BLOG — Nov 02, 2022

US Monthly GDP Index for September 2022

By Ben Herzon and Kathleen Navin

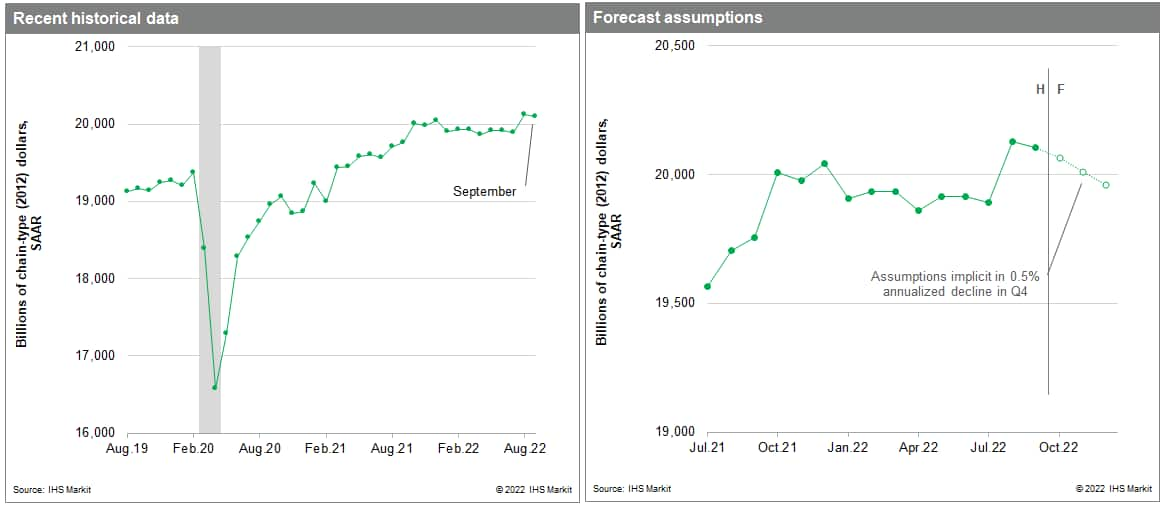

Monthly US GDP declined 0.1% in September following a 1.2% increase in August that was revised higher from 0.8%. The slight decline in September mainly reflected declines in net exports and residential investment that were nearly offset by gains in personal consumption expenditures and nonresidential fixed investment. The level of GDP in September was 1.2% above the third-quarter average at an annual rate. Implicit in our forecast of a 0.5% annualized decline in GDP in the fourth quarter are declines in monthly GDP in October, November, and December that average 0.2% per month (not annualized).

Our Monthly US GDP Index (MGDP) is a monthly indicator of real aggregate output that is conceptually consistent with real Gross Domestic Product (GDP) in the National Income and Product Accounts. The Monthly GDP Index is consistent with the NIPAs for two reasons: first, MGDP is calculated using much of the same underlying monthly source data that is used in the calculation of GDP. Second, the method of aggregation to arrive at MGDP is similar to that for official GDP. Growth of MGDP at the monthly frequency is determined primarily by movements in the underlying monthly source data, and growth of MGDP at the quarterly frequency is nearly identical to growth of real GDP.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.