ECONOMICS COMMENTARY — 02 Jul, 2026

US manufacturers report further strong output growth, in June but jobs are cut as optimism fades

US manufacturers reported a further marked improvement in growth of output and order books in June, according to S&P Global’s PMI data, extending the growth spell that has been reported since the outbreak of the war in the Middle East. Employment was nevertheless cut sharply as firms often sought to offset rising costs of energy and raw materials. Supply chain delays and upward price pressures continued to be widely reported, albeit moderating thanks to recent news of an improving situation in the Middle East. However, despite the recent drop in energy prices and brighter outlook for shipping, business confidence fell sharply, in part reflecting concerns that an end to war-related inventory building could start to act as a drag on sales.

Solid output growth

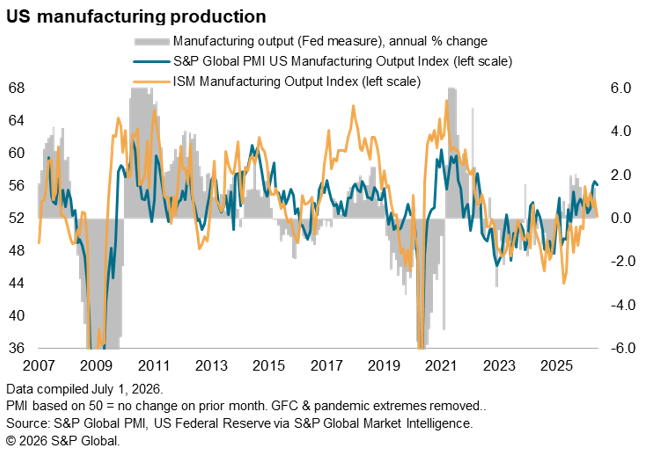

S&P Global’s US Manufacturing PMI surveys indicated strong output growth in June, closing out the best calendar quarter for nearly five years.

Although not as impressive as the earlier ‘flash’ estimate and dipping from May’s recent high, the PMI Output Index for June signaled the second-strongest increase in factory production since April 2022. Production growth has been especially impressive over the second quarter, expanding on aggregate at the fastest pace since the third quarter of 2021.

Stock build boosts demand

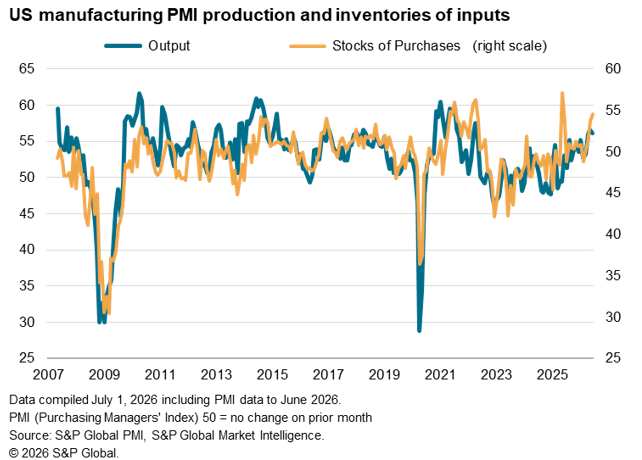

Driving the upturn in production was a further marked increase in new orders received by factories. However, in both cases, the expansion was in part a reflection of further safety stock building, as manufacturers and their suppliers and customers alike sought to build inventories ahead of potential supply shortages or price hikes. Stocks of purchased inventory, for example, posted one of the largest gains in the history of the survey during June, beaten only by the accumulations seen in the pandemic, the invasion of Ukraine and last year’s tariff announcements.

Anecdotal evidence collected via the June PMI surveys indicate that this inventory build added around 2-3 index points to the PMI output, new orders and input buying survey gauges, albeit still implying moderate growth in each case.

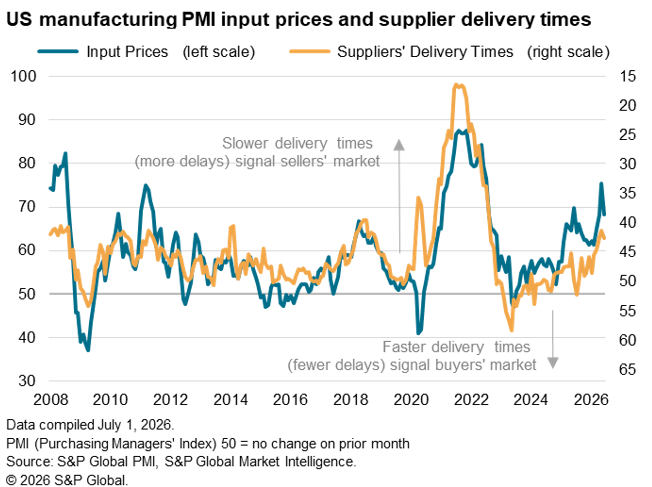

Safety stock building remained prevalent as supply chain delays were again widely reported in June and were commonly cited as causing producers’ input costs to have risen sharply again. Since the outbreak of the war in the Middle East, the price and supply shock has been the greatest seen since the invasion of Ukraine exacerbated post-pandemic price and supply issues in 2022. However, we note that tariff-related supply issues and associated higher import costs continue to be reported alongside the impact of the war.

Encouragingly, the reporting of supply delays and higher input costs showed some signs of easing in June from the recent highs seen in May, attributed to the lower energy prices seen during June and the easing of some supply concerns emanating from the closure of the Strait of Hormuz. Although both gauges foretell higher consumer price inflation to come in the months ahead, as price pressures feed through with a lag to the end consumer, the falls in June at least hint at a potential peaking in these inflationary pressures.

Employment slumps

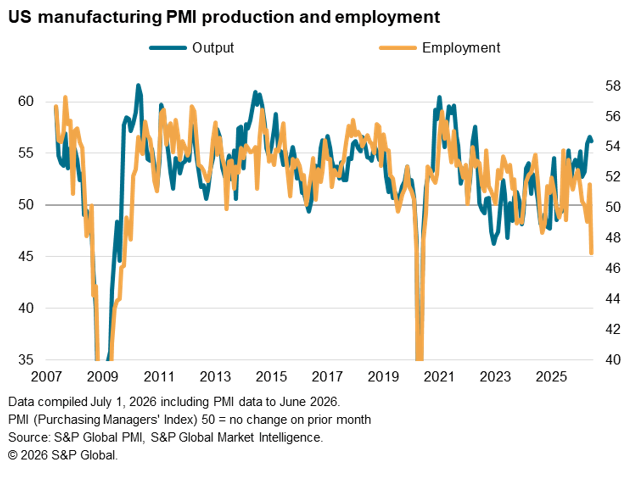

Despite the rise in order book inflows and production, firms reported lower employment levels. In fact, June saw the largest drop in factory payroll numbers since the early pandemic months in the first half of 2020. Although the fall came on the heels of a rise in headcounts in May, factory jobs have now been cut among PMI respondents on average in two of the past three months, with the employment trend having weakened since the summer of last year.

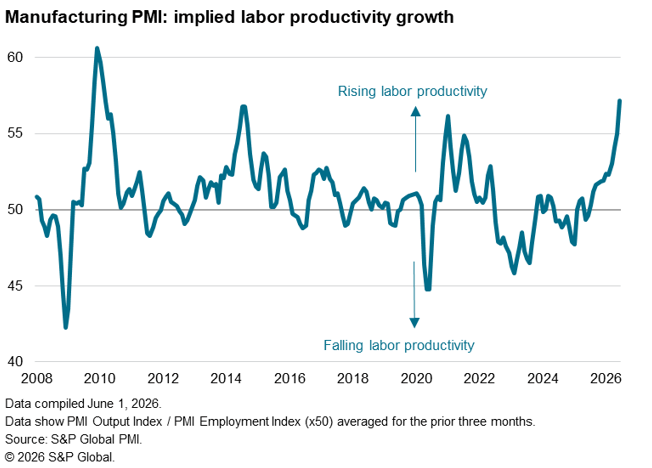

Productivity gains

The combination of sharply rising production and falling employment implies rising productivity. The last three months have in fact seen the biggest improvement in output per worker indicated by the PMI survey since the productivity gains seen in the recovery from the depths of the global financial crisis over 15 years ago.

Higher productivity was largely intended: jobs were cut in many companies in response to firms citing the need to reduce overheads in the face of rising energy and raw material prices amid an uncertain economic outlook. Productivity improvements have been aided by technological, and in particular AI, advances. You can read our report on AI adoption here.

However, it was not all about deliberate cost savings, roughly one-in-five companies reporting lower employment cited a lack of suitable candidates to fill vacant positions, hinting at constrained production and expansion.

Gloomier outlook

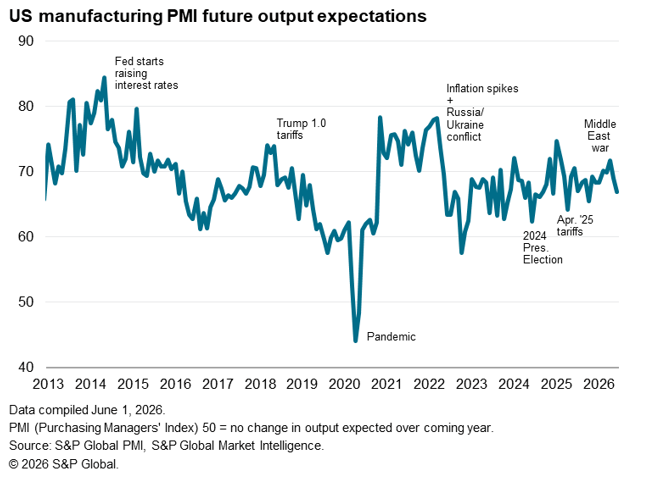

One further contributor to lost jobs was a drop in business confidence. Despite the June data collection period seeing sharply lower energy prices and including the signing of an MOU between the US and Iran to reopen the Strait of Hormuz, US manufacturers’ expectations of their own output over the coming 12 months deteriorated to the gloomiest since last October, contrasting markedly with the 14-month high seen back in April.

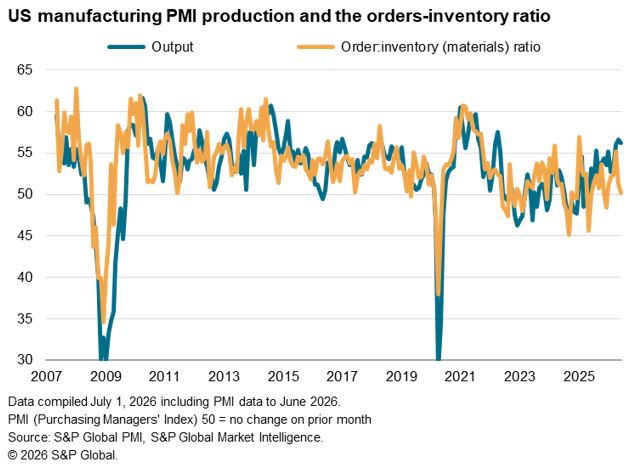

One reason hinted at by the anecdotal evidence collected in the June PMI is that companies are anticipating a pull-back in purchasing by customers now that war-related price and supply worries have started to ease. This inventory cycle drag is also hinted at by the survey’s new orders to inventory ratio, which is often a reliable indicator of future production trends, which fell sharply in June.

On balance, it therefore seems that producers are telling us that the risks to the near-term outlook are skewed to the downside.

Access the latest PMI press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings