Research — July 13, 2026

Visible Alpha breakdown of US banks’ second-quarter 2026 earnings expectations

By Jigar Saiya

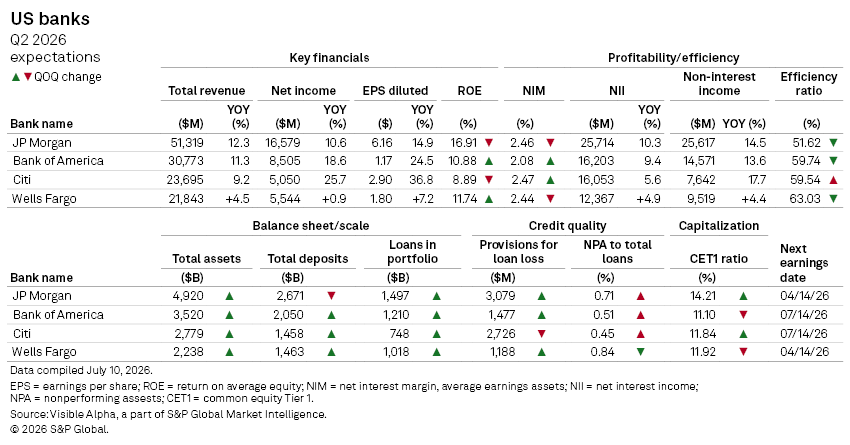

The big four US lenders will kick off second-quarter earnings season on Tuesday, July 14. Based on Visible Alpha consensus estimates, JPMorgan Chase (NYSE: JPM), Bank of America (NYSE: BAC), Citigroup (NYSE: C), and Wells Fargo (NYSE: WFC) are all poised for strong earnings growth in Q2, with consensus estimates pointing to broad-based top-line growth.

JPMorgan is expected to report adjusted earnings of $6.16 per share on revenue of $51.3 billion, with consensus diluted EPS estimate revised up 11.83% in the last one month. Bank of America is expected to earn $1.17 per share on $30.8 billion in revenue, with year-on-year EPS growth of around 24% and estimates lifted up 2.66% over the past month.

Citigroup and Wells Fargo are expected to post diluted EPS of $2.90 and $1.80, respectively, with consensus estimates increasing 9.0% and 5.9% over the past month.

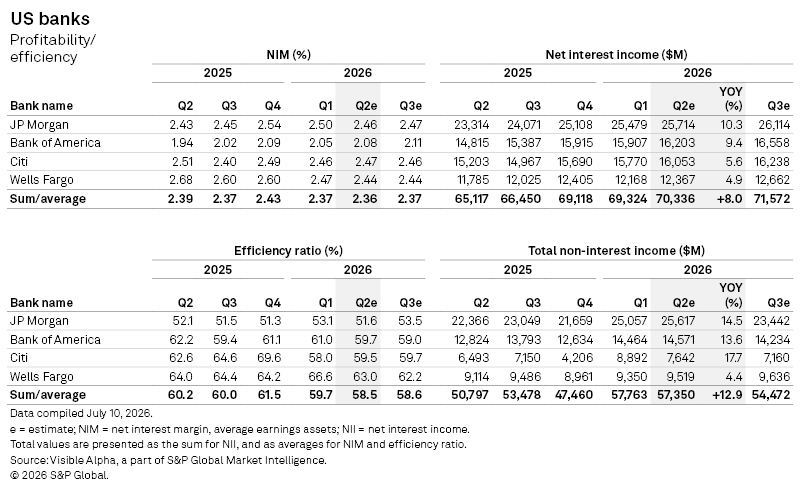

Net interest margins remain mixed

Despite improving revenues, lending profitability remains uneven. Net interest margins (NIM) are expected to remain broadly stable in Q2, averaging 2.36% across the four largest banks, down slightly from last quarter. Bank of America is expected to post the strongest sequential NIM improvement, while JPMorgan and Wells Fargo are expected to see modest NIM declines. The mixed margin outlook will remain a key area of focus as banks navigate changing funding costs and evolving expectations for US interest rates.

Despite the muted margin outlook, higher earning assets are expected to drive net interest income (NII) higher across the group. Aggregate NII is forecast to increase 8% year-on-year, led by JPMorgan. NII growth is supported by an expected 8.1% loan growth on an aggregates basis, mainly commercial loans.

Non-interest income is expected to grow faster than NII across banks, with the exception of Wells Fargo, highlighting the increasing importance of fee-based businesses as lending margins normalize.

Meanwhile, operating efficiency is expected to improve modestly. The average efficiency ratio is forecast to decline to 58.7% from 59.7% in the previous quarter, indicating better cost control. Bank of America and Wells Fargo are expected to post the biggest improvements, while Citi is projected to see efficiency ratio slightly edge up. Banks have continued to highlight their focus on expense management through headcount rationalization, while continuing to re-invest in technology, AI and process re-engineering across business segments leading to higher productivity.

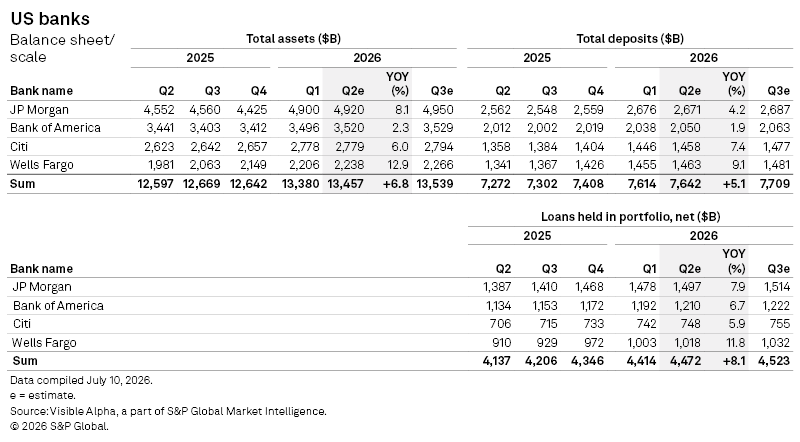

Loan growth gathers pace

Asset and deposit growth is expected to remain healthy across the banks. Wells Fargo is projected to record the fastest asset and deposit growth among peers.

Loan growth is expected to outpace deposit growth across the banks, suggesting improving credit demand. Wells Fargo is expected to post the strongest loan portfolio expansion, with loans rising 11.7% year-on-year. Overall, analysts expect loan growth, especially commercial and industrial loans, to boost NII across banks.

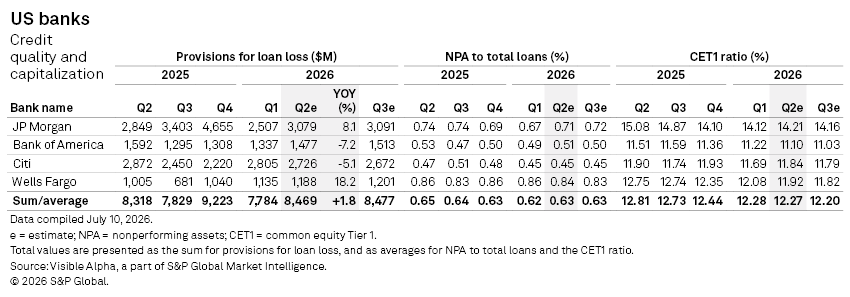

Credit quality remains resilient

Aggregate provisions for credit losses are forecast to rise a modest 1.8% year-on-year, although the trend varies across banks. Wells Fargo is expected to post the largest increase, with provisions rising 17.8%, while JPMorgan's reserves are projected to increase 8.3%. In contrast, Bank of America and Citigroup are expected to see provisions decline.

Asset quality remains robust across the sector. The average non-performing assets (NPA)-to-total loans ratio is expected to hold broadly steady at 0.63%, with all four banks maintaining ratios below 1%.

Capital positions also remain strong despite ongoing shareholder distributions and business growth. The average Common Equity Tier 1 (CET1) ratio is expected to ease slightly to 12.26% from 12.28% in the prior quarter. JPMorgan is forecast to retain the strongest capital position, while Citi is expected to improve its ratio to 11.83%. Bank of America and Wells Fargo are projected to see modest declines, though both remain comfortably above regulatory minimums.

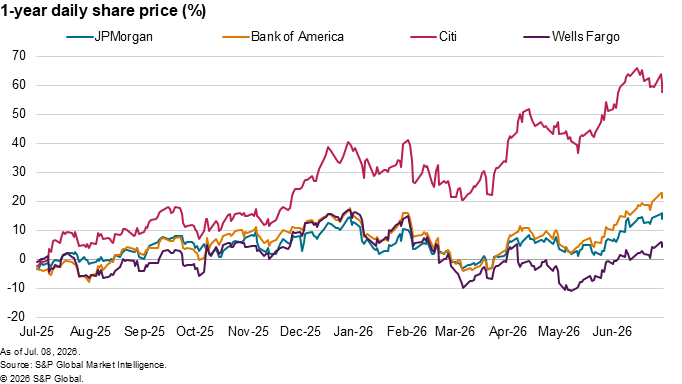

Bank shares have rallied sharply since mid-May, supported by easing geopolitical concerns, resilient US economic data and renewed optimism over capital markets activity.

As banks reports earnings next week, the focus is expected to be less on whether banks beat quarterly estimates and more on management commentary around loan demand, NII, capital deployment and the outlook for the second half of 2026.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment