ECONOMICS COMMENTARY — 06 Jul, 2026

Emerging markets show greater war resilience to outpace advanced economies

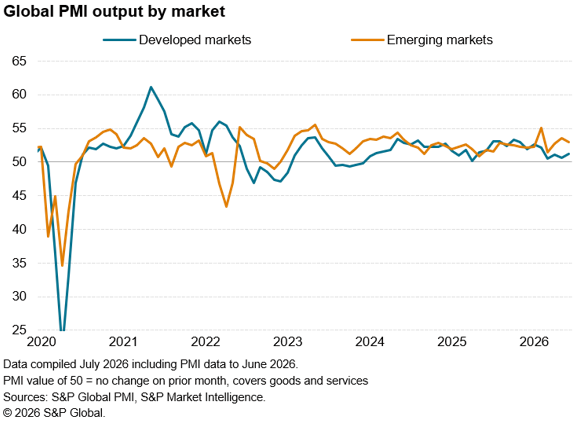

Worldwide PMI survey data from S&P Global showed global economic growth picking up slightly in June but remaining subdued compared to the pace seen at the start of the year. However, while the war in the Middle East has so far dampened growth in the developed markets to one of the slowest for two-and-a-half years, growth has proven more resilient in the emerging markets, outperforming the developed world so far this year to the greatest extent since 2024.

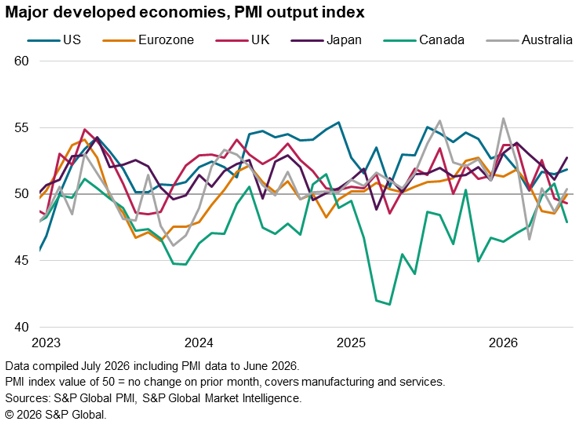

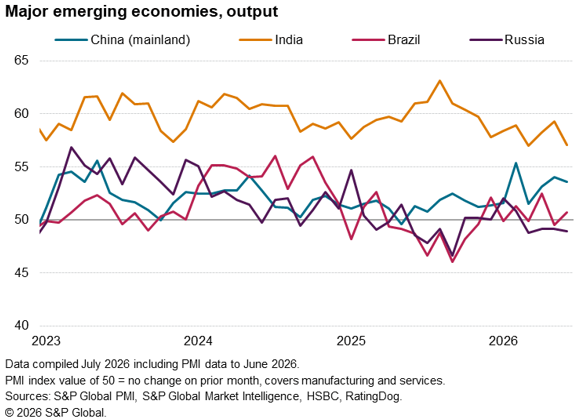

Trends have varied markedly within these markets, however. In the advanced economies, Japan is enjoying a growth spurt and the US has sustained a modest expansion, albeit weaker than earlier in the year, while Europe has largely stalled and Canada has slipped back into decline. In the emerging markets, best-performer India has seen growth weaken but mainland China reported its best growth spell for three years in the second quarter.

Global PMI edges higher in June

Survey data indicated that global economic growth picked up in June amid improved news out of the Middle East. The J.P.Morgan Global Composite PMI Output Index ticked higher for a third successive month, up from 51.9 in May to 52.0 in June.

Japan leads advanced economies

Output growth across the advanced economies accelerated in June to the fastest since February, but with the UK and Canada bucking the improved trend. Furthermore, at 51.2, the developed world PMI output index continued to sign only modest growth, continuing the weak spell that has been evident over the past four months following the outbreak of the war in the Middle East.

Not all advanced economies are seeing sluggish growth, however. Japan was the best performer, with output growth perking up from May’s five-month low to the highest since March. Improved manufacturing growth was matched by a revival of growth in the previously-stalled services economy. Japan’s factories notably reported the largest expansion of output for just over 12 years during the three months to June.

The US also reported ongoing growth consistent with the economy growing at a 1.2% annualised rate, the pace ticking up to the fastest since February. A slight cooling in the recent manufacturing growth spurt was offset by faster, though still only modest, services growth.

The eurozone reported unchanged output, stabilising after two months of contraction, reflecting stronger manufacturing output growth and a moderation of the service sector downturn. The eurozone PMI indicates flat GDP in the second quarter. While the UK PMI showed output falling for a second month in June, underpinned by declining services output. The PMI here is also indicative of flat GDP in the second quarter.

Australia meanwhile climbed back into expansion after a decline in May, tied to resumed services growth, but Canada reported falling output, linked to lower service sector activity.

Emerging markets buoyed as mainland China reports best quarter for three years

Emerging market growth meanwhile remained robust overall in June. Although at 53.0, the emerging markets PMI output index signalled a loss of some momentum in June. May had seen growth reach the second-highest for two years. The average output index reading so far this year, also at 53.0, marks the best first half of a year since 2024.

While India remained the best performer among the four largest emerging economies, growth slackened from May’s six-month high to sit at the second-weakest seen in more than three-and-a-half years. Growth slowed in both manufacturing and services.

Slightly weakened growth was also recorded in mainland China during June, but the reading closed of China’s strongest quarterly expansion for three years. Mainland China’s manufacturers enjoyed their best calendar quarter for two years while service sector growth over the second quarter as a whole was the joint-fastest for three years.

Brazil meanwhile edged back into growth territory after a brief decline in May, as a revived expansion of the services economy was accompanied by a slower manufacturing downturn. However, the overall pace of growth remained only tepid.

That left Russia as the only major emerging market in decline, with output dropping in June for a fourth successive month. A stronger drop in services activity was accompanied by a further modest upturn in manufacturing output.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings