Blog — 24 Jan, 2023

Insight Weekly: Inflation eases; bank M&A slows; top companies boost market share

By Sarah Cottle

Today is Tuesday, January 24, 2023, and here’s your weekly selection of essential intelligence on financial markets and the global economy from S&P Global Market Intelligence. Subscribe to be notified of each new Insight Weekly.

In this edition of Insight Weekly, we put a spotlight on the continued slowdown in U.S. inflation, an indication that the Federal Reserve's aggressive interest rate hike push is working as intended. The consumer price index rose 6.5% year over year on a non-seasonally adjusted basis in December 2022, marking the sixth consecutive month of lower annual growth since inflation peaked at 9.1% in June. Economists at S&P Global Market Intelligence expect inflation to ease further, consistent with their forecast for a mild recession this year and softening demand in product and labor markets. Stocks and government bonds have rallied from recent lows, reflecting investors' optimism that cooling inflation will pave the way for a more dovish Fed.

The combination of economic uncertainty, rapidly rising interest rates and heightened scrutiny weakened U.S. bank deal activity in 2022. Banks announced 167 deals last year for a total deal value of $22.62 billion, the lowest deal value since 2014. The impact of interest rate hikes on merger math impeded dealmaking, and deal advisers expect that dynamic to continue in 2023.

The largest U.S. companies have increased their dominance of industry market share as the economy becomes more consolidated. In 91 of the 157 primary industries tracked by Market Intelligence, the top five companies by revenue combine for at least 80% of total revenue among publicly traded companies in their respective industries, up from 71 industries in 2000. The publishing industry has seen the biggest growth in market concentration. Some industries have become less consolidated, notably specialized real estate investment trusts.

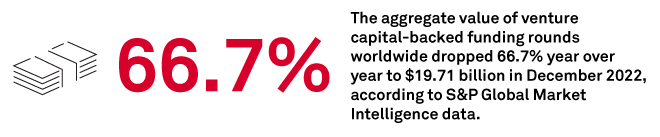

The Big Number

Trending

—Read more on S&P Global Market Intelligence and follow @SPGlobal on Twitter

The Big Picture

What will shape your big picture in 2023? How will disrupted supply chains, inflation, and new sustainability and M&A trends impact your sector? Our 2023 Big Picture Outlook reports can expand your perspective and enable decisions with conviction.

Additional Insights from S&P Global Market Intelligence

Increase your competitive edge with essential insights delivered straight to your inbox. We offer complimentary newsletters on a wide variety of topics to help you stay on top of what’s moving the markets, separating the immaterial from the invaluable. Review our newsletters and sign up here.

IHS Markit is now part of S&P Global.

Written and compiled by Roma Arora

Theme