ECONOMICS COMMENTARY — 08 Jun, 2026

Higher fuel costs drive reacceleration of inflation in sub-Saharan Africa

Increases in fuel costs as a result of the war in the Middle East have driven up costs among sub-Saharan African companies, putting upwards pressure on inflation and likely bringing to an end cycles of interest rate easing seen in a number of economies in the region. PMI data and the anecdotal evidence collected alongside the responses help us to track not only the movements in prices, but the reasons behind them as well. Latest data showed that more than a third of those firms seeing purchase prices increase linked this directly to rising fuel costs.

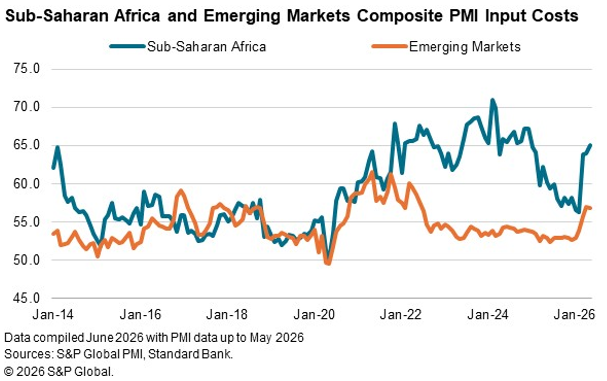

Input cost inflation at 17-month high in May

The reliance of many sub-Saharan African economies on imports of refined petroleum and the relatively large proportions that fuel costs and transport expenses contribute to consumer price index (CPI) baskets are the key reasons why rising oil prices have a substantial impact on inflationary pressures and official statistics in the region.

May PMI data showed that input costs increased rapidly at companies in sub-Saharan Africa midway through the second quarter of 2026, with the pace of inflation quickening for the third month running to the fastest in almost a year-and-a-half. This represents a turnaround from the picture in 2025 when inflationary pressures moderated amid currency improvements. In fact, by February this year the gap between the Input Prices Index in sub-Saharan Africa and that across all Emerging Markets had narrowed to the smallest in more than four years, before expanding back out following the start of the war.

Fuel costs central to higher purchase prices

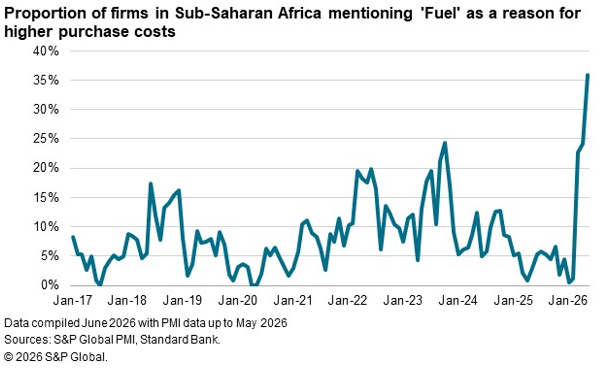

Comments from the PMI survey respondents can help us to understand what drives changes we see in the data. Since the outbreak of war in the Middle East, reports of higher fuel prices driving increases in purchase costs have surged. While February saw only 1% of those firms reporting a rise in purchase costs linking this to fuel prices, by May this had risen to 36%, the highest proportion on record and well above the previous peak seen in October 2023. This highlights the particular impact of fuel prices on firms’ cost burdens at present.

Region’s central banks end rate easing cycles

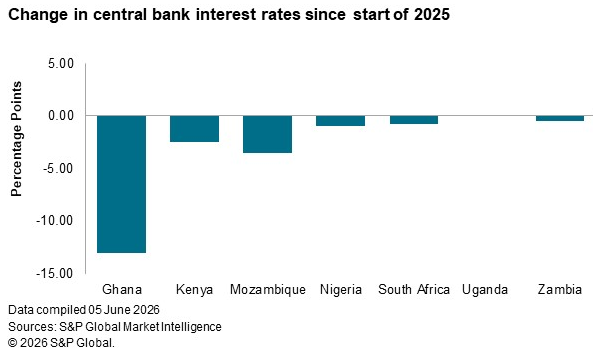

Resurgent inflationary pressures have brought an end to cycles of interest rate reductions seen across a number of central banks in sub-Saharan Africa as inflation softened last year. While all but one of the seven economies covered by PMI data in the region have lower interest rates now than was the case at the start of 2025, none have recorded a reduction at their most recent rate setting meetings, and the South African Reserve Bank even raised rates back up to 7.0% in May.

Looking to the future, the worry for policymakers in the region will be that rises in fuel and transportation costs feed through to second round impacts on other key raw materials. With sub-Saharan Africa also exposed to rising fertiliser prices, food prices are set to increase, widening the impact from the fuel-related shock seen thus far. Monthly PMI data will continue to track the evolution of inflationary pressures across the region, with anecdotal evidence able to show the key drivers of the movements in the data.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings