Research — June 16, 2026

Incyte's Vega deal adds VGA039 with $1 billion sales potential by 2034

By Romit Gupta

US biotech Incyte Corp. (NASDAQ: INCY) has entered into a definitive agreement to acquire Vega Therapeutics, Inc., adding a late-stage treatment for von Willebrand disease (VWD) that could help offset the looming loss of exclusivity of its blockbuster cancer drug Jakafi.

The acquisition brings VGA039, a Phase III antibody therapy being developed for patients with VWD, a rare genetic bleeding disorder. The candidate is being positioned as a potentially first-in-class monthly, self-administered prophylactic treatment, offering a more convenient alternative to existing therapies that typically require intravenous infusions several times a week.

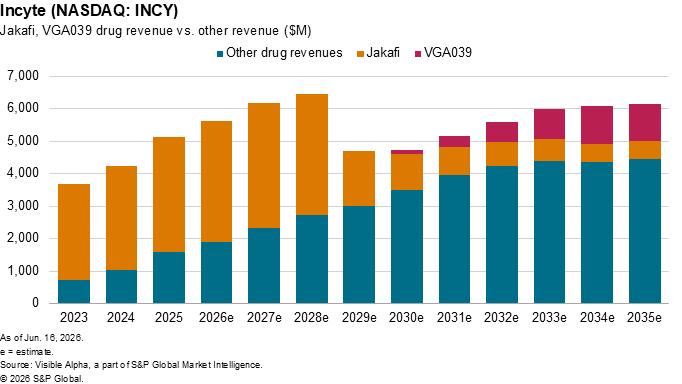

The timing is significant for Incyte. Jakafi, the company's leading treatment for myelofibrosis and other blood disorders, is expected to generate about $3.7 billion of revenue this year, accounting for roughly 60% of total sales. Consensus estimates suggest revenue from the drug will peak at $3.8 billion in 2027 before declining as generic competition emerges following patent expiry in 2028.

Against that backdrop, VGA039 could become an important contributor to Incyte's next phase of growth. The Phase III study is expected to complete in October 2028, with data anticipated in early 2029, potentially paving the way for a commercial launch by 2030. Visible Alpha consensus forecasts point to risk-adjusted revenue of $115 million in 2030, rising to $336 million in 2031 and exceeding $1.2 billion by 2035.

The asset has received several expedited regulatory designations from the U.S. Food and Drug Administration, including Fast Track, Breakthrough Therapy and Orphan Drug status, reflecting both the unmet need in VWD and the therapy's potential clinical significance.

Incyte's overall revenue is projected to increase 9% year-on-year to $5.6 billion in 2026, a slower pace than the 21% growth recorded last year.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment