adjustment Mechanism (CBAM) also takes effect in October with a requirement to report imports under the scheme.

While international trade activity patterns appear to have returned to normal, physical logistics network disruptions from a variety of natural disaster and staff-related factors remain possible, particularly during the peak shipping season.

- The risk of a West Coast port strike has diminished with a new — but as yet unratified — deal, but inland labor disruptions cannot be ruled out.

- Low water levels in the Panama Canal are already restricting ship movements from Asia to the Atlantic basin.

- The logistics sector has endured several cyber attacks over the past five years, the impact of which can be elevated during peak shipping season.

Right place, right time: Delivering supply chain change

As supply chain activities have normalized, corporations are reviewing and implementing supply chain changes in the light of the past three years. The second half of 2023 should bring more announcements of long-term supply chain strategy choices.

A central issue is that the main routes to change are all long-term in nature and expensive to implement in a lower cash-flow / higher interest rate environment. That's particularly the case for inventory management and multi-sourcing, which both add cost.

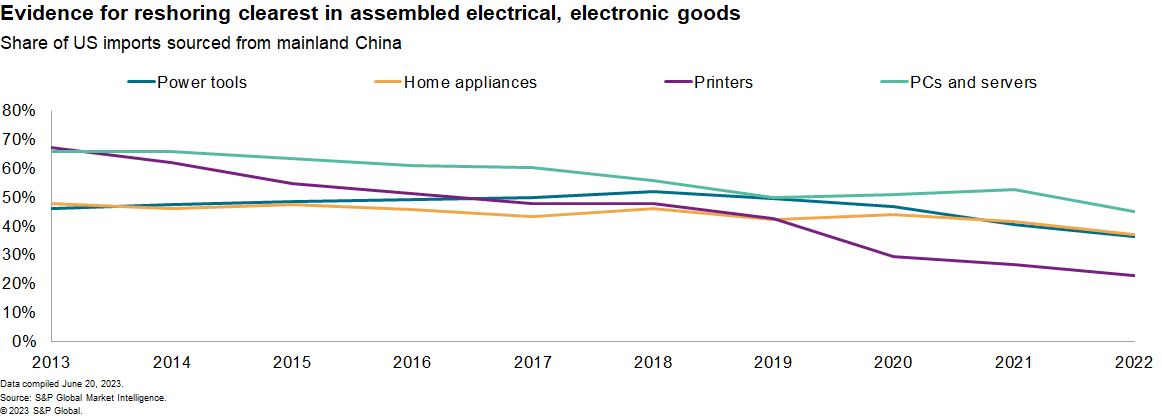

There is plenty of evidence that reshoring is already taking place. Mainland China's suppliers' share of US imports printers was 23% in 2022 down steadily from 67% in 2013. There's been similar patterns for power tools, home appliances and personal computers.

Reshoring can take years to implement. A key part of that process, alongside other resilience strategies, such as inventory management and multi-sourcing, is investment to digitize supply chain operations. There's evidence of that taking place. A recent survey by S&P Global's 451 Research showed that 42% of firms already have comprehensive supply chain visibility systems in place, while another 33% are in the discovery, or proof-of-concept stage.

Sign up for our Supply Chain Essentials newsletter

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.