Research — June 26, 2026

Critical rare earth race to accelerate as China tightens grip

By Arti Gupta

China recently imposed export controls on two US rare earth producers. The move targets MP Materials Corp. (NYSE: MP) and USA Rare Earth Inc. (NASDAQ: USAR), both at the center of US’ efforts to build domestic sources of critical minerals and reduce reliance on China, which continues to dominate the sector.

Rare earth elements comprise a group of 17 metals, which are essential for high-performance permanent magnets used in EVs, wind turbines, industrial automation, consumer electronics and increasingly AI-related infrastructure. As demand for these technologies rises, securing access to rare earth supplies has become a national and industrial priority.

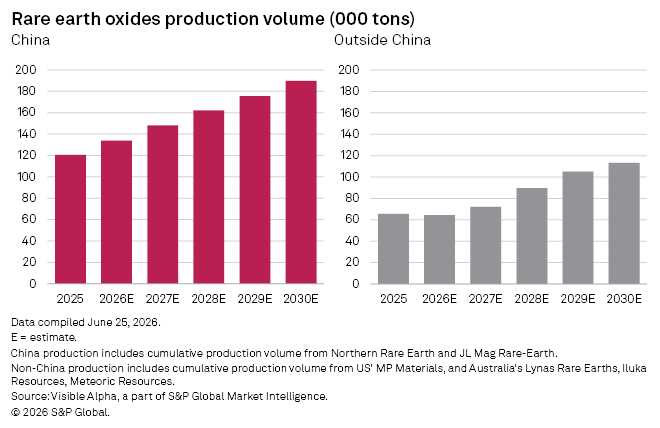

The latest restrictions come as non-Chinese producers accelerate efforts to expand production capacity. MP Materials, which operates the Mountain Pass mine in California, which is the only large-scale active rare earth mine in the US, produced roughly 51,000 tons of rare earth oxide concentrate in 2025, up from about 42,000 tons in 2021. Visible Alpha consensus estimates point to production of about 48,000 tons in 2026.

By comparison, China Northern Rare Earth (Group) High-Tech Co.Ltd. (SSE: 600111), the world's largest producer, generated about 95,000 tons of rare earth oxides in 2025, with analysts forecasting output of 103,000 tons in 2026.

Australia’s Lynas Rare Earths Ltd. (ASX: LYC) produced approximately 12,000 tons of rare earth oxides in 2025 and is expected to increase output to about 16,000 tons in 2026. A second wave of Australian entrants is also emerging. Analysts expect Iluka Resources Ltd. (ASX: ILU) to begin production in 2027, reaching around 5,000 tons in its first year before ramping to 13,000 tons by 2028. Meteoric Resources NL (ASX: MEI) is expected to begin production by 2028 - 2029.

Despite these investments, China remains the dominant force in the industry. Consensus forecasts for seven listed rare earth producers on Visible Alpha Insights indicate China will account for roughly 68% of combined production volumes in 2026. However, as capacity expansions at MP Materials, Lynas, Iluka and Meteoric come online, China's share is projected to decline to about 63% by 2030.

The shift may appear modest, but it reflects a broader restructuring of global supply chains. Governments in the US, Europe and allied nations are increasingly backing domestic mining, processing and magnet manufacturing projects in an effort to reduce strategic dependence on China.

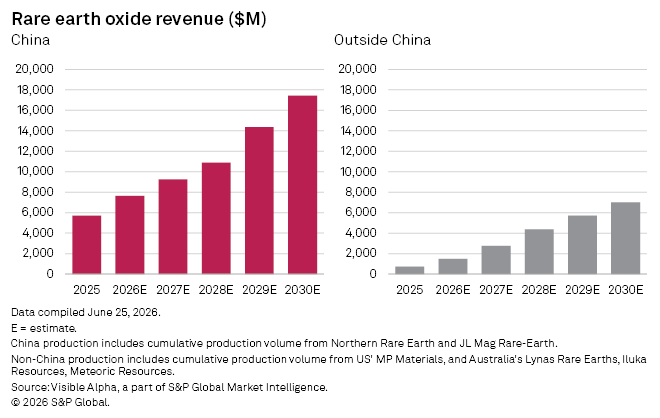

Rising production volumes are also expected to translate into strong revenue growth across the players. Visible Alpha consensus estimates indicate that rare earth oxide revenues for the listed producers in the analysis will more than double over the next five years.

Revenue generated by Chinese producers is forecast to increase from about $5.7 billion in 2025 to $17.4 billion by 2030, while revenues from producers outside China are projected to climb nearly tenfold, from $725 million to just over $7 billion over the same period.

As new projects in the US and Australia come online and existing operators expand capacity, non-Chinese producers are expected to capture a growing share of industry revenues. Even so, Chinese companies are projected to remain the dominant force, highlighting both the scale of China's existing industry and the challenge facing countries seeking to build alternative supply chains.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Theme

Products & Offerings

Segment