ECONOMICS COMMENTARY — 01 May, 2026

Week Ahead Economic Preview: Week of 4 May 2026

The following is an extract from S&P Global Market Intelligence's latest Week Ahead Economic Preview. For the full report, please click on the 'Download Full Report' link.

US non-farm payroll report to follow global PMI surveys

The US employment report, global PMI data and a rate setting meeting in Australia are the highlights of the week amid the ongoing uncertainty surrounding the conflict in the Middle East and the US earnings season.

The week ahead is a slow build up to Friday’s US non-farm payroll report, which could be key in steering interest rate expectations for upcoming FOMC meetings. March saw a surprise 178k increase in payrolls, more than offsetting a 92k decline in February. The unemployment rate meanwhile dipped to 4.3%. Alongside a 2.0% GDP rise in the first quarter and a jump in the PCE prices index in March (the annual rate was up from 2.8% to 3.5%, its highest since May 2023, with core inflation also up from 3.0% to 3.2%, a 28-month high), it’s no surprise that US interest rate expectations have taken a more hawkish tilt. However, weak flash US PMI data for April suggest that some of the economic strength seen recently is likely to fade, as the war in the Middle East takes a growing toll on spending.

The big question of course is how long the inflation spike persists and how this affects inflation expectations. Hence, look out for the University of Michigan’s consumer sentiment survey, also out on Friday, which includes households’ views on the inflation outlook.

After the US Fed, ECB and Bank of England all held rates steady at their April meetings, the central bank focus turns to the Reserve Bank of Australia. The RBA hiked rates at each of its last two meetings amid concerns over inflation. A further rate hike is therefore widely anticipated after inflation jumped to 4.6% in March and April’s flash Australia PMI data showed the steepest rise in firms’ prices since August 2022, hinting at more inflation to come. Interest rate decisions are also due in Norway, Sweden, Malaysia and Poland.

The week also sees the staggered release of remaining manufacturing PMI data and comparable service sector survey releases from S&P Global as well as the ISM non-manufacturing index. For the manufacturing PMIs, we urge caution in reading too much into stronger output readings after the flash PMI data showed demand and output to have been buoyed by temporary stockpiling due to war-related price and supply worries. In the service sectors, there were signs that consumer-facing companies have been the hardest hit by the initial impact of the conflict, with concerns over higher borrowing costs an additional drag.

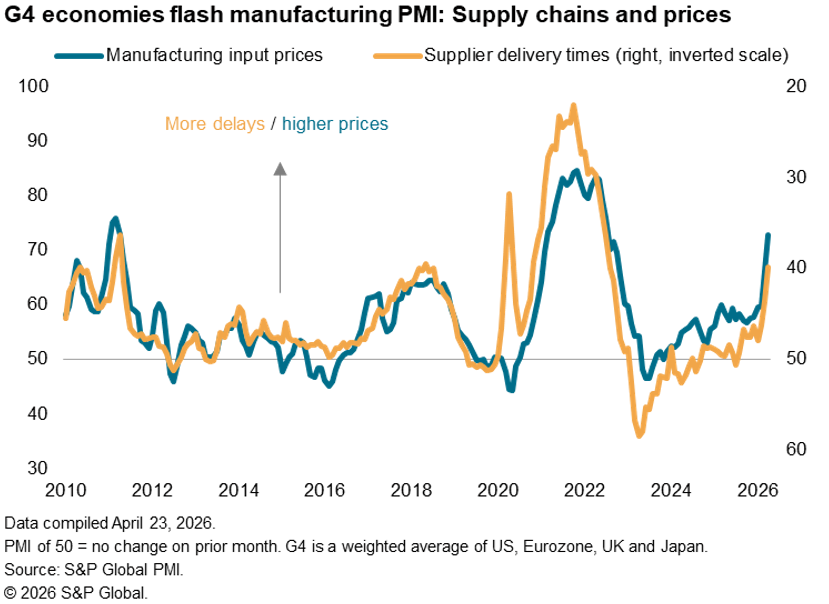

Chart of the week: Supply chain delays hint at further inflation worries

S&P Global’s early April flash PMI surveys showed the incidence of supply delays spiking higher in all four largest developed economies to extents not seen since 2022. With pricing power therefore shifting form the buyer to the suppliers, input prices have surged higher, suggesting that the supply-linked price shock will feed through to consumer price inflation in the coming months.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings