Research — July 15, 2026

Visible Alpha breakdown of Indian bank’s Q1 FY2027 earnings expectations

By Pranay Deshmukh and Jigar Saiya

India’s banking earnings season is set to begin on Friday, July 17, with leading private-sector lenders HDFC Bank (NSE: HDFCBANK) and ICICI Bank (NSE: ICICIBANK) scheduled to report their first-quarter ending June results.

After a resilient March quarter, when healthy loan growth and stable asset quality helped offset pressure from a lower interest-rate environment, the focus this quarter is expected to shift from growth alone to the sustainability of margins as the Reserve Bank of India’s easing cycle works through bank balance sheets.

Visible Alpha consensus points to a broadly healthy start to FY 2027 for India’s largest public and private-sector lenders, with loan growth expected to remain robust and credit quality steady. However, the impact of cumulative RBI rate cuts is likely to emerge as a central theme during earnings calls, with analysts watching closely for commentary on loan repricing, deposit competition and the trajectory of net interest margins (NIMs).

The RBI reduced the repo rate to 5.25% in December 2025, following a cumulative 125 basis points of cuts during 2025. Since then, the central bank has kept rates unchanged, including at its June 2026 meeting, when it maintained the repo rate at 5.25%.

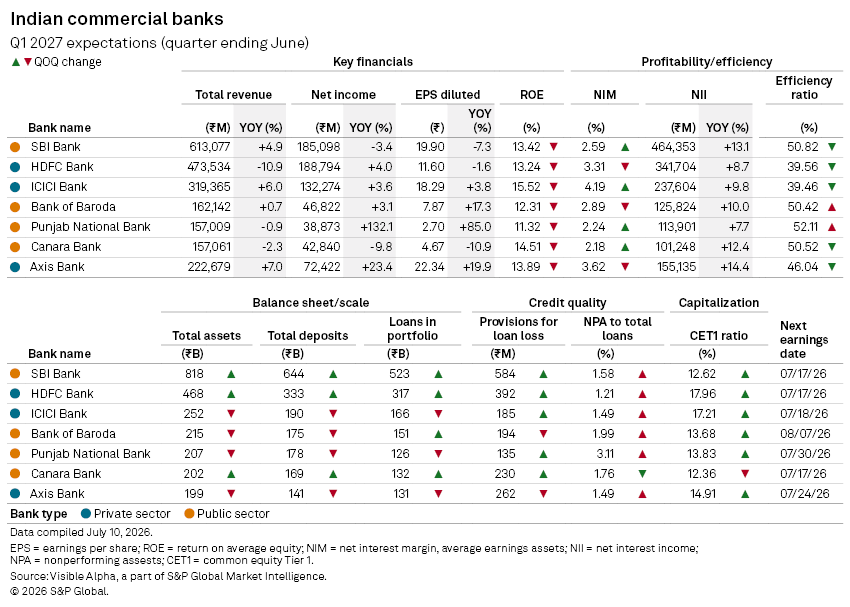

Looking at top line expectations for Q1, among the large banks, Axis Bank (NSE: AXISBANK) is expected to deliver the strongest revenue growth, with total revenue forecast to rise 7% year-on-year to ₹223 billion. By contrast, HDFC Bank revenue is forecast to decline 10.9% year-on-year, reflecting a tougher comparison following the benefits from its merger with Housing Development Finance Corp. and continued pressure on margins as the enlarged balance sheet adjusts to a lower-rate environment.

Profit trends are expected to vary more significantly. Axis Bank is forecast to again lead among major lenders, with net operating profit after tax (NOPAT) rising 33.2% year-on-year. Punjab National Bank (NSE: PNB) is expected to post the sharpest improvement, with NOPAT surging 132.1%, although this reflects a weak year-ago comparison.

State Bank of India (NSE: SBIN) and Canara Bank (NSE: CANBK) are projected to report modest declines in profitability.

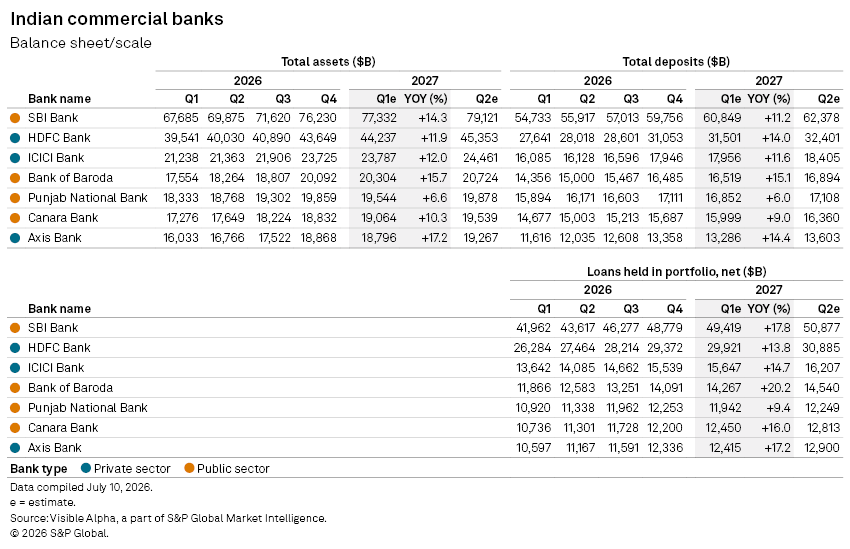

Loan growth to remain robust while banks expand deposits and assets

Credit expansion is expected to remain a bright spot for Indian banks, with six of the seven lenders forecast to deliver double-digit [PH1.1]year-on-year growth in net loans held in portfolio.

Bank of Baroda (NSE: BANKBARODA) is expected to record the strongest loan growth, with its loan portfolio rising 20.2% year-on-year. Among private-sector lenders, Axis Bank is projected to lead with loan growth of 17.2%.

Deposit growth is also expected to remain healthy, helping banks maintain funding capacity as demand for retail and corporate credit continues. However, competition for deposits remains a key watch point, particularly as banks attempt to preserve margins in a declining-rate environment.

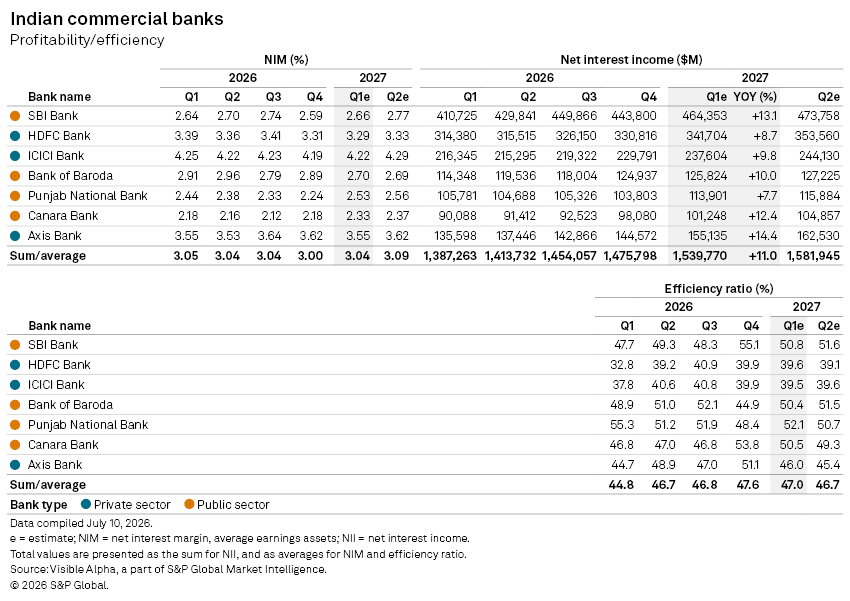

Margin trends diverge; NII growth to remain resilient

Net interest income (NII) is expected to remain resilient. Aggregate NII for the seven banks is forecast to rise 11% year-on-year, supported by continued loan growth. However, margin performance is expected to diverge. NIMs are forecast to remain broadly stable or decline in the June quarter, as the benefit from lower deposit costs only partially offsets pressure from lower-yielding corporate loans and elevated bulk deposit rates.

Bank of Baroda is expected to experience the sharpest margin contraction, with NIM declining 19 basis points sequentially. Axis Bank and HDFC Bank are also expected to see modest pressure, with margins falling 7 basis points and 2 basis points, respectively. Punjab National Bank is expected to see the highest growth, with NIM expanding 29 basis points sequentially to 2.53%.

Operational efficiency is expected to improve across most lenders. Axis Bank is forecast to report the strongest improvement, with its efficiency ratio declining 510 basis points quarter-on-quarter to 46%. SBI and Canara Bank are also expected to record improvements, with efficiency ratios falling 430 basis points and 330 basis points, respectively.

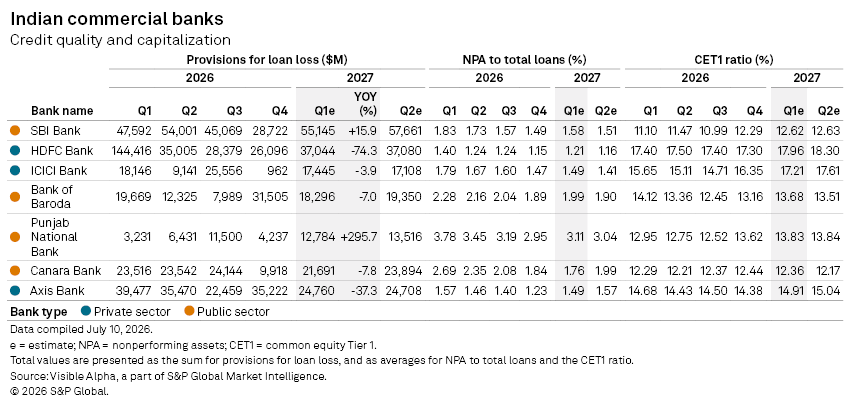

Asset quality continues to improve as capital buffers remain strong

Asset quality is expected to remain supportive of earnings. Non-performing asset (NPA) ratios are expected to remain below 2% for all banks except for Punjab National Bank at an estimated 3.11%. HDFC Bank is expected to report the lowest NPA-to-loan ratio at 1.21%.

Provision expenses are generally expected to remain manageable, suggesting no material deterioration in credit costs. HDFC Bank's provisions are expected to decline 74% year-on-year and Axis Bank's by 37%, while State Bank of India and Punjab National Bank are expected to increase provisions by 18% and 370%, respectively. These differences appear to reflect institution-specific provisioning strategies rather than a broad deterioration in credit quality.

Common Equity Tier 1 (CET1) ratios are expected to improve or remain stable across most banks, providing ample capital to support future lending growth. HDFC Bank is forecast to maintain one of the strongest capital positions with a CET1 ratio of 17.96%, while Canara Bank is expected at 12.36%.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment