BLOG — Feb 10, 2021

Daily Global Market Summary - 10 February 2021

By Chris Fenske

Most APAC equity markets closed higher, US was mixed, and all major European indices closed lower. US government bonds closed higher, while most benchmark European bonds closed lower. European iTraxx and CDX-NA were slightly tighter on the day. For the second consecutive day, the US dollar and silver were lower and oil, gold, and copper were higher on the day.

Americas

- US equity indices closed mixed; DJIA +0.2%, S&P 500 flat, Nasdaq -0.3%, and Russell 2000 -0.7%.

- 10yr US govt bonds closed -3bps/1.13% yield and 30yr bonds -4bps/1.91% yield.

- CDX-NAIG closed -1bp/50bps and CDX-NAHY -2bps/285bps.

- DXY US dollar index closed -0.1%/90.37.

- Gold closed +0.3%/$1,843 per ounce, silver -1.2%/$27.08 per ounce, and copper +1.3%/$3.77 per pound.

- Crude oil closed +0.5%/$58.58 per barrel. It is worth noting that Crude oil has closed higher every trading day in February and is +12.4% MTD.

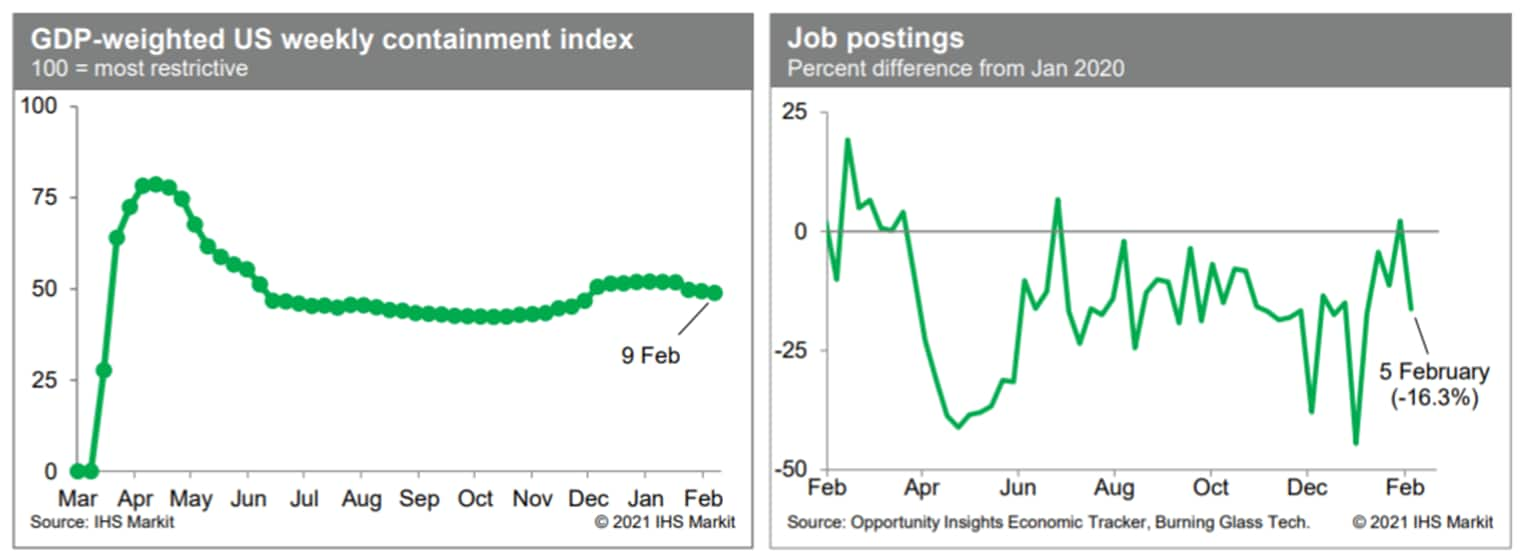

- The IHS Markit GDP-weighted US weekly containment index declined 0.4 index point this week to 49.0, reflecting easing restrictions on social and economic activity in five states: Illinois, New Jersey, Oregon, New Mexico, and Rhode Island. Meanwhile, job postings slowed to 16.3% below the January 2020 level the week ending 5 February and were revised materially lower for prior weeks, according to the Opportunity Insights Economic Tracker. Averaged from mid-January through early February, job postings have improved relative to the prior trend, but the recent data (including revisions) indicate less verve in labor demand than previously thought. (IHS Markit Economists Ben Herzon and Joel Prakken)

- The US Consumer Price Index (CPI) rose 0.3% in January following a 0.2% increase in December. The price index for gasoline rose 7.4%, contributing to a 3.5% increase in the CPI for energy and accounting for most of the rise in the overall CPI. The food index rose 0.1% while the core CPI, which excludes the direct effects of movements in food and energy prices, was unchanged (0.0%). (IHS Markit Economists Ken Matheny and Juan Turcios)

-

- Inflation remained subdued through January. The CPI rose 1.4% over the 12 months through January, unchanged from December. The core CPI also rose 1.4% over the same period, declining 0.2 percentage point from December. The 12-month change in the core CPI has rebounded relatively little after declining sharply from 2.4% in February 2020 to 1.2% in May and June.

- Rent inflation remained low after subsiding since last winter. Both rent of primary residence and owner-equivalent rent of residences rose just 0.1% in January and for the third consecutive month. Their 12-month changes were 2.1% and 2.0%, respectively, down 1.7 percentage points and 1.3 percentage points from 12-month readings as of February 2020. The CPIs for rent represent about 32% of the overall CPI and 40% of the core CPI.

- The price index for used cars and trucks fell 0.9% in January and declined 3.1% over the last three months, partially reversing a 15.4% increase from July to October. Also declining in January were indices for airlines fares (3.2%), new vehicles (0.5%), and lodging away from home (1.9%). Rising in January were indices for apparel (2.2%) and medical care services (0.5%).

- The price index for gasoline jumped 7.4% in January. Since May, the price of gasoline has risen 37.4%, reversing about three-quarters of the sharp decline that occurred over the first five months of 2020.

- California's Department of Motor Vehicles (DMV), which administers the US state's program on autonomous vehicle (AV) testing, has released the latest annual company reports on testing results. The DMV requires automakers and others testing AVs in the state to report annually the number of disengagements (when the car required a human to take over) and miles driven, although only those with licenses to operate for the full year are required to file a report. Most reports are broken down by month and contain some explanation of why disengagements happened, although there is no prescribed format for these reports. These companies' AV fleets drove a total of nearly 2 million miles, a decrease of 800,000 from 2019, likely due to COVID-19 virus-related shelter-in-place orders and other pandemic-induced restrictions. (IHS Markit Automotive Mobility's Surabhi Rajpal)

-

- General Motors (GM) Cruise's AVs recorded the most miles, at 770,049, and its disengagement rate dropped to 0.035 per 1,000 autonomous driven miles, or one per 28,520 miles, in 2020.

- Waymo's AVs recorded the lowest disengagement rate of 0.033 per 1,000 autonomous driven miles in 2020, compared with 0.076 in 2019. Waymo's AV fleet drove 628,839 miles during 2020, less than half of what it reported for 2019.

- Apple's AVs drove 18,805 miles last year, up from 7,544 miles in 2019.

- Aurora Technologies has announced a collaboration with Toyota and Denso aimed at creating self-driving vehicles intended to be deployed in a ride-hailing fleets, including Uber's fleet. The collaboration appears to build on Toyota and Denso's prior investment in and relationship with Uber related to its self-driving technology. While the announcement suggests confidence in Aurora's progress on the technology, the collaboration does not appear to be particularly high risk for Toyota or Denso relative to investment in dedicated manufacturing or businesses, and it aligns with Toyota's stated intention to work with partners to deploy advanced technology in the mobility space. (IHS Markit AutoIntelligence's Stephanie Brinley)

- GM is extending the downtime at three North American plants as it manages the impact of the semiconductor shortage affecting the auto industry globally and plans to reassess the situation in mid-March, according to a company statement released on 9 February. The three plants affected by the microchip shortage are Fairfax (United States), CAMI (Canada), and San Luis Potosi (Mexico). GM said, "Our intent is to make up as much production lost at these plants as possible. In addition, when there is a shortage of semiconductors that impacts production, in some cases we intend to build vehicles without certain modules and will complete them as soon as possible. (IHS Markit AutoIntelligence's Stephanie Brinley)

