Research — June 18, 2026

Cloud growth to power two-thirds of Cerebras revenue in 2026

By Nitin Kansal

AI chipmaker Cerebras Systems Inc. (NASDAQ: CBRS) has seen its shares retreat 31% from post-IPO highs, despite continued enthusiasm for AI infrastructure spending.

The company, which debuted on the NASDAQ on May 14, positions itself as a simpler, high-speed alternative to Nvidia by using a single massive chip rather than many smaller ones. While the approach promises lower complexity and faster performance, questions remain over whether its architecture can maintain efficiency as AI models continue to grow in size and computational requirements.

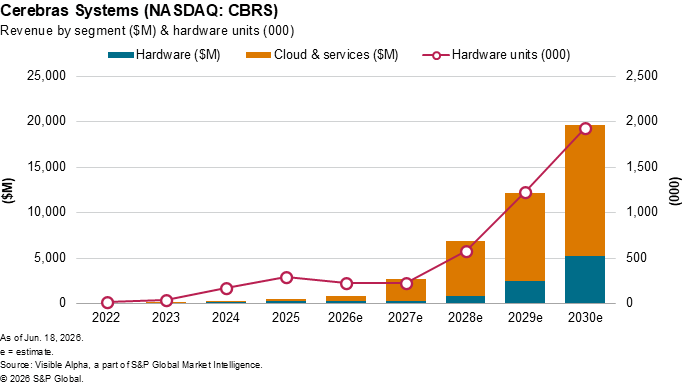

Visible Alpha consensus estimates nevertheless point to robust growth for the semiconductor firm in the forecast period. Analysts expect Cerebras to generate $832 million in non-GAAP revenue in 2026, a 63% increase from 2025 levels. Longer term, revenue is forecast to reach $19.7 billion by 2030.

Growth is expected to be driven increasingly by the Cloud & Services segment rather than Hardware. In 2026, revenue (non-GAAP) from the company's Cloud & Services division is forecast to more than triple, rising 258% year-on-year to $542 million and account for roughly two-thirds of total revenue.

By contrast, Cerebras' hardware business is expected to face a more challenging year. Analysts project Hardware revenue to decline 19% to $290 million in 2026, with unit shipments forecast to fall 20% to 235,000 from 295,000 in 2025.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Theme

Products & Offerings

Segment