ECONOMICS COMMENTARY — Feb 08, 2024

Monthly PMI Bulletin: February 2024

By Jingyi Pan

The following is an extract from S&P Global Market Intelligence's latest Monthly PMI Bulletin. For the full report, please click on the 'Download Full Report' link.

Global growth accelerates while output price inflation ease

The global economic expansion accelerated for a third straight month in January amidst renewed manufacturing output growth and faster services activity expansion. Additionally, an easing of selling price inflation was a welcome sign. Though risks of prices rising amid higher shipping costs will be worth monitoring in the months ahead.

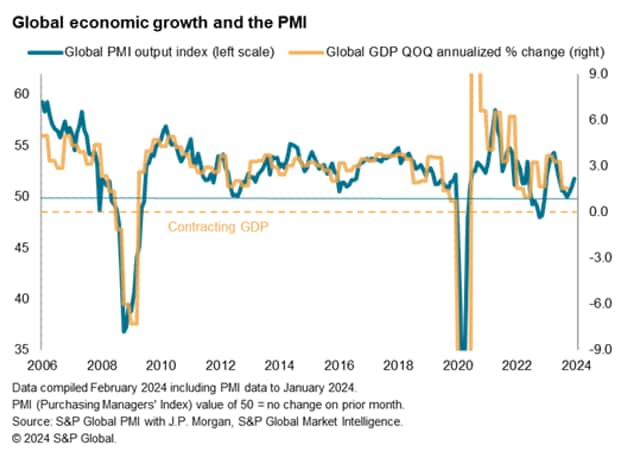

The J.P.Morgan Global PMI Composite Output Index - produced by S&P Global - rose to 51.8 in January, up from 51.0 in December. The headline PMI continued to rest below the survey's long-run average of 53.2 and is consistent with an annualized quarterly global GDP growth of approximately 1.8%, well below the pre-pandemic ten-year average of 3.0%. That said, the latest upturn helps to allay concerns of a global recession and further point to the worst impact of prior rate hikes having now passed as manufacturing demand near-stabilised while services new orders growth accelerated.

Global manufacturing output notably expanded for the first time in eight months despite ongoing disruptions in the Red Sea. While supply delays heightened visibly at the start of the year and shipping costs rose in tandem with the breakout of the Red Sea conflicts, confidence improved among global manufacturers with better growth prospects of looser financial conditions and with global destocking, a key dampening factor on demand thus far, further easing.

Service sector growth also accelerated at the start of the year. This was most importantly accompanied by falling price pressure, leading to overall selling price inflation falling to the lowest since October 2020 and boding well for the prospects of lowering interest rates. That said, a stronger rise in manufacturing cost inflation will be worth monitoring particularly surrounding supply delays as we await the next release of flash PMI data on February 22.

© 2024, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Location