ECONOMICS COMMENTARY — 08 May, 2026

Week Ahead Economic Preview: Week of 11 May 2026

The following is an extract from S&P Global Market Intelligence's latest Week Ahead Economic Preview. For the full report, please click on the 'Download Full Report' link.

Inflation data to reveal war impact on affordability and guide policymakers

Inflation comes under the spotlight in the coming week, with consumer price gauges updated for the United States, eurozone and mainland China. Europe’s growth trajectory will be meanwhile assessed via first quarter GDP releases.

Inflation data for the US will provide important guidance for policymakers. March saw a 0.9% rise, taking the annual rate of inflation to 3.3%, its highest since May 2024. Much of the rise could be attributed to the surge in energy prices following the outbreak of war in the Middle East. Core inflation, which excludes food and energy, rose slightly less than the market had expected, up from 2.5% to 2.6%, though clearly above the Fed’s 2% target.

April has meanwhile seen survey data send mixed signals for prices. While PMI survey data showed manufacturing input cost inflation accelerating, services input cost inflation edged slightly lower amid price competition in the face of weak customer demand. However, overall rates of increase remained elevated by history standards, and supplier delivery times have lengthened again, which could feed through to more price pressures as it signals a growing shift to a sellers’ market for a wide variety of goods. These developing price pressures will also be eyed via the updated official US producer price data due in the week.

Industrial production data could meanwhile prove to be robust after strong US PMI survey data, though the latter came with the caveat that some of the gains in the past two months have been linked to precautionary stock building, and could hence prove temporary.

In Europe, UK GDP data are released for March, giving a full picture of first quarter growth. Comparable quarterly GDP data are also issued for the eurozone. While both economies took a hit from the war in March, first quarter GDP looks to have grown by 0.2-0.3% in both cases. However, whereas the UK PMI bounced back in April, the eurozone slipped into decline. The latter is a complication for ECB policymakers, who have grown further hawkish. The ECB will therefore be eager to see updated inflation numbers, strong readings for which could cement market expectations of a June rate hike.

In APAC, inflation numbers will also come under the spotlight for mainland China. Survey data have pointed to a relatively modest impact on prices from the war in the Middle East so far, though April nonetheless saw average prices charged for goods and services rise at a rate not beaten for four years.

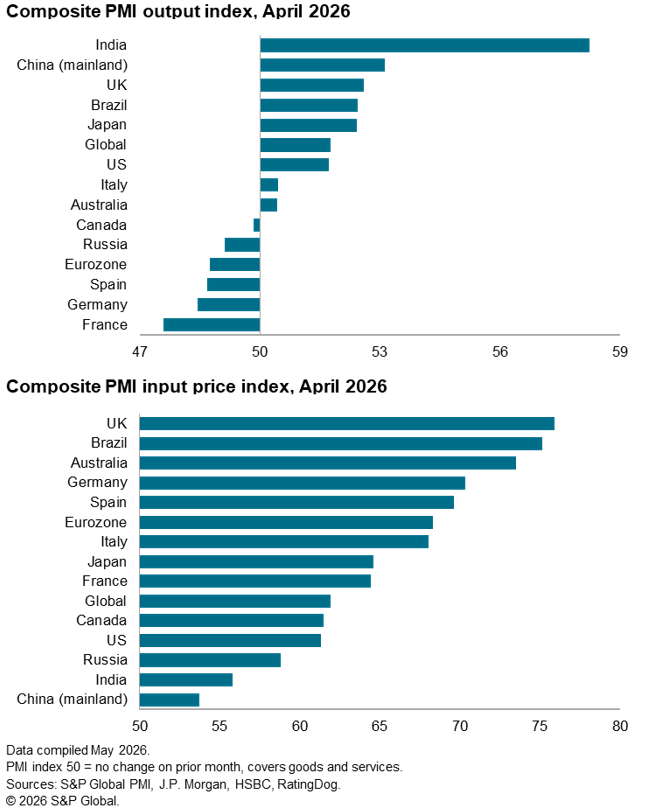

Chart of the week: Worldwide PMI surveys show Europe hit hardest by war impact in April

Of the world’s largest economies, S&P Global’s PMI surveys showed the eurozone nations of France, Germany and Spain to have been hardest hit by the war in the Middle East in terms of economic growth, each reporting lower output in April. The UK meanwhile suffered the steepest rise in input costs, widely linked to the war’s impact on energy and shipping prices

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings