Research — June 18, 2026

Adobe postQ: AI momentum lifts results, guidance; monetization concerns linger

By Kanika Garg

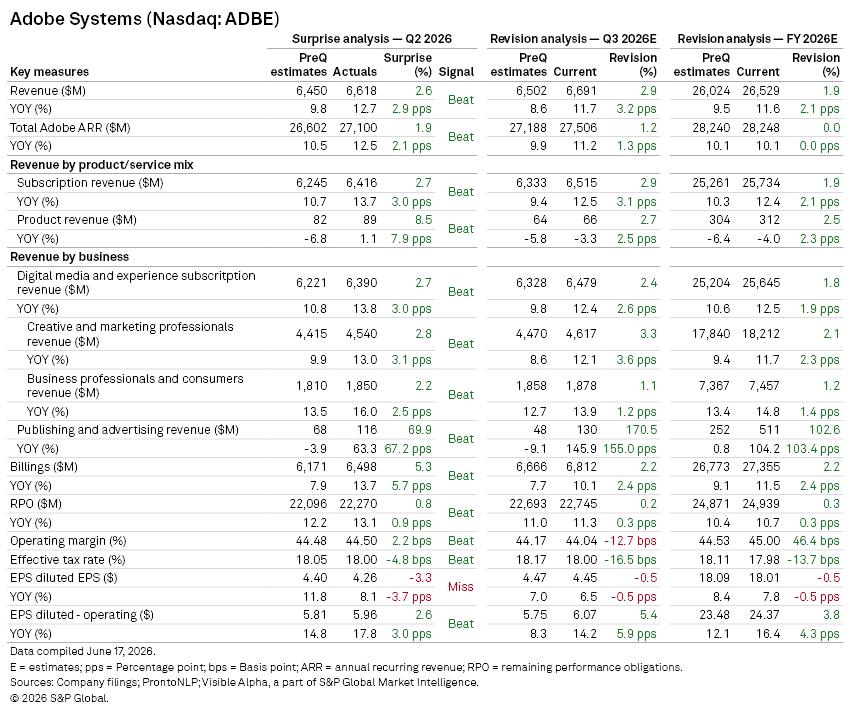

Adobe Inc. (NASDAQ: ADBE) delivered another quarter of better-than-expected growth, with Q2 results surpassing Visible Alpha consensus forecasts across revenue, earnings, billings and annual recurring revenue (ARR), prompting management to raise both quarterly and full-year guidance. The quarter highlighted continued strength in Adobe's core Creative Cloud, Acrobat and Digital Experience franchises, while management pointed to accelerating adoption of AI-enabled products such as Firefly and Express as a growing contributor to customer acquisition and engagement.

Looking at earnings summaries compiled by S&P Global Pronto NLP, along with Visible Alpha pre-quarter consensus expectations and revised outlook, here are some key takeaways.

Key takeaways

Q2 revenue rose 13% year-on-year to $6.62 billion, beating Visible Alpha consensus by ~2.6%, while non-GAAP EPS of $5.96 also exceeded expectations by a similar margin. Outperformance was broad-based, driven by sustained demand across Digital Media and Experience products and increasing adoption of AI-enabled workflows across creative and productivity use cases.

Digital Media and Experience Subscription revenue increased 14% year-on-year to $6.39 billion, ahead of consensus expectations. Within this, Creative & Marketing Professionals revenue rose 13% to $4.54 billion, while Business Professionals & Consumers increased 16% to $1.85 billion, driven by continued strength in core franchises including Creative Cloud, Acrobat, and Document Cloud.

Subscription revenue, which remains the core of Adobe’s model, increased 14% to $6.42 billion and modestly exceeded expectations. Publishing and Advertising revenue more than doubled year-on-year, albeit from a small base.

Forward indicators remained supportive: billings increased 14% to $6.5 billion, beating consensus by more than 5%, while RPO rose 13% to $22.3 billion. Total Adobe ARR reached $27.1 billion, up 13% year-on-year, indicating sustained underlying demand momentum.

Margins remained solid, with non-GAAP operating margin at 44.5%, broadly in line with expectations. GAAP EPS rose 8% year-on-year to $4.25 but slightly missed consensus due to higher expenses and adjustments.

Guidance

Management raised its outlook across the board, signaling continued confidence in demand durability and AI-led engagement trends.

For Q3 FY2026:

- Revenue is guided to $6.67–$6.72 billion versus ~$6.5 billion in preQ consensus expectations

- Non-GAAP EPS is guided to $6.05–$6.10 versus $5.75 expected.

- Creative & Marketing Professionals revenue is expected to be $4.61 billion–$4.64 billion, above the preQ consensus estimate of $4.47 billion.

- Business Professionals & Consumers revenue is expected to be $1.87 billion–$1.89 billion, slightly above preQ consensus estimate of $1.86 billion.

For FY2026:

- Revenue guidance was lifted to $26.5–$26.6 billion versus ~$26 billion prior expectations

- Non-GAAP EPS of $24.35–$24.45 versus $23.44 preQ consensus

- ARR growth is expected at ~10%, with operating margin targeted at ~45%.

Analyst Q&A highlights

Management reiterated confidence in execution continuity despite CEO search dynamics and CFO transition.

AI remains the central strategic priority, with Adobe emphasizing user acquisition and engagement over near-term pricing monetization. Products such as Firefly, Express, and Acrobat are showing strong traction, supported by a freemium-led distribution model.

Management highlighted traffic to adobe.com increased more than 40% year-on-year, reflecting improved discovery via AI-powered search and broader top-of-funnel expansion.

Firefly in particular is gaining early momentum, with management citing 50% sequential ARR growth and improving conversion quality, including higher engagement and lifetime value among converted users.

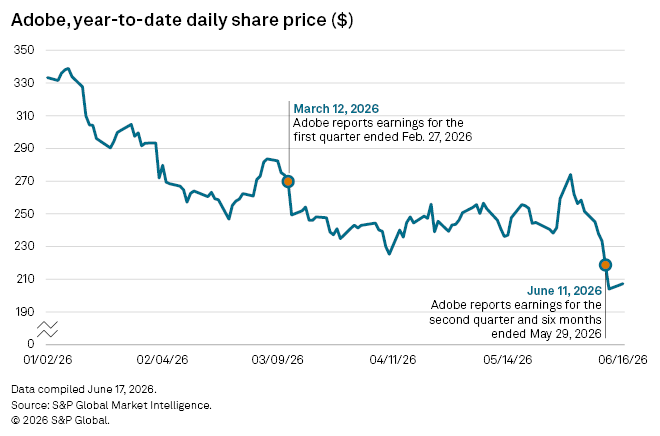

Share price reaction

Shares declined despite the beat-and-raise, reflecting concern that near-term AI monetization remains less visible relative to rising competitive intensity in creative AI tools, as well as governance uncertainty tied to leadership transitions.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment