Research — July 7, 2026

AstraZeneca’s Baxfendy set for blockbuster sales after hypertension approval

By Ankita Patil

AstraZeneca (LSE: AZN) has opened a new chapter in hypertension treatment after the U.S. Food and Drug Administration approved Baxfendy (baxdrostat) in May as the first aldosterone synthase inhibitor (ASI) for adults with uncontrolled or resistant hypertension. The approval gives the UK drugmaker a first-mover advantage in a large and underserved market.

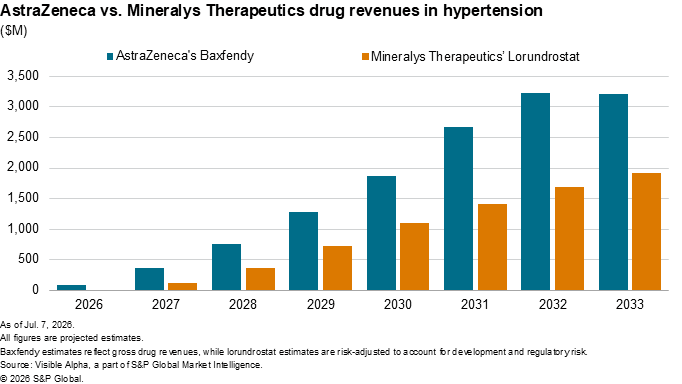

Visible Alpha consensus show the commercial opportunity could ramp quickly. Analysts forecast Baxfendy to generate $94 million in revenue in 2026, rising to $373 million in 2027, its first full year on the market. Sales are expected to surpass the blockbuster threshold, reaching $1.3 billion in 2029 before climbing to $3.2 billion by 2032.

The drug was acquired as part of AstraZeneca's $1.8 billion purchase of CinCor Pharma in 2023 and is a key component of the company's cardiovascular, renal and metabolism franchise. Beyond hypertension, Baxfendy is being evaluated in Phase III trials for primary aldosteronism, chronic kidney disease (CKD) and heart failure, offering the potential to expand its addressable market well beyond its initial indication.

Baxfendy's approval also strengthens AstraZeneca's competitive position ahead of Mineralys Therapeutics (NASDAQ: MLYS), whose rival ASI, lorundrostat, remains in Phase III development for hypertension. Visible Alpha consensus assigns lorundrostat a 90% probability of US approval in the indication, with risk-adjusted sales projected at $122 million in 2027, pending approval, and $365 million in 2028. Analysts expect the drug to reach blockbuster status by 2030, with annual revenue of $1.1 billion.

Mineralys is essentially a single-asset biotech and lorundrostat represents the company's first potential commercial product. AstraZeneca's earlier approval, however, gives Baxfendy a valuable head start. Visible Alpha consensus reflects that advantage, with Baxfendy projected to establish a clear lead in the ASI market and generate substantially higher sales than lorundrostat over the remainder of the decade.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment