BLOG — Dec 07, 2020

US GDP outlook on the rise for 2021 on promising stimulus negotiations and vaccine progress

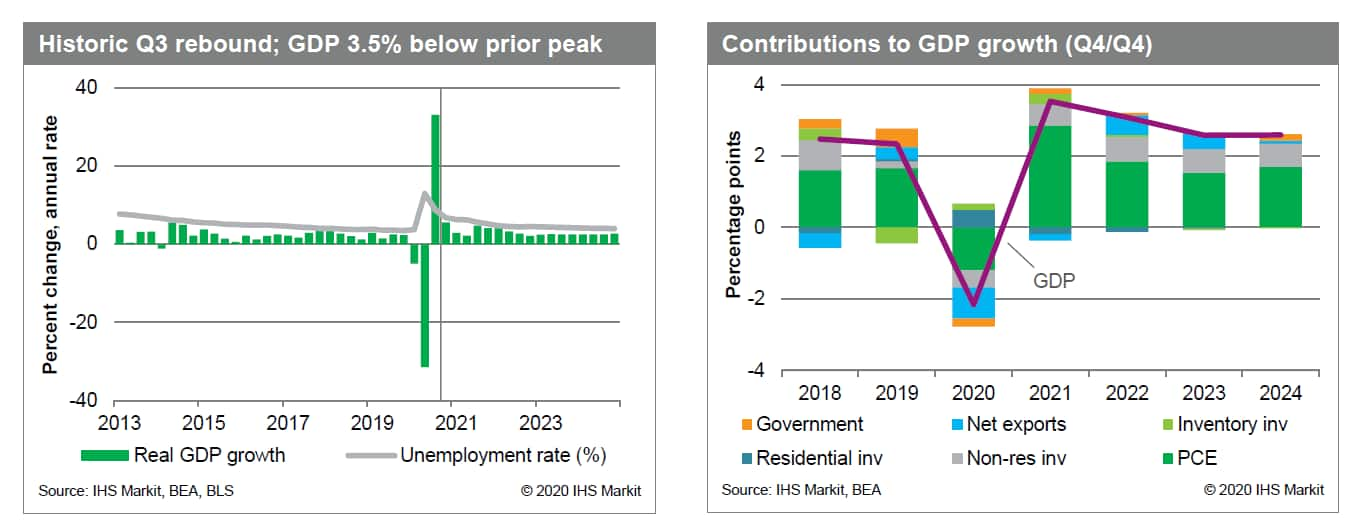

Without additional fiscal stimulus, the recent surge in COVID-19 infections and the re-imposition of measures to contain the virus by some states and localities would undermine the economic recovery early next year. However, the prospective inoculation by midyear of much of the population with unexpectedly effective vaccines will unleash consumer spending in late 2021 and early 2022.

With negotiations on fiscal stimulus now gaining bipartisan support, we now expect agreement on a 3-month extension of emergency unemployment programs, and an enhanced unemployment benefit of $300/week, to be reached before Christmas. This stimulus will more than offset the negative impact on spending of the recent surge in infections and, alongside the promising news on vaccines, led us to revise up our forecast for GDP growth in 2021 from 3.1% to 4.3%.