- Chart Industries along with 10 other like minded companies has launched Hydrogen Forward coalition. The coalition is focused on advancing hydrogen development in the United States by supporting policies that accelerate hydrogen adoption and build related infrastructure. The founding members of the coalition are Air Liquide, Anglo American, Bloom Energy, CF Industries, Chart Industries, Cummins Inc., Hyundai, Linde, McDermott, Shell, and Toyota. The coalition members are linked through complete hydrogen value chain from source to service with a common goal of realizing hydrogen's potential to power its application in daily lives such as delivery trucks, forklifts, cars, power generation, and even aerospace, and decarbonize energy intensive industries, such as transportation and mining. (IHS Markit Upstream Costs and Technology's Neeraj Kumar Tiwari)

- The Center for Science in the Public Interest (CSPI) has petitioned FDA to establish controls for opioids in poppy seeds, ensuring that US consumers are protected from seeds that may contain dangerous levels of naturally occurring opiates, such as morphine and codeine. In a petition submitted on behalf of six families that suffered death and other losses related to consumption of poppy seeds that were contaminated with opiates, the consumer group is urging FDA to establish a cap for the level of opiates that can be found in poppy seeds sold in the US. (IHS Markit Food and Agricultural Policy's Margarita Raycheva)

- Argentina is the world's top producer of soymeal and no.3 exporter of corn had suffered from high domestic food inflation. The country agriculture ministry announced on 30 December 2020 its plans to impose a complete ban on corn exports for two months. However, on 11 January 2021 lifted the complete ban and was replaced by a temporary daily limit on export sales of 30kt. As per IHS Markit's Commodities at Sea, as per provisional calculations, total agribulk shipments from Argentina during January 2021 stood at 5.4mt (versus 6.8mt during January 2020). For the said period, shipments of corn, soybean meal, and wheat stood at 1.4mt (down 29% y/y), 1.7mt (up 15%), and 1.7mt (down 38%), respectively. (IHS Markit Maritime and Trade's Pranay Shukla)

Europe/Middle East/Africa

- European equity markets closed lower; Germany -0.6%, France/Spain -0.4%, Italy -0.2%, and UK -0.1%.

- Most 10yr European govt bonds closed except for Italy closing -1bp and also reaching a new all-time low yield of 0.50%; France/Spain/Germany +1bp and UK +3bps.

- iTraxx-Europe closed flat/48bps and iTraxx-Xover -3bps/244bps.

- Brent crude +0.6%/$61.47 per barrel. Similar to Crude oil mentioned earlier, Brent has closed higher every day this month and is +11.7% MTD.

- UK trading company Chelmer Foods has identified a number of key logistical issues arising from the COVID-19 pandemic. The firm's national accounts manager Paul Turone last week spoke to IHS Markit on many of these. Chelmer Foods trades nuts, dried fruits and seeds. Turone commented: "We find ourselves in unprecedented times where the entire logistics world is in somewhat of a meltdown through a combination of Brexit, COVID and seasonal issues that is going to impact the supply chain massively over the next few months." Chelmer Foods says the entire industry is currently facing the following issues (IHS Markit Food and Agricultural Commodities' Julian Gale):

-

- Shipping - worldwide misalignment of empty shipping containers, over-booked vessels when availability can be found and monumental increases in charges from shipping lines.

- Ports - huge port congestion across the UK as a direct consequence of reduced productivity at all UK ports, increased volumes due to seasonal uplift, Brexit stock building, under investment/preparedness of UK port health/customs and a severe lack of infrastructure on haulage to support these increases.

- Warehousing and delivery transport - lack of empty warehousing due to seasonality and Brexit stock building and an increase in traditional haulers working on internet orders.

- Final January data based on national methodology from Germany's Federal Statistical Office (FSO) have confirmed the end-January 'flash' data release, posting 0.8% month on month (m/m) and 1.0% year on year, the latter leaping from -0.3% in December 2020. This compares with average inflation of 1.4% in 2019 and 0.5% in 2020. (IHS Markit Economist Timo Klein)

-

- Both national and harmonized inflation numbers were boosted by the return of VAT to the rates prevailing until June 2020 (an impact of around 0.9%), the introduction of carbon taxes on energy components (impact around 0.3%), and to a small degree by an increase in the minimum wage rate.

- The y/y rate for clothing/shoes jumped from -5.4% in December to 1.1% in January as seasonal patterns were distorted by the closure of the retail sector for non-essential goods. This boosted inflation by about 0.3% and should unwind again in February-March.

- January's component breakdown for national data reveals that an energy price increase of 5.4% m/m boosted headline inflation by about 0.5 percentage point - a mixture of higher oil prices and the new carbon tax.

- Apart from energy, all major categories equally posted significant price increases due to the VAT effect. Goods were affected much more strongly (2.5% m/m, with the y/y rate jumping from December's -1.8% to 0.6%) than services (-0.8% m/m - negative for seasonal reasons - with the y/y rate up from 1.1% to 1.4%), which essentially reflects the influence of higher energy prices.

- The Volkswagen (VW) Group is expecting the supply of semiconductors for automotive use to remain constrained during the first half of 2021, according to a Reuters report. The company says that it is doing everything in its power to mitigate the effects of the shortage and that it is working to ensure a return to a level of supply that maintains production demand in the second half of 2021. In a statement to Reuters, the company said, "Volkswagen is continuously working on minimizing the effects of the global semiconductor bottleneck on production." (IHS Markit AutoIntelligence Tim Urquhart)

- The French government is set to hold a meeting with the automotive and electronics industries over the semiconductor shortage that has hit production at some automakers. A spokesperson for French automotive industry lobby group La Plateforme Automobile (PFA) said that discussions would cover the fallout of this situation. (IHS Markit AutoIntelligence's Ian Fletcher)

- French industrial production declined by 0.8% month on month (m/m) in December 2020, according to seasonally adjusted figures released by the National Institute of Statistics and Economic Studies (Institut national de la statistique et des études économiques: INSEE). Production had fallen by 0.7% m/m in November. (IHS Markit Economist Diego Iscaro)

-

- Prior to November, industrial production had grown for six successive months. On a year-on-year (y/y) basis, industrial production waned by 3.0% in December and 10.3% in 2020 as a whole.

- Manufacturing output fell by 1.7% m/m in December, following a rise of 0.7% m/m in November. Manufacturing production in December was still 5.7% below its pre-coronavirus disease 2019 (COVID-19) virus pandemic level in February 2020.

- A 3.0% m/m increase in production of transport equipment was more than offset by declines in production of machinery and equipment goods (-3.5% m/m) and food products and beverages (-1.8% m/m).

- On the other hand, energy production, which had fallen by 8.5% m/m in November, rebounded by 4.3% m/m in December thanks to higher electricity production. Energy output was 0.3% above its February 2020 level.

- According to a flash estimate from the Saudi Arabian General Authority for Statistics (GASTAT), real GDP grew by 2.8% on the quarter, seasonally-adjusted, in the final quarter of 2020. The rebound that was apparent in the third quarter was thus maintained. (IHS Markit Economist Ralf Wiegert)

-

- Growth was still negative in year-on-year terms, with GDP falling by 3.8% following 4.6% in the third quarter. The Saudi economy had suffered a steep decline in the second quarter as the lockdown measures against the global pandemic and the cuts to oil production hit the largest economy of the Gulf Cooperation Council (GCC) member states.

- For the year 2020 as a whole, the new data also revealed that the Saudi economy declined 4.1% following 0.3% in 2019. More details, including a full breakdown of GDP for the fourth quarter, will be published by GASTAT on 16 March.

- Recent monthly results for IHS Markit's Purchasing Manager Index (PMI) for the Saudi non-oil economy delivered an upbeat outlook for the first quarter. The PMI reached a new post-pandemic high, capping January at 57.1 points, remaining above the 50-point threshold that separates expansion from decline for the fifth consecutive month.

- Botswana's fiscal account has been under severe stress in FY 2020/21, with revenues plummeting 11% below the revised target of BWP60.71 billion (about USD5.58 billion), due to sluggish economic activity on one hand and total expenditure ramped up to meet health needs induced by the COVID-19 pandemic and to financially support firms and households. (IHS Markit Economist Archbold Macheka)

-

- Against that backdrop, the government of Botswana's 2021/22 budget, presented to parliament on 1 February, includes a host of measures to restore fiscal sustainability through the short to medium term.

- To trim spending, the government proposes to reduce its wage bill, currently estimated at 15% of GDP, by abolishing "50% of vacant positions in value as of 1 April 2021". The Directorate of Public Service Management is also tasked to recommend measures to streamline the public service.

- The speedy roll-out of public services under the ERTP on digital platforms is expected to reduce the number of related personnel required in the workplace, potentially reducing the future wage bill further.

- With effect from 1 April 2021, value-added tax (VAT) is to be increased to 14% from 12%, a rate that the government deems still among the lowest in the world and indeed the Southern African Development Community region.

- The fuel levy is also to be increased, by BWP1 per liter, while withholding tax on dividends is to be levied at a rate of 10%, up from 7.5%.

- Other revenue-generating measures to be introduced include a levy intended to deter consumption of sweetened beverages, which will be implemented at a rate of BWP0.02 per gram of sugar above a content of 4 grams of sugar per 100 milliliters.

Asia-Pacific

- Most APAC equity markets closed higher except for India being unchanged; Hong Kong +1.9%, Mainland China +1.4%, Australia/South Korea +0.5%, and Japan +0.2%.

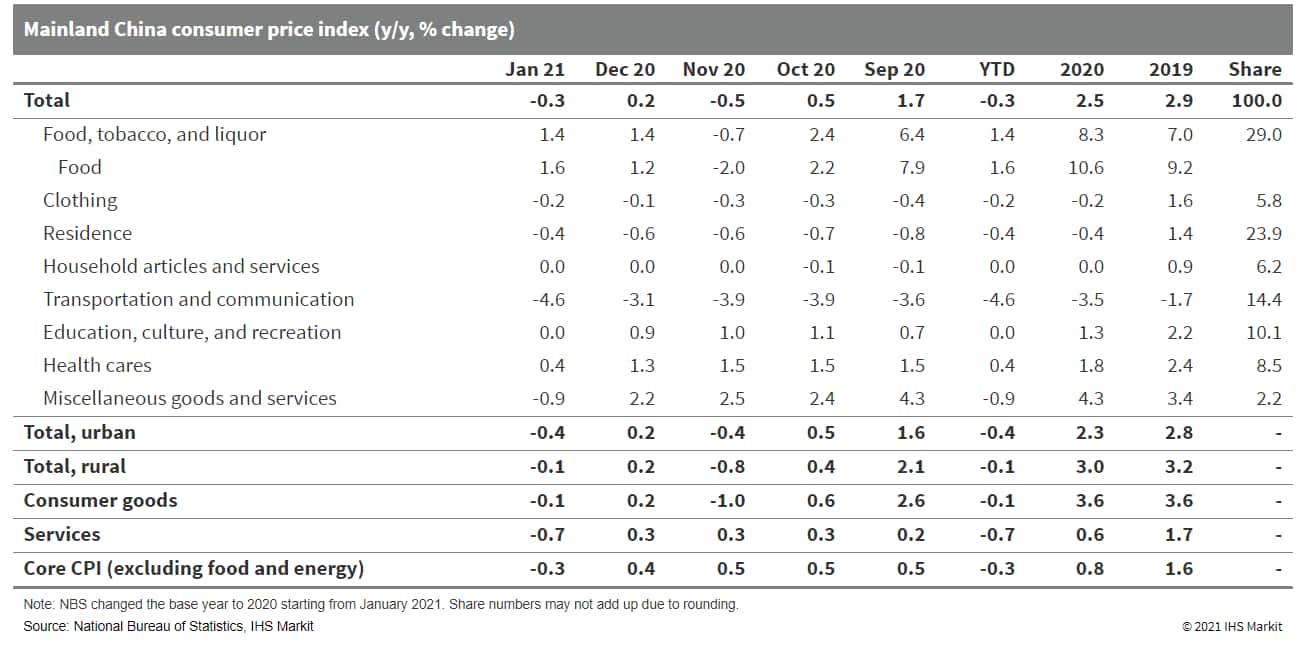

- Mainland China's consumer price index (CPI) fell by 0.3% year on year (y/y) in January 2021, down by 0.5 percentage points from the reading of December 2020, according to the data release by the National Bureau of Statistics (NBS). Month-on-month (m/m) CPI inflation further increased to 1.0%, up by 0.3 percentage points from a month ago and was the highest since January 2020. (IHS Markit Economist Lei Yi)

-

- By component, the headline CPI deflation in January was largely driven by 0.7% y/y decline in services prices, which reported an increase of 0.3% y/y last December.

- Notably, price deflation of transportation and communication widened to 4.6% y/y. As the Lunar New Year was in January in 2020 and the pandemic impact only started to emerge in late January, prices of transportation and tourism remained strong last January, therefore creating a high base for this year.

- Though prices of consumer goods dropped by 0.1% y/y in January, food price inflation edged up to 1.6% y/y on rising fresh vegetable and egg prices. Core CPI, excluding food and energy, registered deflation of 0.3% y/y, down by 0.7 percentage points from December's reading.

- With local outbreaks contained and the coming Spring Festival falling into a pandemic-induced low base month, non-food prices are expected to improve gradually in February. Despite the central bank increasingly flagging concerns for the leverage buildup in the economy, the likelihood of a sharp monetary tightening remains minimal for now. IHS Markit forecasts mainland China's full-year CPI to decline to 1.3% y/y in 2021 from 2.5% y/y in 2020.

- The auto market of mainland China experienced another month of growth in January, with new vehicle sales totaling 2.5 million units, up 29.6% from a year earlier. According to IHS Markit's January forecasts on mainland China's light-vehicle market, production volumes of passenger BEVs are expected to reach 1.74 million units this year and then increase to 2.35 million units in 2022. Light-vehicle production in mainland China is forecast to increase by 6% during 2021 to 24.8 million units, after a decline of 4.2% in 2020. (IHS Markit AutoIntelligence's Abby Chun Tu)

- Chinese electric vehicle (EV) startup WM Motor said on 9 February that it has reached an agreement with a group of banks and financial institutions for a credit line of CNY11.5 billion (USD1.78 billion). The first CNY3.5 billion has been granted by a group of banks, including Shanghai Pudong Development Bank, Agricultural Bank of China, Bank of China, and China Construction Bank. The capital will be used for the development of new products and the expansion of WM Motor's customer-experience-related operations such as digital marketing. (IHS Markit AutoIntelligence's Abby Chun Tu)

- Baidu has deployed a commercial autonomous bus, named Apolong, in Chongqing, China. Apolong, which is 4.4 meters long, 2.2 meters wide, and 2.7 meters high, can carry 14 passengers and has a battery life of 100 km. The driverless bus will transport people on a 3 km route around the mall atrium of Shin Kong Place in Chongqing's Yubei district. The journey will take 20 minutes and is currently being charged at half-price due to a promotion period, amounting to CNY25 (USD4), reports China Daily. (IHS Markit Automotive Mobility's Surabhi Rajpal)

- Japan's nominal monthly average cash earnings fell by 3.2% year on year (y/y) in December 2020, and the annual average for 2020 fell by 1.2% from the previous year. The largest decline since July 2009 was due largely to a 5.4% drop in special earnings (mainly seasonal bonuses), reflecting sluggish corporate financial performance because of the negative effects of the pandemic. (IHS Markit Economist Harumi Taguchi)

-

- The sluggish recovery of economic activity severely affected cash earnings in accommodation, eating, and drinking services (down 13.2% y/y), life-related services (down 13.6% y/y), and transportation and postal services (down 8.8% y/y). A continued decline in hours worked also weighed on cash earnings, although the contraction of non-scheduled hours worked narrowed to 7.6% y/y.

- Cash earnings are likely to remain sluggish over the coming months because of the sustained negative effects of the pandemic. In addition to downside for areas covered in the state of emergency, which seeks cuts in operation hours after 8:00 pm and the promotion of working-from-home, the resurgence of COVID-19 has made consumers cautious about going out.

- The Delhi state government has launched a new "Switch Delhi" initiative to raise awareness and promote electric mobility in the city, reports the Economic Times. As part of the campaign, the state government will only hire electric vehicles (EVs) in the next six weeks. "Our vision is that by 2024, 25% of new vehicles must be electric. Approximately Rs30,000 [in] subsidies are to be given for two- or three-wheelers [and] INR150,000 [USD2,055] for four-wheelers. We are starting the 'Switch Delhi' campaign today to make people aware of clean vehicles," said Delhi chief minister Arvind Kejriwal. (IHS Markit AutoIntelligence's Isha Sharma)

S&P Global provides industry-leading data, software and technology platforms and managed services to tackle some of the most difficult challenges in financial markets. We help our customers better understand complicated markets, reduce risk, operate more efficiently and comply with financial regulation.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.