ECONOMICS COMMENTARY — 23 Apr, 2026

US flash PMI signals inflation spike as supply concerns fuel stockpiling, but help boost growth

The flash US PMI survey data from S&P Global indicated a muted rebound in business activity in April, after growth had almost stalled in March on the outbreak of war in the Middle East. However, part of the rebound reflected a short-term boost from stockpiling as companies feared supply shortages emanating from the conflict.

Not surprisingly, prices are already spiking higher in this environment, and not just for energy but for a wide variety of goods and services. The overall inflation picture is now the most worrying for almost four years.

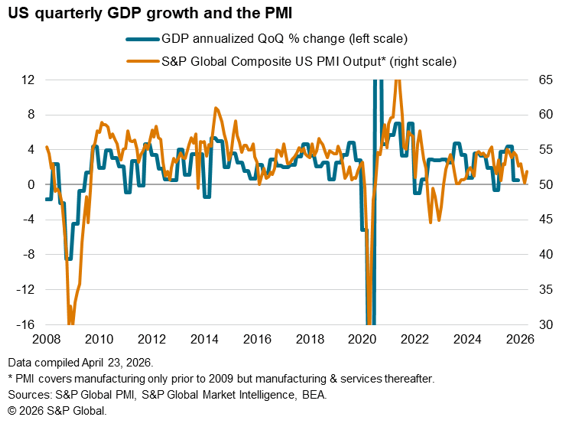

Output rebounds after stalling in March

The headline flash S&P Global US PMI Composite Output Index rose from a two-and-a-half year low of 50.3 in March to a three-month high of 52.0 in April. The improved reading signals faster economic growth at the start of the second quarter, albeit running well below the highs seen last year.

Moreover, we have seen the weakest expansion of output recorded since the start of 2024 over the past three months, with the war in the Middle East squarely to blame according to survey respondents.

The April PMI reading is broadly consistent with the economy struggling to manage annualized growth in excess of 1%.

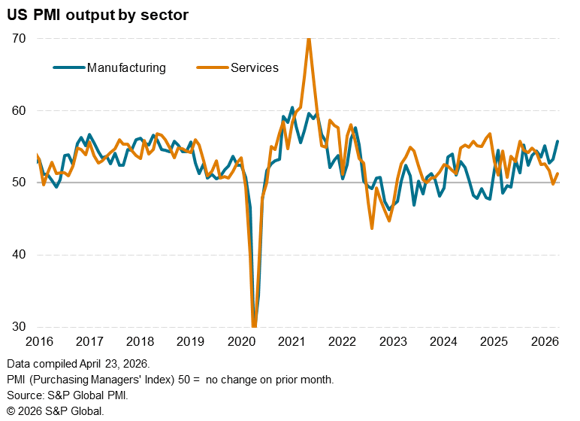

Service sector malaise

Service sector activity remained especially subdued. Although services output recovered slightly from a dip in March, the rate of expansion remained the second-weakest recorded over the past 14 months due to a further cooling of demand growth. New business placed with service providers, ranging from travel and tourism to financial products, rose only marginally and at the slowest rate seen over the past two years, led by an ongoing decline in exports of services.

Lost sales were commonly linked by survey contributors to the uncertainty and disruption caused by the war in the Middle East alongside other government policies and affordability issues, with the prospect of higher borrowing costs acting as a further deterrent to spending.

Manufacturing stockpiling

In contrast, the manufacturing sector saw output rise at the sharpest rate for four years, fueled by the largest influx of new orders since May 2022. However, both output and new orders growth were boosted by stock building amid concerns over supply availability and price hikes due to the ongoing war. Some survey respondents reported “panic” and “emergency” buying in echoes of the problems seen during the pandemic. The rise in orders was driven by domestic demand, as export sales of goods fell at an increased rate.

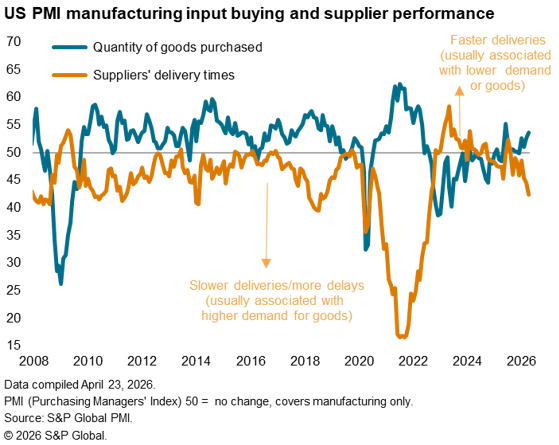

Supply chain delays

War-related issues led to increasingly widespread supply problems, adding to existing supply delays which have been largely blamed on tariffs. Factories reported the greatest lengthening of supplier delivery times since August 2022, with lead times having now lengthened continually over the past eight months. In addition to shipping-related disruptions due to the war, shortages were also linked to the additional purchasing of safety stocks. Purchasing activity rose at the second-fastest rate seen for nearly four years, beaten only by the jump in buying activity seen shortly after last spring’s tariff announcements.

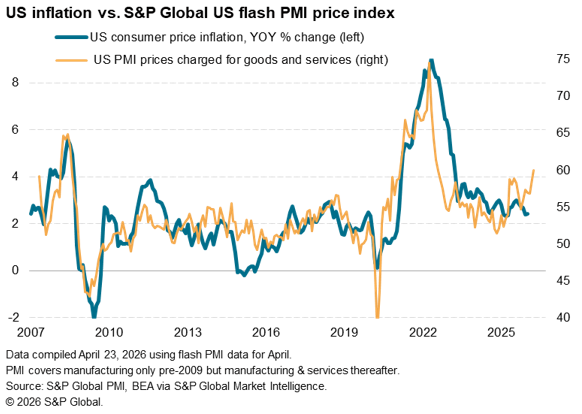

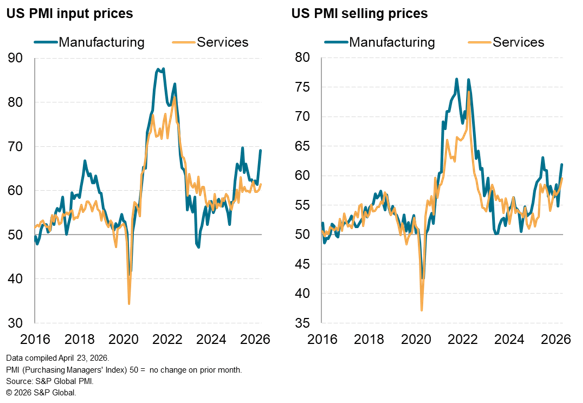

Prices spike

Average prices charged for goods and services rose in April at the fastest pace since July 2022 amid increases in input prices and supply scarcities. The rise in prices is consistent with a marked upturn in the rate of consumer price inflation in the US.

While manufacturers reported an especially steep jump in goods prices, with the rate of inflation at a ten-month high, service sector selling price inflation also accelerated to reach a 45-month high.

Manufacturing input costs meanwhile surged especially steeply, rising at the fastest rate for ten months and posting the second-steepest increase since July 2022, while the rise in services costs was the largest since December and among the sharpest seen over the past three years. Alongside higher energy prices, companies reported increased charges for a broader swathe of commodities and inputs, as well as citing increased staffing costs.

Access the latest flash PMI press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings