ECONOMICS COMMENTARY — 08 Jul, 2026

Global PMI shows inflation rates peaking amid lower oil prices

Global selling price inflation cooled in June amid lower energy prices, according to PMI survey responses, though overall rates of inflation remain elevated by standards seen over the past four years, notably for consumer goods and services.

Inflation peak

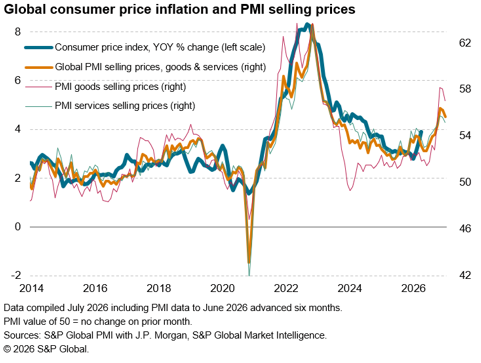

Measured across both goods and services, average prices charged rose sharply again worldwide in June, according to PMI survey data, though the rate of inflation cooled from a month prior.

The J.P. Morgan Global PMI Prices Charged Index – compiled by S&P Global – fell from 56.2 in May to 55.7 in June, dropping for a second successive month to point to slower price growth.

The survey data therefore hint at global inflationary pressures having peaked back in April, though with the rate of inflation continuing to run at a historically elevated pace. Comparisons with official data indicate that June’s PMI price gauge is broadly consistent with global consumer price inflation running at an approximate 4.5% annual rate. The second quarter as a whole has seen the steepest global price growth since late 2022.

While goods price inflation has risen especially sharply since the outbreak of war in the Middle East, hitting levels not seen since 2022 and remaining particularly elevated in June, service sector inflation has also risen markedly, running at a three-year high in the second quarter on average. However, the respective rates of increase cooled to three-month lows in both manufacturing and service sectors in June.

Energy price drop

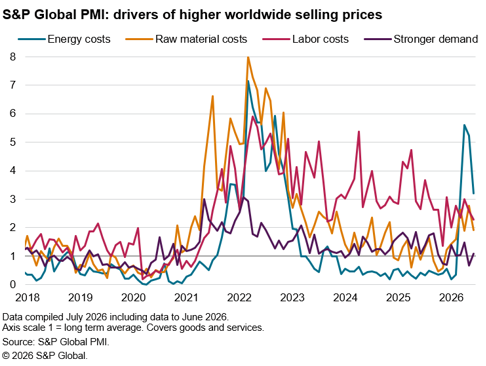

Key to the cooler rates of inflation was a sharp drop in energy prices during the month, reflecting the drop in oil prices thanks to the easing of tensions in the Middle East.

At the same time, upward pressure on prices from non-energy raw material prices and labour costs also moderated in June.

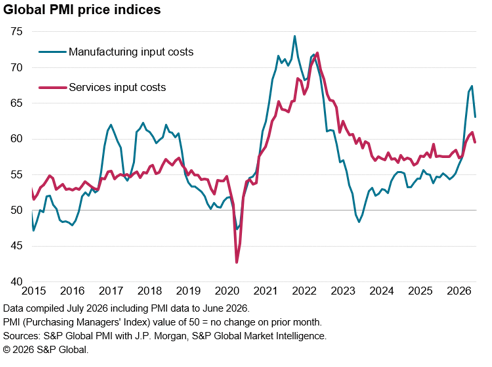

Overall growth of input costs in June consequently slowed to its weakest since February, moderating across both goods and services. A contributing factor in manufacturing was also a softening of supply chain disruptions, albeit with delays remaining widespread, in part linked to curbed trade flows through the Strait of Hormuz.

Consumer-facing sectors still report elevated inflation

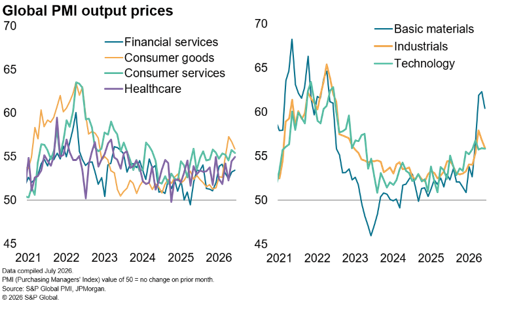

The cooling of selling price inflation was led globally by the basic materials sector, though this remained the sector with steepest overall rate of price increase. Elevated rates of inflation also continued to be reported in the technology sector, unchanged on May, and for industrials, albeit the latter down to a three-month low.

While also cooling, rates of increase for both consumer goods and consumer services prices also remained stubbornly high despite the steep drop in oil prices during June, to suggest some further pass-through to national consumer inflation rates is likely. Higher interest rates meanwhile contributed to accelerated inflation for financial services charges.

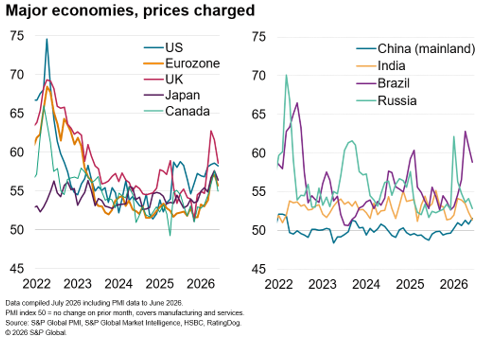

Rates of inflation cool across all major economies bar mainland China

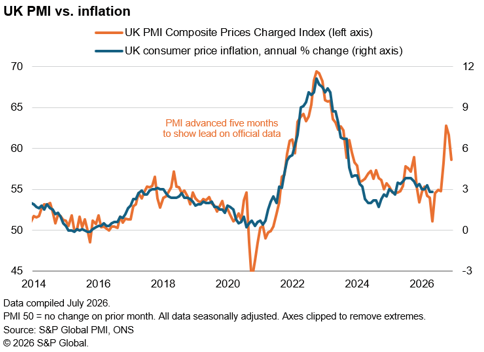

The UK and Brazil, which had reported especially steep rates of selling price inflation (across goods and services) in prior months, both saw sharply reduced rates of selling price inflation in June. In both cases, rates nonetheless remained elevated both historically and internationally.

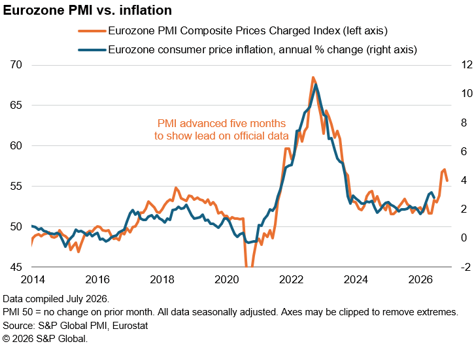

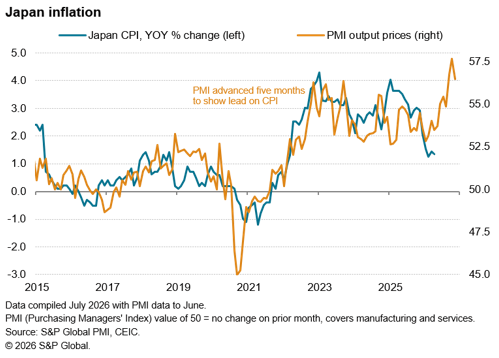

While rates of selling price inflation also slowed in the eurozone, Japan and Canada, rates remained high by standards seen over the past four years, with Japan’s rate notably running among the highest recorded over the history of the survey.

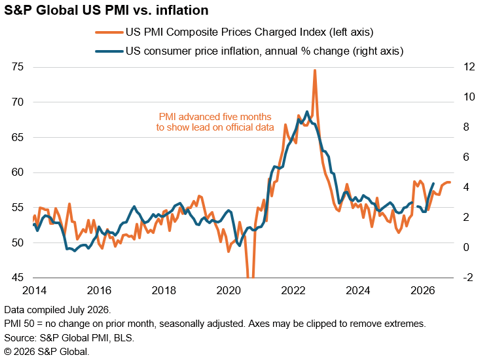

US selling price inflation also moderated but only very slightly to also hold at one of the highest rates seen over the past four years.

In the emerging markets, the cooling rate of inflation in Brazil was accompanied by slower rates of increase in both India and Russia, but price growth ticked higher in mainland China to the fastest since February 2022, bucking the global easing trend, though remained modest by international standards.

Major economies, PMI vs. CPI comparisons

The June PMI data suggest that consumer inflation rates may have further to rise in the major economies as firms pass cost increases down to final consumers. However, the PMI data also hint at a peaking of consumer price inflation in the coming months before rates start to head lower, barring further energy prices spikes.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings