ECONOMICS COMMENTARY — 11 Jun, 2026

Global employment slumps as business outlook darkens and costs rise

Worldwide job cutting intensified in May, according to PMI surveys produced by S&P Global, with a broad-based deterioration in hiring trends among the major economies. The pace of job cuts is unusual given current order book growth, but reflects growing concerns over the sustainability of demand growth, a deteriorating economic outlook, and rising costs.

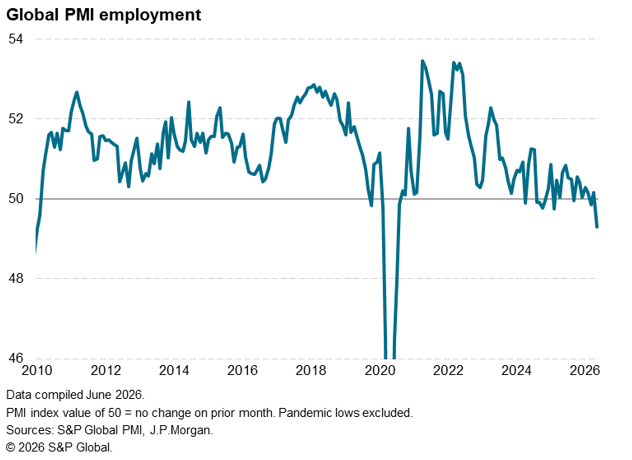

Global PMI signals steepening job losses

Employers worldwide are cutting back on staff in increasing numbers. PMI survey data from S&P Global, compiled at a worldwide level on behalf of J.P. Morgan, recorded the largest net drop in employment globally in May since 2010 if job cuts at the height of the pandemic are excluded.

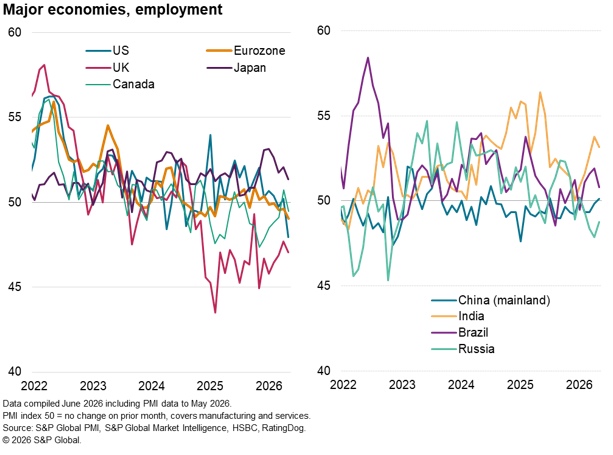

Regionally, the deterioration the labour market was near-universal. Job cutting was especially prominent in the advanced economies, where the overall drop in headcounts during May was the largest recorded since July 2020. Of the major advanced economies, only Japan reported higher staffing levels, and even here the pace of job creation slowed to a seven-month low. While the UK continued to report an especially steep pace of job cuts, job losses spiked in the US to the highest since the early months of the pandemic in 2020.Eurozone job cutting hit the highest since late 2020 and marginal declines were seen in both Canada and Australia.

Jobs growth meanwhile cooled in India and Brazil, which had been two strong performers in prior months, and payroll cuts were again seen in Russia. In contrast, mainland China saw a return to employment growth, representing one of the few gains seen over the past three years, though the increase was only very marginal.

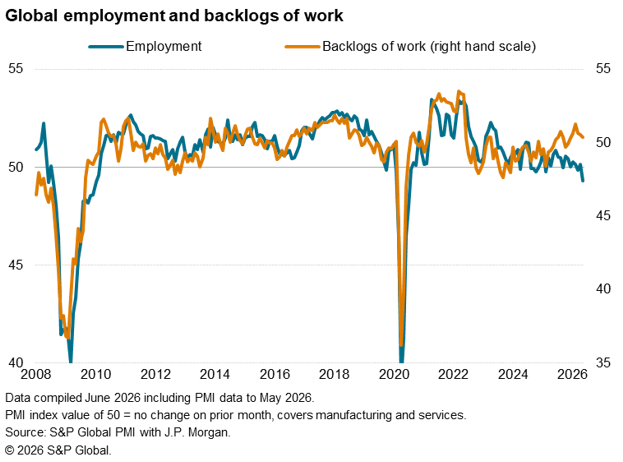

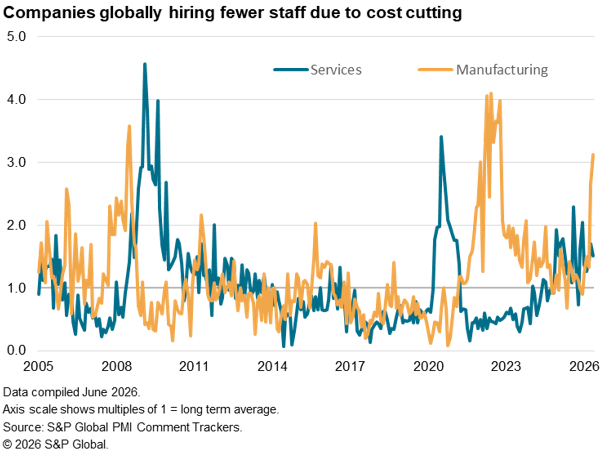

Job cuts reported despite improved order books

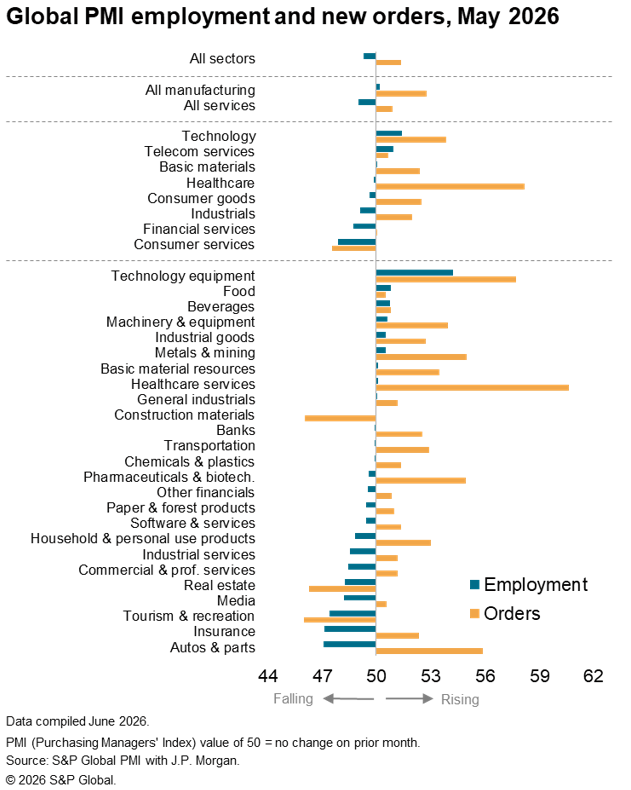

The drop in employment is unusual in the sense that companies are reporting rising demand for their goods and services. Measured globally, inflows of new orders rose at an increased rate in May causing backlogs of uncompleted work to rise for a sixth straight month. This build up of backlogs of work would normally be consistent with firms taking on additional staff in healthy numbers.

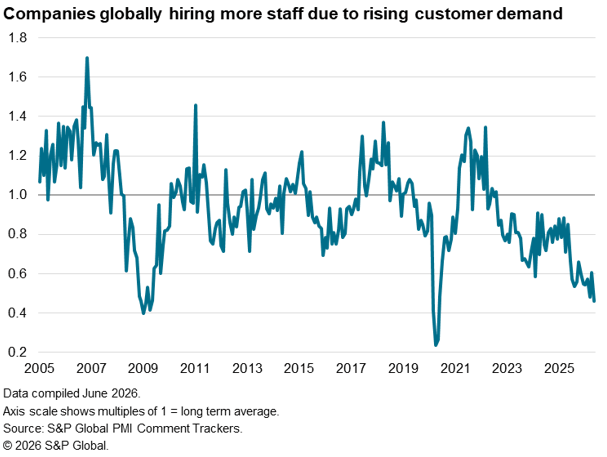

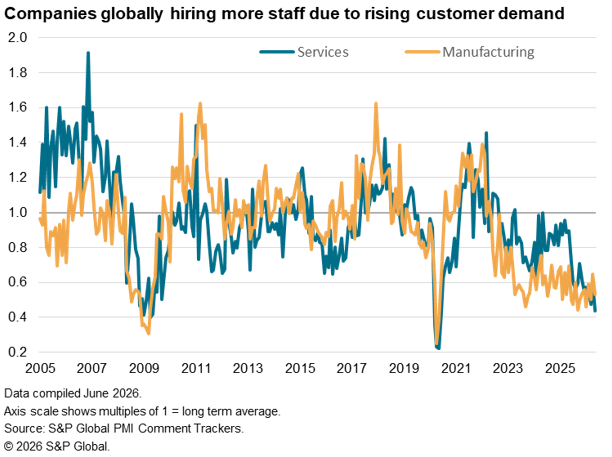

In contrast, when analysing the reasons cited by PMI contributor companies for taking on staff, the number reporting that high customer demand is stimulating hiring is down to one of the lowest levels ever recorded by the surveys globally. Only the height of the pandemic and the global financial crisis have seen less demand-driven employment, with both manufacturing and services reporting historically low levels of demand-driven hiring.

This divergence between weak employment at a time of stronger order book growth is common in both manufacturing and services, albeit with variances if you drill down deeper. For example, demand for consumer services such as travel and tourism has been hit hard by the war and led to a commensurate drop in employment. Conversely, demand for tech equipment is strong amid AI-related investments, supporting jobs growth in that segment. However, many sectors are reporting far weaker hiring than would normally be expected given current order book growth.

Looking beyond the current demand environment, several common themes are apparent globally.

Low growth expectations and rising costs dampen hiring

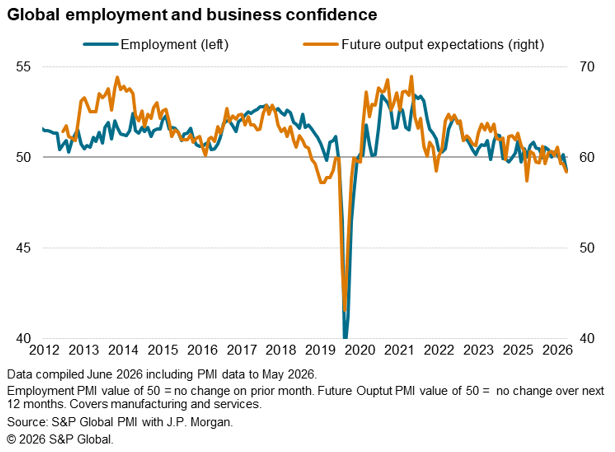

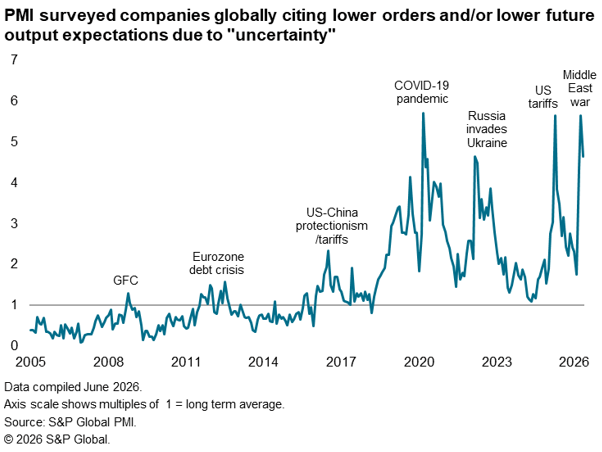

In the first instance, despite seeing improved inflows of orders, business growth expectations for the year ahead have been dented in particular by intensifying geopolitical uncertainty stemming from the war in the Middle East, which has exacerbated other sources of uncertainly, notably fuelled by US tariff policy. While overall business growth expectations fell in May to their lowest since June 2020 barring the shock from surprise US tariff announcements in April 2025, reports of ‘uncertainty’ have spiked to levels rarely exceeded over the past two and a half decades of data history.

In manufacturing, growth expectations have also cooled as many firms are reporting that current demand is being supported by temporary stock piling amid concerns over rising prices and deteriorating supply availability linked to the war. Many firms are aware that, once this stock build has completed, or if supply dries up further, this short-term boost will fade and potentially reverse.

An additional factor is costs, with high energy prices and increasingly broad-based raw material price rises resulting from the war adding to firms’ overall cost burdens. A consequential growing focus on cost-driven job cuts has surged especially in manufacturing globally but is also elevated by historical standards in services.

The role of AI?

One further factor to consider is the extent to which firms are replacing staff with AI technologies, meaning fewer staff are potentially required to fulfil a given level of demand. However, such AI-job replacement is rarely mentioned among PMI survey contributors at present, and a special survey conducted among contributing companies earlier in the year pointed to only a very modest net negative impact of AI, with the additional jobs created to manage AI initiatives expected to partially offset any AI-related job losses over the course of 2026.

Further reading available at The AI and labor landscape 2026: Increased investment, persistent productivity gains and a recalibrated employment outlook | S&P Global.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings