Research — August 29, 2025

Community bank earnings stand up to tariffs for now

By Zain Tariq and Nathan Stovall

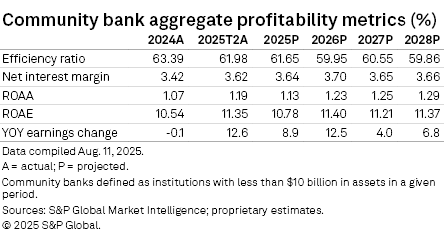

US community banks' strong expansion in net interest margins has bolstered earnings in the first half of 2025, but the delayed impact of tariffs will surface in the coming quarters and slow loan growth and push credit costs higher.

Modest declines in funding costs and the repricing of fixed rate assets from the pandemic era has fueled margin expansion at community banks and double-digit earnings growth through the first six months of the year. Margins are still expected to expand further, but earnings growth should not be as strong in the second half of 2025 as the lagging impact of tariffs slow growth, weigh on the consumer and push delinquencies higher and require banks to build reserves. Those modest earnings headwinds should provide further support for stronger bank M&A activity as institutions seek ways to grow.

Click here to access data exhibits and the US community bank aggregate's projections template.

Fixed asset repricing bolsters community bank margins

Community banks will continue to benefit from remixing their balance sheets as lower-yielding securities mature and are reinvested at higher yields, while fixed rate loan yields originated during the pandemic roll off and are replaced with new credits carrying more attractive yields.

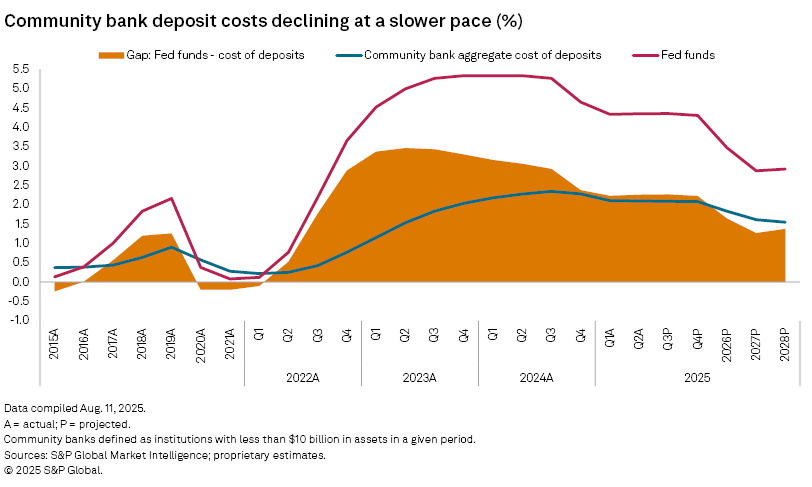

Declines in deposit costs have also supported margin expansion in recent quarters, but the pace of decline has slowed. Community banks' cost of deposits dipped 1 basis point quarter over quarter in the second quarter. That decrease pales in comparison to the 17 basis points linked quarter decline in the first quarter and 7 basis points quarter over quarter decrease in the fourth quarter. Even while holding the line on the deposit costs, community banks failed to attract new funds in the second quarter as deposit balances actually declined in the period.

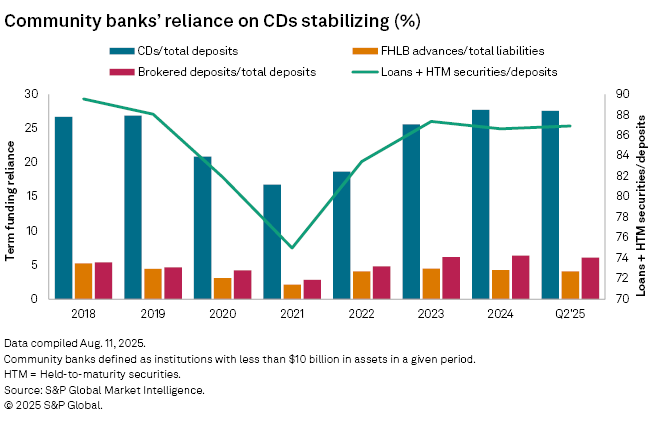

Community banks recorded significant pricing relief in prior quarters because they shed higher cost CDs originated when deposit competition was far fiercer. Pricing on CDs has significantly influenced deposit costs since community banks relied heavily on CDs to bolster their funding during the recent tightening cycle.

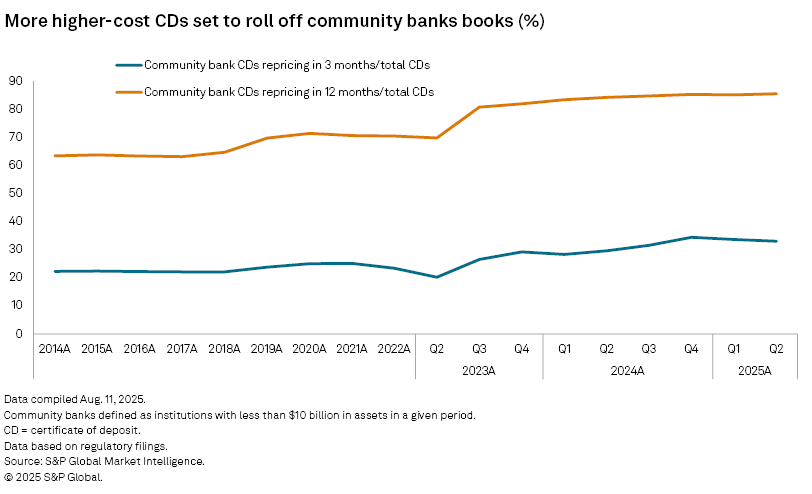

Banks grew CDs as deposit pricing competition reached a fever pitch in the last six months of 2023 and the early part of 2024. That period followed the liquidity crunch in the spring of 2023 that led to a trio of large bank failures. For community banks, the vast majority of CDs originated at that time have since matured. For instance, at the end of the second quarter of 2024, 84.1% of CDs were set to mature a year later.

When CDs mature, most banks have to meet market rates to retain the deposits. CD rates began declining late in the third quarter of 2024 and far fewer institutions are offering the products at rates over 4%, but there has been less movement around the 3.5% level. The number of banks marketing one-year CDs over 3.5% included 1,053 institutions as of Aug. 8, up slightly from 1,048 as of June 27, but down from 1,079 as of March 28, 1,134 as of Dec. 27, 2024, and 1,266 as of Sept. 27.

Banks would like to cut deposit costs further but need to remain competitive with alternatives in the Treasury and money markets. The difference between the average fed funds rate — a proxy for those alternatives — and the community bank aggregate's cost of deposits widened slightly in the second quarter of 2025 from the prior quarter. Still, the gap remained far narrower than in 2023 and 2024.

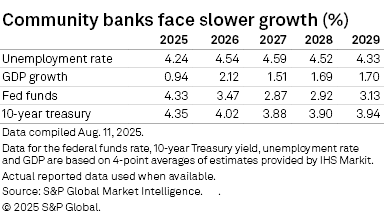

Community banks likely need additional rate cuts by the Fed to record notable declines in deposit costs in future quarters. S&P economists do not expect the quarterly fed funds rate to decline by at least 25 basis points from current levels until the first quarter of 2026.

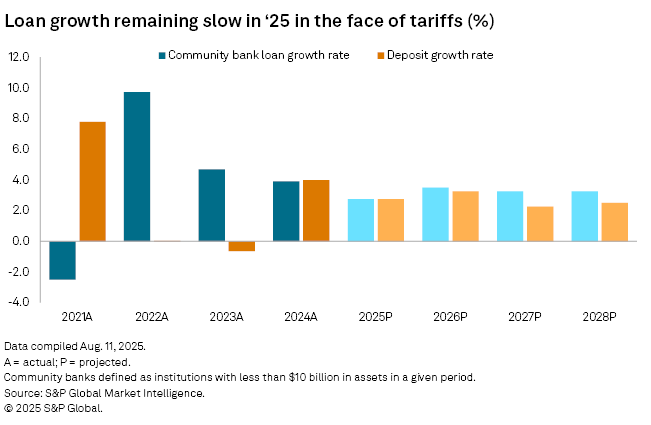

Deposits should grow further, but interest-bearing deposits will continue to grow at a quicker clip than non-interest-bearing deposits — banks' most prized source of funding.

Loan growth is expected to remain relatively weak as borrowers digest new trade policies that could change the cost of operating their businesses and households. The impact of tariffs arguably have not been felt as businesses increased inventories ahead of the landmark announcements in early April. Building inventories has allowed some businesses to maintain prices at pre-tariff rates, for now.

Weaker loan growth offers one silver lining for banks. If loan growth is slower, community banks' funding need would not be as great and could allow them to price deposits incrementally lower.

Credit quality still normalizing but potential signs of weaker economic conditions

Bankers maintained during second-quarter earnings season that credit quality remains benign, and the US economy has proven resilient in the face of uncertainty created by tariffs. However, credit quality has normalized with delinquencies rising off historical lows.

In the second quarter, nonaccrual loans at the community bank aggregate rose modestly to 0.67% of loans from 0.65% in the first quarter. That compares to 0.56% in the second quarter of 2024 and 0.43% in the second quarter of 2023.

Much of the concern in the investment community has related to commercial real estate loans. Some CRE borrowers face a double whammy of lower cash flows due to the rise of hybrid work and higher debt service stemming from increases in interest rates over the last few years. CRE nonaccruals have risen for 10 consecutive quarters at the community bank aggregate, but losses have often been less than many feared, in part due to well-funded distressed investors and private credit firms targeting the asset class. When banks have sold CRE loans — often in connection with an acquisition — sellers have recorded relatively modest discounts to par, ranging from 8% to 10%.

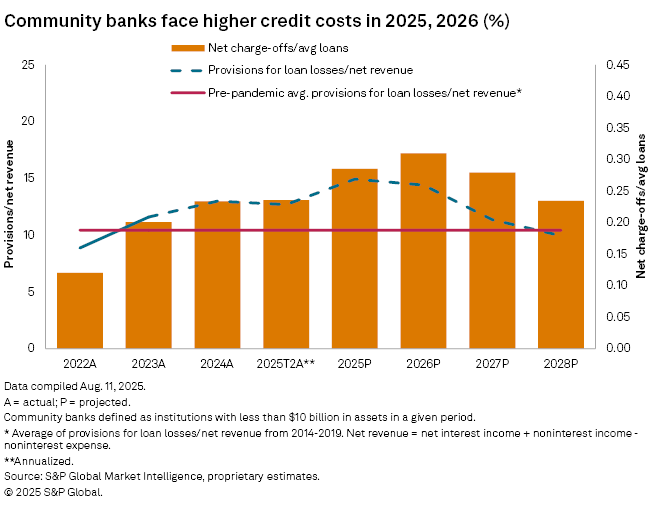

We expect related refinancing challenges to result in defaults and higher loss content in 2025 and 2026, with net charge-offs continuing to rise from benign levels. We expect loss content to linger as banks provide borrowers with extensions in the face of some maturity walls.

Consumer delinquencies have risen from historical lows as well. While many community banks might not have sizable consumer or credit card portfolios, the consumer drives the economy. Currently, the US consumer is stretched — consumer spending and savings rates have slowed, and excess savings accumulated during the pandemic have been exhausted. Many businesses seem to have absorbed the cost of tariffs thus far, but it seems likely that some of those costs will eventually be passed on the consumer.

Community banks have assumed that greater stress lies ahead and have set aside considerable reserves for the most troubled projects. At the end of the second quarter of 2025, reserves rose modestly to 1.30% of loans. We expect further increases by year-end 2025 and small reserve builds in 2026 as economic uncertainty pushes banks to prepare for trouble ahead. Net charge-offs should rise in 2025, but losses and the reserves required to fund them should serve as a modest headwind to earnings rather than a severe downturn.

Provisions are projected to rise to 14.9% of net revenue in 2025 and hold fairly steady at 14.4% in 2026. That level of provisions would represent a larger headwind to earnings than seen in recent periods, with provisions equating to 12.7% of net revenue through the first half of 2025, 13.0% in 2024 and 11.6% in 2023. On average, from 2014 to 2019, banks' provisions equated to 10.4% of net revenue.

Looking ahead

We think community banks would be wise to price greater risk into their loan portfolios and consider rethinking their growth goals. Bankers will likely find that strong loan growth will be tough to come by and could be prudent to avoid pressuring lenders aggressively at this point in the cycle.

Rather than fighting to meet their organic growth goals, bank managers should move in the other direction and encourage lenders to tighten pricing and lending standards, increase debt service coverage ratios and move away from their least credit worthy borrowers.

While lower loan volumes may reduce earnings in the near term, avoiding risk today could pay dividends later and help banks minimize credit losses. The approach could also help institutions to improve their funding bases, which represent the true value of a banking franchise.

A stronger funding base and continued strength in credit quality would be rewarded by investors and appeal to potential acquirers. Banks that are willing to take a step back and operate more cautiously now will also have a greater opportunity to continue growing, both organically and through acquisitions, when the next downturn occurs.

While M&A activity has remained relatively slow, the pace of deal activity seems poised to increase. A friendlier regulatory environment has brought back serial acquirers, and the combination of modestly higher credit costs and slower loan growth could create more willing sellers. Greater interest from institutions looking to partner with buyers could come as bank valuations have recovered from the lows in April, setting the stage for much stronger dealmaking activity.

Scope and methodology

The outlook discussed in this article is based on a proprietary S&P Global Market Intelligence model that utilizes the actual results of nearly 10,000 active and historical commercial and savings banks and savings and loan associations. The outlook is based on management commentary, discussions with industry sources, regression analysis, and asset and liability repricing data disclosed in banks' quarterly call reports. While taking into consideration historical growth rates, the analysis often excludes the significant volatility experienced in the years around the credit crisis.

The outlook is subject to change, perhaps materially, based on adjustments to the consensus expectations for interest rates, unemployment and economic growth. The projections can be updated or revised at any time as developments warrant, particularly when material changes occur.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.